News Global Market iron ore prices 1956 18 November 2022

Iron ore futures on the Dalyan Commodity Exchange for the week of November 11-18, 2022, increased by 5.6% compared to the previous week

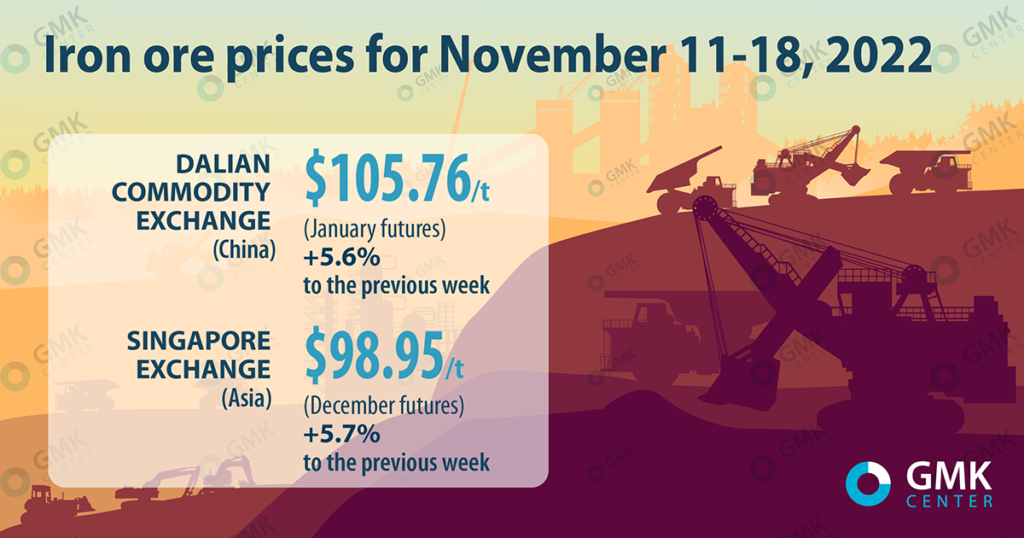

January iron ore futures on the Dalian Commodity Exchange for the week of November 11-18, 2022, increased by 5.6% compared to the previous week – to 753.5 yuan/t ($105.76/t). Thus, quotations of iron ore are increasing for the third week in a row. This is evidenced by the data of Nasdaq.

December iron ore futures on the Singapore Exchange rose in price to $98.95/t, which is 5.7% more compared to trading as of November 11, 2022.

Iron ore prices GMK Center

Iron ore prices have been rising for the past three weeks against the background of actions by Chinese authorities to support the economy amid the coronavirus epidemic. This significantly improves market sentiment and the outlook for iron ore demand.

Expectations that Beijing will implement more policy measures to support the economy after easing some restrictions due to COVID-19 and unveiling new measures to help the real estate sector, added to the buoyancy to the iron ore market.

China has adjusted its policy of zero spread of the coronavirus, which has caused significant damage to the economy, despite the rapid spread of the number of new infections. Softer quarantine rules gave market participants hope for an imminent end to tough restrictions.

In addition, the country’s central bank announced a tightening of monetary policy, intentions to stabilize employment and prices to accelerate economic growth. Against this background, prices for steel and other steel raw materials are rising, which also improves the outlook.

Despite the implementation of rescue measures by the government, there is still some uncertainty in the market about the long-term recovery of activity.

“The government’s recent actions to strengthen financing support for developers could improve the financial flexibility of companies and partially reduce their short-term pressure to refinance. But the impact will depend on the scale, duration and effectiveness of these measures,” notes Kelly Chen, vice president and senior analyst at Moody’s Investors Service.

Currently, market activity is based only on rumors about the improvement of the situation. Traders’ optimism may fade if the effect of the measures is not noticeable in the future. In addition, some steel plants are targeting production cuts and are preparing for winter capacity cuts.

“The stimulation of the construction sector in China can have a positive effect on the global steel market, at least in the short term. Rise in prices for both iron ore and steel products is probable. However, a long-term positive trend should not be expected, since the fundamental problems in the economies of the EU and the USA will not be resolved. These economies are headed for recession, while their central banks are unable to conduct monetary stimulus policies due to high inflation,” noted Andriy Glushchenko, GMK Center analyst.

As GMK Center reported earlier, in January-October 2022, steel companies of China reduced imports of iron ore by 1.7% compared to the same period in 2021 – to 97 million tons. In October, China imported 94.97 million tons of iron ore, which is 4.3% less y/y.

China is the largest producer of steel in the world. In 2021, Chinese steelmakers reduced steel production by 3% compared to 2020 – to 1.03 billion tons. In 2022, the country plans to continue reducing production.

-

Opinions Industry steel consumption

13 July 2026

24 July 2026

24 July 2026

24 July 2026