News Global Market electricity prices 6895 07 April 2023

European gas storage capacity remained high after the winter

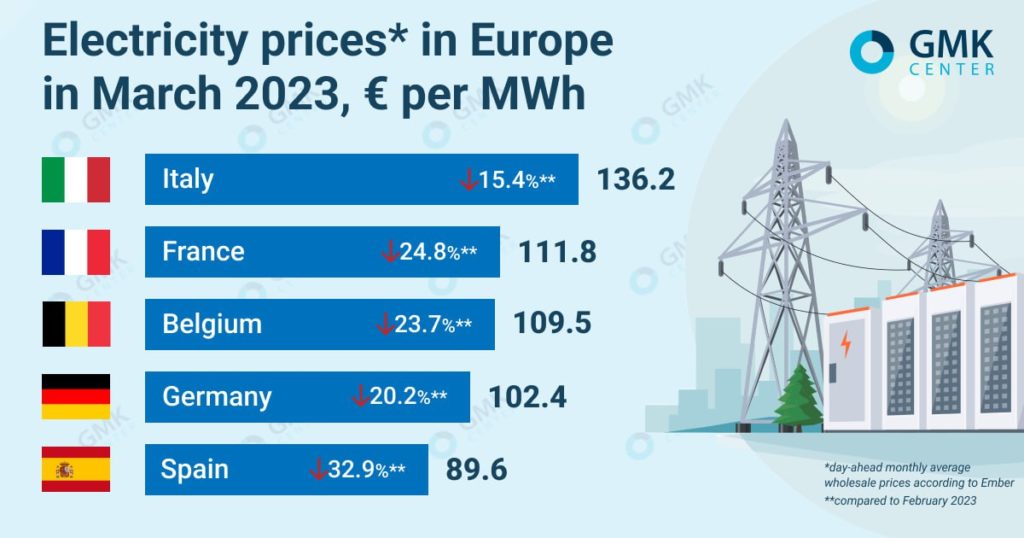

Prices. In March 2023, compared to February, the average monthly day-ahead electricity price in most European countries, with some exceptions, slightly exceeded €100 MWh.

In the EU, average monthly wholesale prices for the day ahead, according to Ember, in March were as follows:

- Italy – €136.2/MWh;

- France – €111.8/MWh;

- Germany – €102.4/MWh;

- Spain – €89.6/MWh;

- Belgium – €109.5/MWh.

In the UK, according to Nordpool, the monthly average day-ahead spot price in February was €130.8/MWh.

Electricity prices in the EU in March, GMK Center

According to AleaSoft Energy Forecasting analysis, in the first quarter of 2023, the average quarterly price remained below €130/MWh in most European markets except for France, the UK and Italy. The lowest quarterly price – €85.23/MWh – was registered on the Nord Pool market of the Scandinavian countries.

Compared to the previous quarter, in the first quarter of 2023, average prices decreased on all European electricity markets. The largest drop – by 40% – was recorded in the German market, and the smallest – 14% and 15% – in Portugal and Spain, respectively. In the UK, prices fell by 26% q/q in this period, in France – by 39% q/q.

A drop in average prices in the first quarter of 2023 was also observed on an annual basis, in particular, in Spain – by 58%, in France – by 44%.

The decrease in electricity prices in the first quarter of 2023 compared to the previous year was facilitated by a general increase in the production of renewable energy (solar, wind) and a drop in demand.

France. According to S&P Global, France, despite the reduction in nuclear power capacity in March (it fell by 19% in the period, according to system operator RTE), was mainly a net exporter of electricity, supplying it to Italy, Switzerland and the UK. Ongoing strikes in the country affected the production of electricity.

At the end of February and in March, the energy generating company EDF announced the discovery of new corrosion cracks at three reactors. Subsequently, the French Nuclear Safety Authority (ASN) recommended that EDF review its control strategy. The market is still awaiting an updated maintenance plan and annual generation, but the situation has already affected forward contracts. For the first quarter of 2024, in the first days of April, it closed at a price above €400/MWh.

United Kingdom. British businesses will once again face pressure on energy prices as a government scheme capping the cost of energy for businesses ended on 31 March. The new Energy Bills Discount Scheme offers discounts on the wholesale price of electricity, including for energy-intensive industries. It will be valid until April 2024.

In the Spring Budget 2023, Chancellor Jeremy Hunt set out a series of measures to ease the impact of high energy prices on households and businesses. However, it did not offer an additional short-term solution for businesses. At the end of February, the government proposed scheme British Industry Supercharger, designed to bring electricity costs for key industries in line with prices in other major economies. Within its framework, support was promised to energy-intensive sectors such as steel and the chemical industry. However, the mechanisms and timing of the implementation of the scheme have not yet been finalized, and support will begin only in the spring of 2024.

Spain. Meanwhile, Spain and Portugal continued the Iberian model until the end of 2023. This mechanism limits the price of natural gas for electricity generation, and was supposed to expire in May 2023. The proposal by the two countries foresees a new increase in the price of gas for electricity generation from €55/MWh in March to a cap of €65/MWh in December, with a monthly increase of €1.10/MWh.

Gas. As predicted, the gas storage capacity of the EU countries remains high. According to of the AGSI platform, as of April 1, 2023, this indicator was 55.7% in the EU as a whole. Europe came out of the winter in better shape than expected. However, experts point to the approach of the summer season, which is key for filling gas storages.

Europe is currently increasing investments in new LNG import capacity and exploring new opportunities for gas imports. However, the market remains difficult. In particular, increased demand for liquefied gas from China and competition for fuel from Asian economies may lead to an outflow of cargo from the European market.

Analysts are concerned that Europe has not made enough progress on long-term contracts for LNG because of its climate policy, and it will come from the spot market, where prices are much higher, which could affect next winter.

In 2022, Europe increased the import of this fuel by 60% y/y – up to 121 million tons, writes Reuters. At the same time, according to the International Energy Agency, the value of LNG imports increased more than three times last year to approximately $190 billion. According to analysts, in 2022 Europe accounted for more than a third of global deals on the spot market. If no long-term contracts are concluded, in 2023 this indicator will reach more than 50%.

As GMK Center reported earlier, the review of the structure of the electricity market of the European Union needs a deeper and more complex approach, according to the Association of European Steel Producers (EUROFER). The European Commission published a proposal on the reform of the electricity market design on March 14. The reform aims to expand the role of long-term instruments such as power purchase agreements (PPAs).

-

02 July 2026

02 July 2026

02 July 2026

02 July 2026