Opinions Industry ferroalloys 551 24 February 2026

Ferroalloy plants operated at minimum capacity in 2025 — at 10%

The plants were forced to shut down after an electricity shortage in January 2026

Although ferroalloy plants demonstrated higher production figures last year than in 2024, their capacity utilization remained minimal. Given the security threats, high electricity prices and supply disruptions, labor shortages, and other constraints, a significant increase in production and exports is virtually impossible.

Situation in the industry

Throughout 2025, companies in the industry operated steadily, albeit at minimal capacity utilisation of around 10%. Following the attacks on energy infrastructure in November and the rise in electricity price caps, production declined significantly. For example, the Nikopol Ferroalloy Plant (NFP) reduced its production from 10,000 tons to 3,500 tons, making production unprofitable. The plants have been shut down since January 19, 2026.

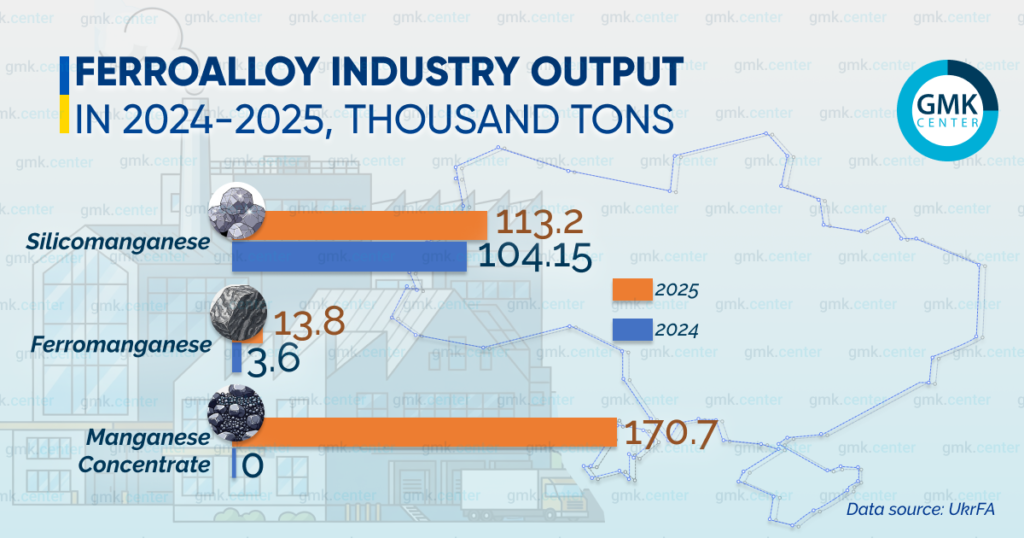

At the end of the year, Ukraine’s ferroalloy enterprises increased their output by 17% y/y – to 127,000 tons. Production increased as follows:

- silicomanganese – by 8.7% y/y, to 113,200 tons;

- ferromanganese – almost 4 times, to 13,800 tons.

No ferrosilicon or other ferroalloys were produced.

For comparison: in pre-war 2021, enterprises produced 858.7 thousand tons of ferroalloys.

Ferrosilicon plants have refocused on the domestic market, as high domestic prices, difficulties with export logistics, and other factors create more favorable conditions for supplying the Ukrainian market rather than exporting.

There is even re-export: products previously exported for sale in Europe are being returned or will be returned to fulfill contracts on the domestic market during the period of plant downtime. The current volume of production is insufficient to fulfill export contracts.

As for the situation at mining enterprises, they produced 171,000 tons of manganese concentrate in 2025. This is an increase compared to the previous year, but extremely small when compared to pre-war figures. For comparison: in 2021, the Pokrovsk Mining and Processing Plant (Pokrovsk Mining) produced 1.21 million tons of concentrate, and the Marganets Mining and Processing Plant (Marganets Mining) produced 551,000 tons.

Pokrovsk Mining operated in September-November 2025. The extracted products were stored at the enterprise, as logistical capabilities did not allow for their removal. Under current conditions, manganese ore production is intended for the company’s own ferroalloy plants, not for export.

In 2026, Pokrovsk Mining plans to increase manganese concentrate production by 3.4 times compared to the previous year, to 220,000 tons. Currently, both plants are idle due to a lack of electricity.

Export status

According to the results of 2025, Ukrainian ferroalloy enterprises exported 93.8 thousand tons of products, which is 21% more than in 2024. Exports were made to nearby markets: Algeria (21.3 thousand tons), Poland (26 thousand tons, +24% y/y), and Turkey (20.4 thousand tons, +87% y/y). Export revenue for 2025 increased to $105.4 million, compared to $88.6 million a year earlier.

There is foreign demand for Ukrainian ferroalloys, but prices on international markets do not allow products to be sold without losses. Due to the cost of electricity, which accounts for more than 50% of the cost price, Ukrainian producers are not competitive.

Ukrainian producers do not win tenders at Turkish and North African plants due to price, logistics, and delivery times. The difficult situation with transshipment in ports and the high cost of transportation through Europe make Ukrainian offers uncompetitive.

Industry challenges

The main challenges facing the ferroalloy industry include the following:

- The cost of electricity and its availability

Ferrosilicon enterprises, which operate dozens of electric arc furnaces, suffer from high electricity prices that exceed those in developed European countries. The NFP operates a cogeneration plant to meet non-industrial needs, which has encountered a problem with Ukrenergo regarding connection and metering of electricity transmission to the unified energy system. The documents have already been submitted for review. Perhaps this procedure will be simplified.

- Logistics

To deliver ore from Pokrovsk Mining to NFP, cargo must be transported through Kryvyi Rih, as the railway connection between Marhanets and Nikopol has been destroyed. This has led to a 10–20-fold increase in transportation costs. Due to the high tariff, the extracted ore remains in the plant’s warehouse, meaning that NFP cannot obtain the ore. It is impossible to transport the required volumes by road.

- Insurance against military risks

Insurance against military risks is only possible at a distance of more than 100 km from the combat zone. Nikopol, Zaporizhia, and Marganet are located much closer to the line of contact, so companies in the industry cannot insure their assets or risks. Insurance companies avoid taking on risks in the frontline zone amid constant shelling.

- Staff reservation

After the latest shelling, the enterprises were cut off from the power supply and went into idle mode. During downtime, enterprises cannot pay salaries of UAH 20,000, which is one of the main criteria for reserving employees. As a result, enterprises lose their right to reserve employees. Pokrovsk Mining and Marganets Mining cannot reserve the necessary personnel to maintain pumps, mines, and electrical equipment because they do not meet the salary criterion.

-

OpinionsIndustrysteel consumption

13 July 2026

13 July 2026

11 June 2026

28 May 2026