News Global Market iron ore prices 2023 22 September 2023

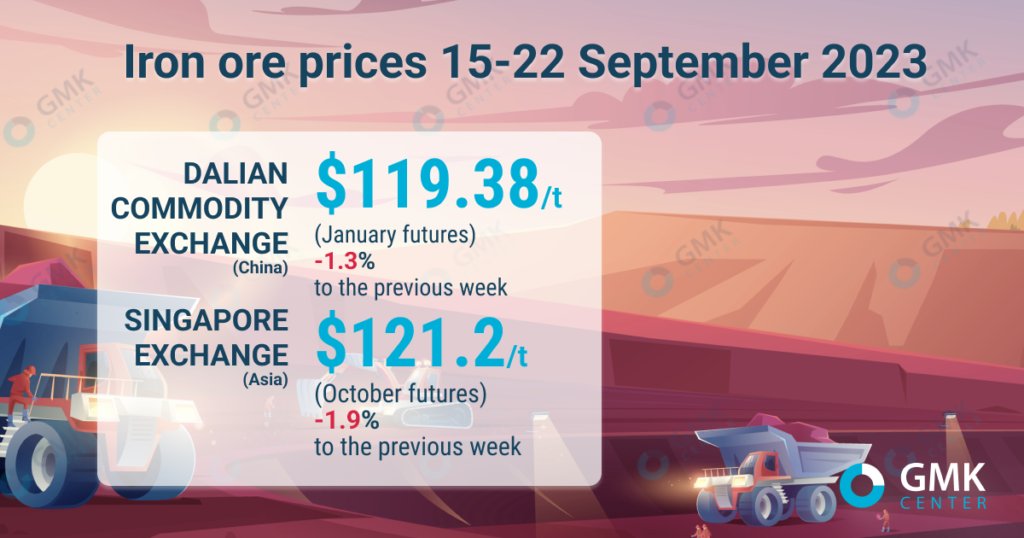

During September 15-22, iron ore futures on the Dalian Commodity Exchange fell to $119.4/t, and on the Singapore Exchange – to $121.2/t

January iron ore futures, the most traded on the Dalian Commodity Exchange, for the period September 15-22, 2023, fell by 1.3% compared to the previous week – to 871.5 yuan/t ($119.38/t ). This is evidenced by Nasdaq data.

As of September 22, 2023, on the Singapore Exchange, quotations of the underlying October futures decreased by 1.9% compared to the price a week earlier – to $121.2/t.

Iron ore prices reversed their uptrend last week, but still remain at high levels. Quotes have started to fall amid growing domestic supply of raw materials in China, while demand remains stable under the influence of uncertainty about sufficient demand for finished steel from the construction industry.

“We view last week’s decline in iron ore price levels as a normal correction after reaching the upper limit. It is risky to offer raw materials at high levels for a long time due to market control by the authorities,» commented Sinosteel Futures analyst Chen Peng.

Concerns about the real estate market still persist, despite a temporary improvement in the situation at the beginning of September, in particular the increase and simplification of lending.

Despite this, the Chinese authorities have pledged to accelerate the introduction of additional measures to speed up the economic recovery. During this month, iron ore prices were held at a high level thanks to the implemented incentives from the authorities, but their effect is probably waning. For now, the general sentiment remains cautious.

«China’s real estate market continues to fall and remains the biggest uncertainty in the economy,» Mysteel points out.

A sharper drop in prices is avoided thanks to still low raw material stocks at steel mills and the need to replenish them ahead of China’s National Day (September 26-October 6).

Iron ore prices are likely to hold above $115/t until the end of September, but with the start of the national holiday demand for the raw material will again slow down and put pressure on prices. Further prospects will depend on the effectiveness of the authorities’ actions to support and stimulate the economy.

As GMK Center reported earlier, the rating agency Fitch Ratings recently reviewed the price forecast for iron ore in 2023 towards growth – up to $110/t compared to $105/t in the previous forecast. Forecasts for 2024-2026 remained unchanged – $85/t, $75/t and $70/t, respectively.

Investment bank Goldman Sachs in August revised its forecast for iron ore prices for the second half of the current year to decrease – by 12%, to $90/t. This is due to a forecast iron ore oversupply of 68 million tonnes and a decline in steelmaking in China. At the same time, ING analysts expect prices for this raw material to be at $105/t in the third quarter, and $100/t – in the fourth.

-

Opinions Industry steel consumption

13 July 2026

27 July 2026

27 July 2026

27 July 2026