News Global Market rebar prices 4377 05 December 2023

Prices were supported by the increase in production costs, in particular due to the increase in the cost of scrap and iron ore

In November 2023, global prices for rebar increased in most global markets, particularly in Turkiye and China. Prices were supported by the rapid increase in the cost of raw materials and rising production costs. At the same time, real demand was weak. In December, the growth trend is likely to slow down as winter holidays approach and activity in most markets slows.

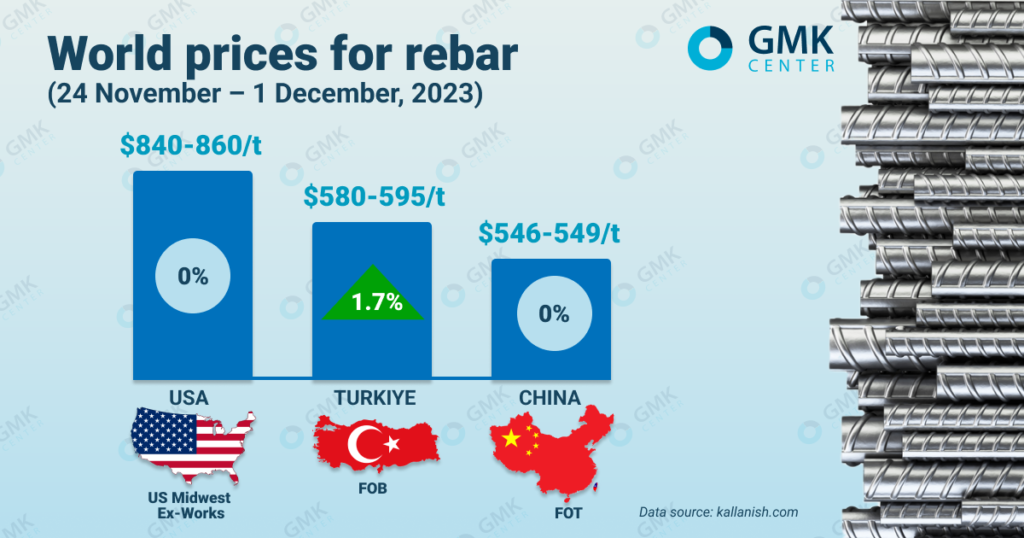

Prices for rebar in Turkiye for the week of November 24 – December 1, 2023, increased by 1.7% or $10/t compared to the previous week – to $580-595/t FOB. In November, prices for Turkish rebar increased by $35/t or 6.2%. Currently, rebar quotations on the Turkish market have reached their highest level since the beginning of July 2023.

The positive trend in the Turkish rebar market has been maintained since the end of October. The rise in prices is to some extent due not to the growing demand for long products but to the dependence of prices for steel products on rising scrap prices.

At the beginning of the month, Turkish rebar producers continued to meet export demand for rebar, especially in Eastern and Western Europe, as North African suppliers largely withdrew from the market due to the exhaustion of EU quotas and full order books.

At the same time, Turkiye’s main export markets, Israel and Yemen, have stopped purchasing due to the military actions. These countries are not expected to re-enter the market in the near future. In addition, the situation in Yemen is likely to affect the supply of products to Ethiopia, which has become an important market for Turkish producers this year, as well as Djibouti.

In the second half of November, demand for Turkish rebar began to decline as consumers found prices unacceptable. At the same time, demand from the EU, West Africa and Central America was sufficient to compensate for the loss of Israeli volumes.

Although demand does not show positive signs for the last quarter of 2023, most market participants still believe that prices will remain high due to increased production costs for steelmakers, in particular due to the high cost of raw materials and the expected increase in energy tariffs.

At the end of the month, Israel resumed purchases of rebar from Turkiye, which gave a positive boost to the market. The volumes are expected to grow to cover the lack of deals for most of November. Yemen, an important export destination for Turkiye, has also resumed activity. At the same time, demand in the EU has dropped significantly as winter holidays approach.

Thus, by the end of the year, prices for Turkish rebar are likely to stabilize or grow slightly as Israel and Yemen resume purchases. This will support the demand from these countries that was lost in November and cover the decline in activity in the EU and the US.

In the US, rebar prices remained unchanged from November 24 to December 1, 2023, at $840-860/mt Midwest Ex-Works, compared to the previous week. At the same time, the quotes decreased by $40/t or 4.4% over the month.

Rebar prices in the US began to decline in mid-November and stabilized at the end of the month as winter approached and demand declined. Construction in different states of the country is stagnating, but in the regions of the sunny belt has somewhat intensified. At present, the main support for long products prices may come from higher scrap prices. So far, scrap prices have not contributed to the growth of rebar prices, but they have contributed to market stability.

Market participants expect rebar prices to potentially rise in December and possibly in January as local mills try to influence the market. The increase will be driven not by any particular optimism about demand, but by rising scrap prices in the US.

However, some regions may indeed see higher demand for rebar, particularly in the Sun Belt, where construction continues in winter. If the southeastern US mills initiate price increases, the Midwest mills will also have a stronger basis for doing so.

In China, rebar prices also remained unchanged over the past week at $546-549/t FOT Warehouse. In November, the price level increased by $27/t or 5.2%.

Rebar prices in China have stabilized amid limited demand. Steel producers do not risk raising prices in order not to lose current sales volumes as they approach the seasonal decline in market activity.

Market participants expect that demand for long products will not recover during the winter and will remain low. If steel prices remain stable for a long period, some traders are likely to postpone purchases until the Spring Festival in 2024, as they did last year, or skip the winter stockpiling altogether.

As GMK Center reported earlier, in January-October 2023, Ukraine exported 428.34 thousand tons of long products worth $327.82 million. Revenues from sales abroad decreased by 48.8% year-on-year, while exports decreased by 35.3%.

-

02 July 2026

12 July 2026

12 July 2026

11 July 2026