News Global Market rebar prices 4654 24 September 2024

Consumer buying activity is not sufficient to support prices

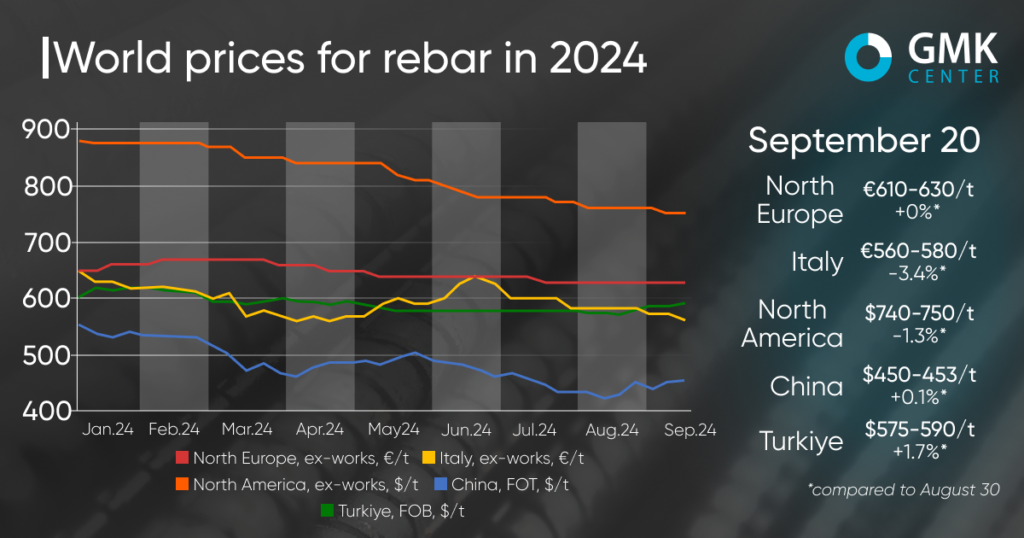

In September, global rebar prices did not show a clearly defined trend. In the US and the EU, the dynamics were negative, but in Turkey and China, growth was observed, which is not considered sustainable.

Rebar prices in Turkey increased by 1.7% to $575-590/t FOB during the period August 30 – September 20, 2024. The upward trend in the market has been observed for the first time since March, as prices declined in April-May and stabilized at $580/t in June-August.

A slight increase in rebar prices in the Turkish market is a result of rising scrap prices. In addition, market sources point to improved demand from European consumers, mainly from Romania and Bulgaria, amid the strengthening of the euro against the dollar. At the same time, the main export demand comes from the Balkans. Yemeni buyers are not active, as they have sufficient stocks. Domestic demand has also picked up, but local consumers consider current price levels ($590-610/ton Ex-Works) too high.

At the same time, weak sentiment in the global steel market, mainly pessimistic expectations about the Chinese economy, continues to put negative pressure on the market. Turkish rebar producers note that the lowest operating price level is currently estimated at $580-585/t FOB. At the same time, urgent orders are fulfilled at a higher level, and offers for shipment in November-December are discussed individually.

Rebar prices on the European market remained largely stable in August-September. In Northern Europe, prices have been at €610-630/tonne Ex-Works since mid-July, while in Italy, offers have fallen by 3.4% to €550-560/tonne Ex-Works since the beginning of September, mainly following the trend in scrap prices. At the same time, prices on the Italian market are expected to rise to €560-580/t this week. Thus, local plants are trying to stop the prolonged decline and restore margins, which are significantly affected by high production costs.

Buyers in the European market are taking a cautious approach to purchases, working with existing stocks as long as possible. At the same time, infrastructure construction is expected to pick up in some regions, which will help steelmakers to implement their plans to raise their offer prices in the second half of September.

The overall picture of the European market is uncertain. On the one hand, producers are trying to restore margins by gradually raising prices, but on the other hand, consumers are set to cut prices, given the fall in scrap prices and weak economic performance, which continue to put pressure on the construction industry.

In the US Midwest, rebar prices have fallen by 1.3% since the beginning of September – to $740-750/t Ex-Works. Since the beginning of the year, prices have never shown a monthly increase.

Bid prices declined amid a weakening scrap market, low demand for rebar and potential growth in imports. Market participants predict that the market will only feel a noticeable relief in the second quarter of 2025, and until then prices will fluctuate in limited ranges.

At present, some price increases are expected in October, as there are prospects for an increase in scrap prices with the start of October trading. Maintenance shutdowns will continue next month, but the number of plants that will stop production will decrease, which will increase demand for raw materials. In addition, a shortage of scrap and rising prices for hot-rolled coils should also support the rebar market.

Supply of rebar on the Chinese market has recovered slightly since the beginning of September, up 0.1% – to $452.88 per tonne. At the same time, in August, the growth was 4.8%.

Rebar prices in China are rising despite the weakness of the construction industry. Actual demand is still low, but the market is preparing for an approaching seasonal increase in steel consumption. Sentiment is improving slightly as Chinese authorities introduce measures to support the real estate sector, which have little short-term but cumulative effect. An additional supporting factor is the expectation that the country’s authorities may soon lower interest rates. The expected economic stimulus measures are aimed at keeping China on track to achieve its 2024 GDP growth target of 5%.

In August, China’s rebar production fell to 2012 levels, reflecting market weakness, but will contribute to reduced product supply and higher prices.

-

02 July 2026

12 July 2026

12 July 2026

11 July 2026