Posts Infrastructure Danube 5025 24 February 2025

The operation of the maritime corridor led to a 46% drop in transshipment at ports on the Danube in 2024

The war in Ukraine and the blocking of Ukrainian seaports on the Black Sea led to the diversion of some export and, to a lesser extent, import cargo flows to Ukrainian ports on the Danube. During 2022-2023, their cargo turnover increased six times compared to pre-war 2021. However, the successful operation of the sea corridor from the ports of Great Odessa predictably led to a drop of almost half of the Danube transshipment. As a result, we have a surprising situation: the Danube ports, which saved Ukrainian exports in the first two years of the war, now need urgent help themselves. What are their prospects and what are their problems, GMK Center has been looking into.

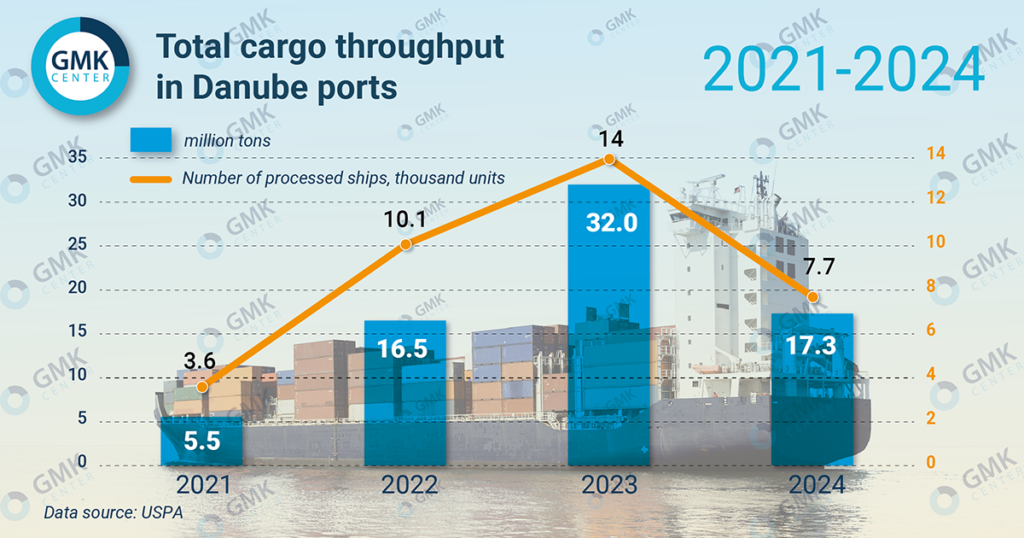

Figures of transshipment on the Danube River

In 2024, Ukrainian seaports increased cargo transshipment by 57% y/y. – to 97.2 million tons. The main reason for this significant growth was the successful operation of the sea corridor, through which last year 79.9 million tons of cargo passed, including 76.4 million tons for export.

Also, the work of the corridor to reorientation of cargo flows. Ports of Great Odessa in 2024 increased the volume of cargo transshipment in 2.6 times compared to 2023 – up to 79.9 million tons, while ports on the Danube reduced this figure by 45.9% – 17.3 million tons. However, this is still three times the pre-war cargo turnover.

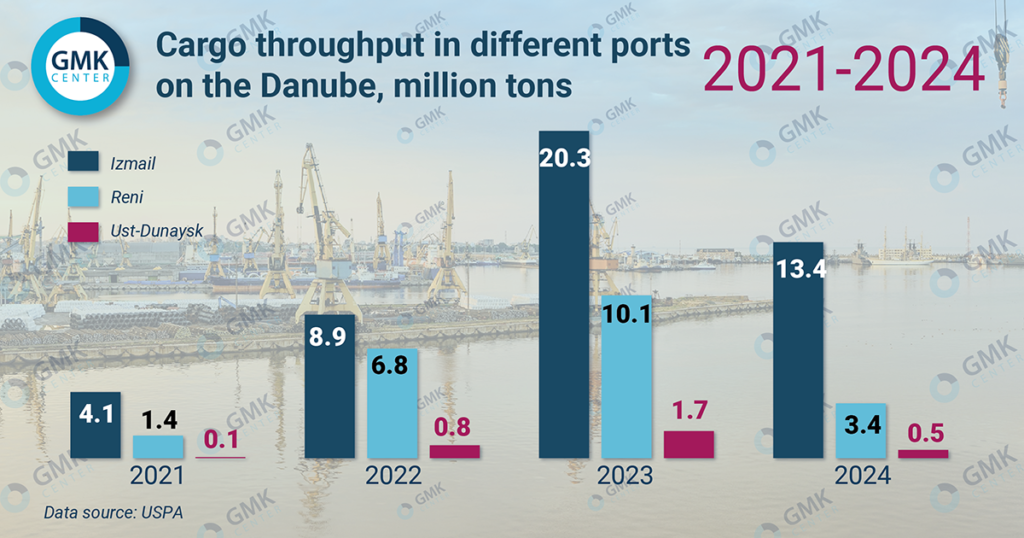

The dynamics of transshipment decline in the Danube ports last year compared to 2023 was as follows:

- Izmail – by 33.9% – to 13.4 million tons;

- Reni – by 66%, to 3.4 million tons;

- Ust-Dunaysk – by 69.6%, to 0.5 million tons.

“As of today, only cargoes that can be loaded through the port Izmail for export remain in the Danube region. They are loaded on small vessels – kosters – with a carrying capacity of up to 10,000 tons. This fleet serves short distances in the direction of Black Sea and Mediterranean ports. It is no longer a question of sending large shipments of agricultural products by river fleet to Constanta, where they used to be reloaded on large ships and sent to Southeast Asian countries,” explains Iryna Kosse, a senior researcher at the Institute for Economic Research and Policy Consulting.

Reasons for the drop in Danube transshipment

The reasons for the significant drop in cargo turnover of Ukrainian ports on the Danube:

1. Cargo overflow to Odessa ports due to the stable operation of the sea corridor. This overflow is caused by purely economic reasons:

- shallow depths and restrictions on the tonnage of ships accepted. Deep-water ports of Great Odessa have many times greater throughput capacity due to acceptance of vessels of larger tonnage than shallow-water Danube ports.

- More expensive logistics to ports on the Danube. The additional shoulder from Odessa is about 250 km by road or 200 km by rail.

“The attractiveness of prices now is exactly in the ports of Great Odessa. If we talk about Pivdennyi, they offer a price of $8-10 for transshipment of a ton of cargo. Izmail is ready for a price of $6-7, taking into account that transportation will cost another $10-12 per ton, so there is a difference”, says Eugene Perez Baro, CEO of Porta Maris.

2. Frequent shallows of the Danube. They are observed in the summer and fall period and significantly limit or make it impossible to navigate.

3. The situation on the grain market. The fall of Danube transshipment in 2024 was aggravated by high dependence on grain (62.5% in the structure of cargo handling in 2023), which with the opening of the corridor moved to Odessa and a general decline in yields. In addition, global grain prices have fallen, so market operators started to consider logistics costs even more carefully.

Infrastructural development

Amid the drop in transshipment, there is one positive moment – the infrastructure of the Danube ports has improved significantly since the full-scale invasion began. The passage of ships through the mouth of the Bystre River was opened, 23 new terminals (mainly for grain and liquid cargo) and 20 new transshipment points were opened by the end of 2023. In particular, Nibulon (Izmail), Kernel (Reni), Asket Shipping, Danube Logistics Group, etc. opened their terminals. Initially, market operators delivered from the Danube to the Romanian port of Constanta, where cargo was transshipped to sea vessels. Total investments in the infrastructure of ports on the Danube amounted to more than $100 million.

Also, the number of pilots has increased several times, dispatching has been improved, including the launch of night-time navigation of ships, etc. The main thing is to increase the available depths. However, the main thing is to increase the available depths. According to Iryna Kosse, in 2022-2023, AMPU will make a dredging dredge. AMPU dredged the Danube ports, which allowed to increase the number of ship calls there, but it must be done regularly, as the river bed is constantly silting up.

The capacity of the Danube ports allows handling vessels with draught up to 6-7 meters and deadweight up to 6,000 tons. Previously, the export capacity of the Danube cluster was expected to grow to 35-40 million tons in 2024 from 33 million tons in 2023. However, now the design capacity of the ports of Reni (8 million tons) and Ust-Dunaisk (4 million tons) is much higher than their current transshipment figures, although Izmail (8.5 million tons) is still in high demand.

At the same time, rail accessibility of the Danube ports remains limited. The railroad to the port of Izmail is single-track and non-electrified, while the line to Reni runs through Moldova – it is limited in size and transportation is more expensive. And improvements are not to be expected. UZ planned two projects with a private investor to expand capacity to Izmail, but due to reduced transshipment, this investor from AIC refused to participate.

Options for solving the problem

Against the backdrop of the deep decline in Danube transshipment, operators of the customs segment of the logistics market are raising the issue of the need for urgent support measures.

“The Danube is stopping. The Danube needs a comprehensive plan based on market realities, not illusions that supposedly ‘spot’ projects and improvements will change the overall picture. Any plan to save the Danube needs to start with the concept of a competitive logistics chain. Railroad, accumulation, transshipment, fleet – the plan should include a combination of all links,” former CEO of the Ukrainian Danube Shipping Company (UDP) Dmytro Moskalenko noted earlier.

Possible options to support the industry and increase transshipment through the Danube ports look like this:

- Fixing UZ tariffs. Shippers (agrarians) and carriers have repeatedly raised the issue of tariffs. Market operators propose to leave the tariffs for cargo transportation to Izmail unchanged amid UZ wants to index them by 37%. UZ’s tariff increase may raise the cost of logistics through the Danube ports by about $5-7 per ton of cargo, putting Danube at an even greater disadvantage compared to Odessa ports.

- Reducing the cost of port transshipment on the Danube. AMPU may take a corresponding decision to reduce port fees (e.g., shipping fees).

- Development of niche cargo transportation. Fertilizers, general cargoes, oil products, gas and hazardous fertilizers requiring either specialized infrastructure or oriented to further transshipment in Constanta remain partially on the Danube route.

- Interception of cargoes at the ports of Great Odessa. In deep-water ports it is more profitable to unload/load a vessel of larger tonnage rather than a small vessel of 5 thousand tons, which can be sent to the Danube ports. However, the ports of Great Odessa themselves are not very willing to accept small shipments of up to 5000 tons. The target segment is import or export of small consignments, which are sent to Turkey and Mediterranean countries, as well as to consumers upstream of the Danube.

- Dredging and maintaining passport depths. Without this, even those vessels that could potentially use the Danube will simply not be able to enter at full draft. Maintaining depths of 7 meters is essential for larger vessels – it immediately expands the range of possible cargoes and makes transshipment more cost-effective.

- Development of cooperation with large shippers. We are talking about deepening cooperation with large companies like Kernel and Nibulon, which came to the region after the beginning of the war. This is a win-win situation, as the ports are guaranteed a significant cargo base, while the large companies themselves receive attractively priced logistics. For example, after the start of the war, Nibulon invested $22.5 million in a transshipment terminal in Izmail and by the end of 2024 it had already recouped these investments.

- Development of processing facilities and industrial production in the port zone. This can become a “magnet” for certain cargoes, but it is possible only within the framework of a comprehensive policy of development of this region.

For its part, the relevant ministry assures that it is making every effort to expand the capacity of the ports in the Danube region and to implement projects for their modernization.

Importance of the Danube for steel industry

Iron and steel products are among the traditional ones for the Danube ports. In particular, Izmail is a transshipment point for the delivery of Ukrainian iron ore for a number of European steel mills. For example, Ferrexpo has traditionally shipped about 10% of its production up the Danube. The company has a competitive advantage in the form of its own company on the Danube, First-DDSG. It owns various types of river vessels, including tugs and barges, which provides flexibility in handling different types of cargo and adapting to different operational needs. In addition, the availability of its own bunkers in Vienna ensures fuel supply at a competitive price.

“The Danube is a convenient and cost-effective means of serving customer needs. Full access to Europe’s network of rivers and canals, including the Danube, complements Ferrexpo’s rail and marine logistics network, providing flexible delivery solutions to customers across Europe,” Ferrexpo said.

In turn, UDP has signed contacts for 2025 with a 30% increase in the transportation of Ukrainian iron ore raw materials. However, the absolute indicators of iron ore transportation are now small due to low demand in Europe, and there are practically no prospects for their growth in 2025.

Currently, iron and steel companies use the Danube ports very limitedly – either for transportation of small vessels by sea to the markets of Mediterranean countries and up the Danube or for import of small consignments.

“In terms of export products through the port Izmail the main cargo turnover of Metinvest is iron ore raw materials and steelproducts. Historically, Izmail is the key port for delivery of our products to European customers along the Danube. The versatility of this port in handling both bulk and general cargo, as well as sufficient number of unloading fronts and number of berths allow to fully cover the demand of Metinvest’s cargo flow in this direction,” Metinvest informed GMK Center.

In their turn, ferroalloy plants now transport finished products to Romania via the Danube and import small volumes of ore under old contracts. In particular, exports of ferroalloys to Italy and Turkey in 2024 amounted to 17 thousand tons and 15.3 thousand tons respectively, imports of manganese ore – 84.3 thousand tons.

At the same time, iron and steel shippers, as well as representatives of other industries, realistically assess the overall situation with the Danube logistics. Especially when it comes to the prospects of transportation of their products to the EU countries.

“Unfortunately, the current level of service does not allow competing with direct road transportation neither from the economic point of view, nor from the point of view of transit time,” says Olexiy Yanovsky, director for procurement and logistics at Interpipe.

At the same time, under the conditions of war and remaining risks of shelling of port infrastructure, there is still a need for alternative logistics routes for exports and imports with a sufficiently high throughput capacity. Therefore, despite the fact that the importance of the Danube ports has decreased with the opening of the sea corridor, these routes need to be maintained as an element of Ukraine’s economic security and logistics diversification.

-

Opinions Industry rolled steel

25 June 2025

19 May 2025

14 April 2025

17 March 2025