News Industry Ukraine’s iron and steel industry 3318 22 August 2025

The utilization rates of individual companies in the industry vary significantly depending on the situation at the plants and sales markets

In 2025, Ukraine’s iron and steel industry continues to face significant challenges due to the military situation and economic instability. In view of this, the industry’s key enterprises demonstrate different levels of capacity utilization, reflecting both the impact of external factors and the companies’ adaptation to the new market realities.

GMK Center has assessed the capacity utilization of enterprises in various segments of the iron and steel industry based on production figures for 2024 and 6 months of this year.

Mining and Processing Plants

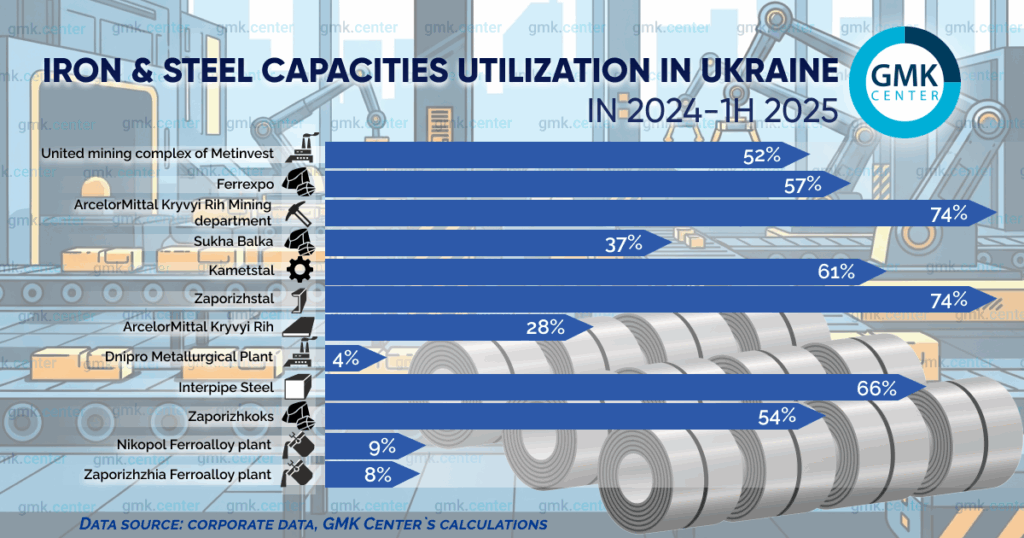

As of the end of 2024, Ukrainian mining and processing plants operated at different levels of capacity depending on the company. For example, Metinvest Group’s Northern and Central Minings have reached almost 100% capacity, while Southern and Ingulets Minings are in a long downtime due to weak profitability and pressure from a number of internal factors. GMK Center estimates that the average utilization rate of Metinvest’s United Minings was 52% in 2024 and 1H2025.

Since May this year, Ferrexpo’s Poltava Mining and Processing Plant has suspended two of its three pelletizing lines due to non-refund of VAT on exported products. Without the VAT refund, Ferrexpo planned to reduce production to 25% of its full capacity, but the company still shows a fairly high level of utilization – 57% in the last year and the first half of this year.

The mining division of ArcelorMittal Kryvyi Rih operated at 74% last year, while DCH’s Sukha Balka had a utilization rate of about 37%. At the same time, Kryvyi Rih Iron Ore Plant (KZHRK) has been idle since March 2025 due to a lack of markets and demand for its products, as well as non-refund of VAT.

Steel plants

The overall utilization rate of steelmaking companies in the first half of this year was about 45% (46% in 2024). However, the performance of individual companies varies significantly depending on their financial and economic condition and the situation in their sales markets.

For example, the average utilization rate of Kametstal in 2024 and the first half of 2025 was 61%, while Zaporizhstal’s was 74%. For its part, Interpipe Steel, according to GMK Center, reached an average utilization rate of 65.6% over the same period.

Last year, ArcelorMittal Kryvyi Rih operated at 27.5% of its steel production capacity. Dnipro Iron and Steel Works (DMZ) operates only rolling facilities with minimal utilization based on the availability of orders. GMK Center estimates that DMZ’s capacity utilization does not exceed 4%.

Ferroalloy plants

The state of the ferroalloy industry has deteriorated significantly since the start of the full-scale invasion. At the end of 2023, the key producers, Zaporizhzhia Ferroalloy Plant and Nikopol Ferroalloy Plant, suspended production due to high electricity prices and proximity to the frontline. In the second quarter of 2024, the companies resumed operations and gradually increased production. At the end of last year, the utilization of ferroalloy enterprises was extremely low, not exceeding 8-9%, although it increased slightly in 2025.

The mining and processing plants – Pokrovske and Marhanets – are not currently producing, although sinter plants can process raw materials in small quantities.

Coking plants

Zaporizhkoks is currently operating at about 54% capacity, while DMZ has decided to completely decommission its coke production.

Reasons for low capacity utilization

The general factors that significantly affect the level of production utilization and, in general, the nature of economic activity of the iron and steel companies include the following

- high security risks;

- constant growth of prices and tariffs for energy resources (electricity, gas);

- high logistics tariffs;

- significant shortage of personnel;

- trade wars in the world, which negatively affects external demand, etc.

Against this backdrop, the Ukrainian economy has no significant growth drivers, and the government’s decisions to stimulate economic activity have little or no positive impact on the level of production utilization of iron and steel companies.

-

15 June 2026

18 June 2026

16 June 2026

16 June 2026