News Global Market coking coal prices 3974 01 November 2024

Traders doubt the long-term effect of Beijing's stimulus policy

The coking coal market has shown some optimism since the end of September amid the stimulus announced by Beijing, but is in a state of uncertainty at the end of the current month.

On August 23, Australian high-quality coking coal prices fell below $200/t FOB for the first time in a year and remained below that level for five weeks.

At the end of September, after the announcement of a series of economic incentives by China, prices for these raw materials, as well as for iron ore, began to rise. Sentiment on the market has improved, however, the nature of the measures announced has made traders doubt that their effect will be long-term.

In addition, the coking coal market was still oversupplied and weak in demand. Trading activity during the specified period was insignificant – Chinese buyers did not show much activity on the eve of the autumn national holiday – Golden Week (October 1-7).

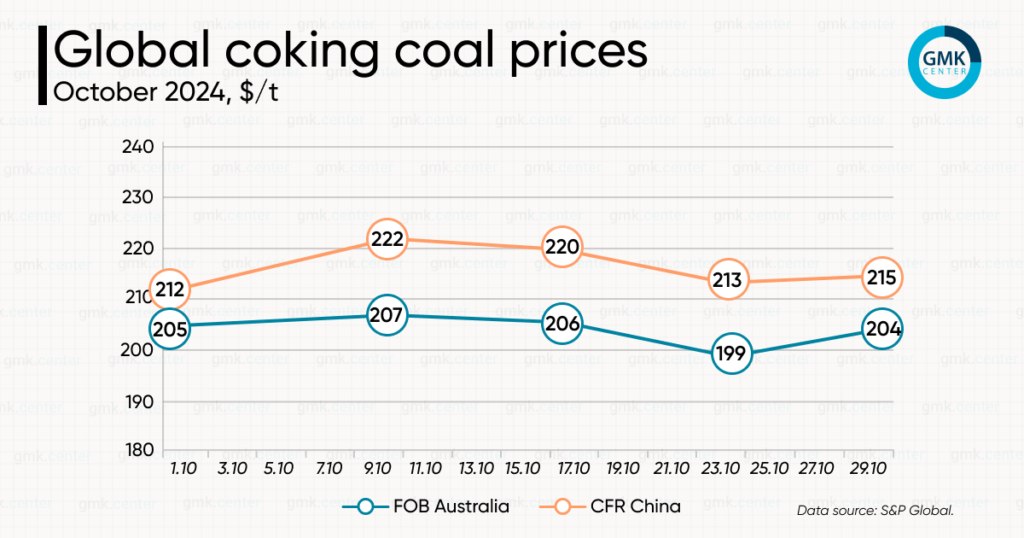

As of October 1, quotes for Australian coking coal (FOB Australia), according to S&P Global, were $204.75/t (+8.3% compared to the previous week), prices for this raw material in China (CFR China) were $212/t (+3.9%).

At the end of October, the market remained uncertain about the further dynamics of coking coal prices. Demand for this commodity in India is expected to improve after the Diwali holiday. In the fourth quarter, it may also be affected by the recovery of the Chinese market.

Buyers from China remain inactive for sea freight as the ports have stocks at lower prices. In addition, both consumers and traders are waiting for the meeting of the legislative body of the People’s Republic of China, which should take place on November 4-8.

As of October 30, quotes for Australian coking coal (FOB Australia) returned to $204/t (+2.5% to the previous week), prices for this raw material in China (CFR China) were $215/t (+1.2%).

The market is also paying attention to the latest figures from India and China. In September, these countries recorded a drop in steel production by 0.2% and 6.1% year-on-year, respectively.

Initial announcements of China’s economic stimulus raised some expectations, but confirmation of these moves is important for now.

In the six months of the 2024/2025 fiscal year (April-September), coking coal imports into India amounted to 29.6 million tons, reaching a six-year high. The country’s metalworking plants continued to import coal from the Russian Federation, reducing purchases from Australia.

In September, China reduced coking coal imports for the second month in a row, these volumes fell by 3.1% m/m. and 4.1% year-on-year to 10.4 million tons. Coke production in the country has been falling for three months in a row. On October 24, after several increases, the country began the first round of a new reduction in coke prices due to the reduction of metal mills’ margins and the reduction of coking coal prices.

As GMK Center reported earlier, in September it was expected that at the end of the fourth quarter of 2024 and in the first quarter of 2025, coking coal prices will stabilize and start to rise to $220-240/t.

-

02 July 2026

03 July 2026

03 July 2026

03 July 2026