News Global Market rebar prices 4963 07 April 2026

Some manufacturers even temporarily suspended sales to avoid operating at a loss

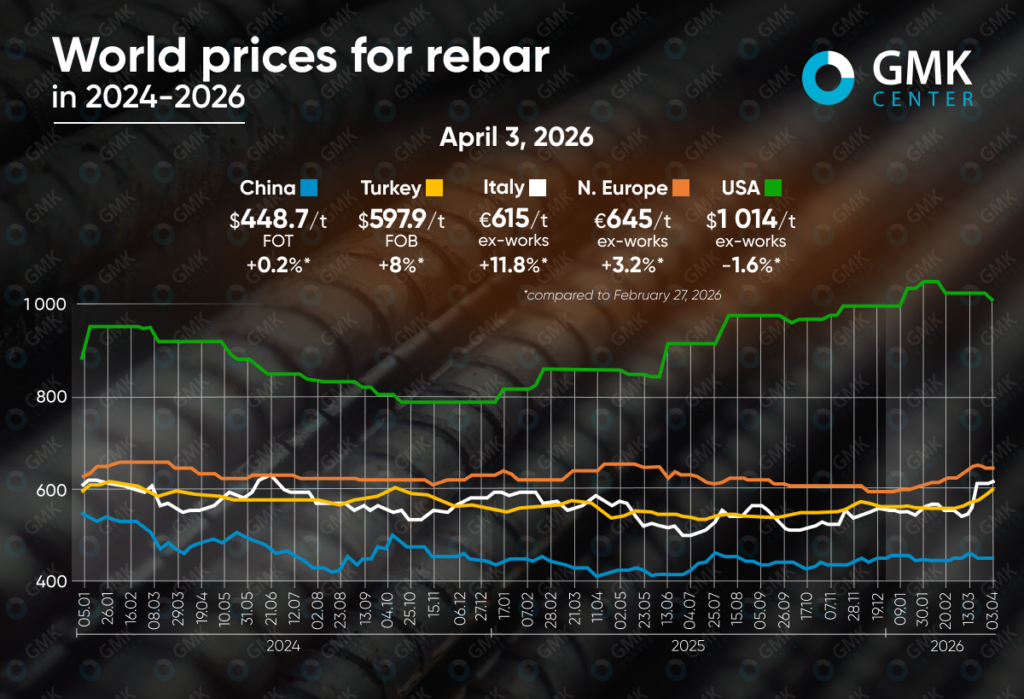

In March 2026, the global rebar market showed mixed trends depending on the region. The most significant price increases were observed in the EU and Turkey, while prices fell in the U.S., and the Chinese market remained virtually unchanged.

Turkey

Turkey’s rebar market rose by 8% between February 27 and April 3, reaching $597.9/t FOB—the highest level since February 2024.

In Turkey, the March price increase was primarily driven by rising costs, particularly higher prices for energy, scrap, freight, and insurance amid the war in the Middle East. An additional factor was the reduced availability of competitively priced imported billets.

Domestic demand was uneven but periodically picked up due to fears of further price hikes. Kardemir’s behavior served as a key indicator: the company raised prices several times and quickly sold off available volumes. At the same time, buyers’ financial constraints held back a more active recovery in trade.

In foreign markets, Turkish producers gradually improved their pricing positions, particularly due to weaker competition from China and Egypt. Demand came from the EU, the Balkans, Africa, and certain countries in the Americas.

In the near future, prices may stabilize above $600/t FOB if pressure from raw materials and energy does not ease and buyers remain willing to accept higher offers.

EU

In the EU, rebar prices rose in March to above their annual highs. In Northern Europe, prices reached €645/t ex-works, up 3.2% from the previous month, while in Italy they reached €615/t ex-works (+11.8%).

The European market experienced a sharp price surge in March, driven primarily by a cost shock. Following the escalation of tensions in the Middle East, prices for gas, electricity, and transportation rose significantly, with scrap prices following suit. Against this backdrop, some producers temporarily halted sales to adjust prices and avoid operating at reduced margins.

In Northern Europe, mills acted in a fairly coordinated manner. Supply was limited, and new prices were pushed through due to low sales volumes. This created a sense of scarcity and reinforced expectations of further price increases. The Italian market moved even more sharply, but there the price increases increasingly clashed with consumers’ actual purchasing power.

The construction sector in Italy remained weak, and distributors avoided large purchases, operating primarily on a spot basis. Part of the demand was covered entirely by existing inventories.

In the short term, prices in the EU are likely to remain high, but further growth will become increasingly difficult to achieve without a real improvement in demand, especially in the Italian market.

United States

The U.S. market was the only major market where prices fell in March—by 1.6%, to $1,014.1/ton.

Unlike Europe and Turkey, the U.S. rebar segment appeared weaker in March. For most of the month, prices remained largely unchanged, but began to decline toward the end of the period. The main reason was insufficient demand. New projects were launched slowly, and a significant portion of purchases amounted to minimal restocking.

Additionally, the market was pressured by expectations of cheaper scrap in April. This weakened the case for maintaining previous prices and made the market more favorable for buyers.

However, a deeper decline did not occur. Support came from tariffs and other trade barriers, a relatively weak presence of imports, as well as high energy and logistics costs. At the same time, mills maintained fairly stable capacity utilization.

In the coming weeks, the U.S. market will most likely remain in a mode of cautious decline or sideways movement. Weak demand and softer scrap prices will put pressure on prices, but a sharp collapse is not expected yet.

China

In China, rebar prices rose by 0.2% in March, reaching $448.71/ton.

The Chinese market appeared to be the calmest among key regions in March. After a moderate rise at the beginning of the month, prices gradually lost momentum, and overall, the period ended virtually unchanged. Early support came from government signals regarding infrastructure stimulus, temporary production restrictions, as well as rising raw material and energy costs.

However, the market’s underlying fundamentals remained fragile. The post-holiday recovery in construction was slow, the situation in the real estate sector offered little cause for optimism, and inventory levels remained substantial. That is why, even against a favorable news backdrop, sellers found it difficult to achieve a full-fledged price increase.

This became particularly evident in late March—to revive trading, traders were already having to concede on price.

In the short term, the baseline scenario for China appears to be a narrow range of fluctuations with slight downward pressure. Inventories are gradually declining, but demand still does not provide the market with sufficient support for a sustained recovery.

-

15 June 2026

23 June 2026

23 June 2026

23 June 2026