News Global Market hot-rolled prices 2503 14 June 2026

The Chinese and US markets saw a slight increase in average prices

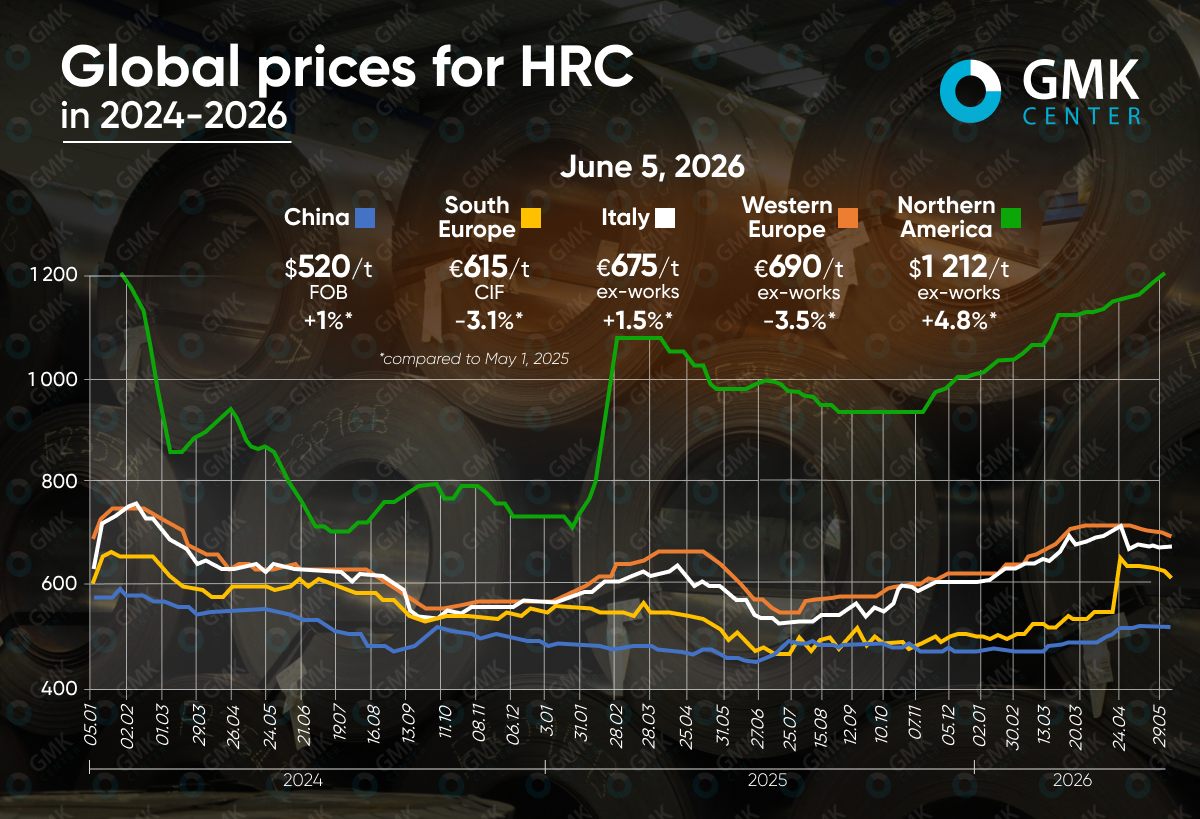

Global prices for hot-rolled coils showed mixed trends in May. In the European market, average monthly offers fell by 2–4%, whilst in China and the US there was a slight increase of 3–4%.

EU

In Europe, average prices for hot-rolled coils fell in May: in Western Europe by 1.8% to €690/t ex-works, and in Italy by 3.9% to €675/t ex-works. At the same time, imported products in Southern Europe rose in price by 10.1% — to €629/t CIF. Comparing prices as of 5 June with those on 1 May, they fell by 0.7% in Western Europe to €690/t ex-works, remained unchanged in Italy (€675/t ex-works), and dropped by 1.6% in Southern Europe to €615/t CIF.

The main feature of the European market in May was extremely low buyer activity. Despite the absence of sharp price fluctuations, service centres and distributors operated mainly at minimal volumes, purchasing steel only for current needs. The situation remained particularly difficult in Italy, where demand had virtually stalled and companies focused on reducing accumulated stocks.

Additional uncertainty was created by the anticipation of a new mechanism for allocating import quotas and the launch of updated EU trade rules from July. Significant volumes of previously imported rolled steel, the impact of CBAM and uncertainty regarding future rules held back the signing of new contracts. At the same time, producers attempted to maintain price levels, citing rising costs for energy, raw materials and logistics, which were further exacerbated by geopolitical tensions in the Middle East.

In the North-West European market, prices largely stabilised following the April correction. Competition between service centres, willing to operate on minimal margins to maintain sales, prevented producers from implementing more ambitious pricing strategies.

The situation is expected to change after the summer, when accumulated stocks are reduced and new trade restrictions begin to have a more significant impact on the market. This creates the conditions for a moderate price increase in the autumn.

USA

In the US market, average product prices for May rose by 3.2% month-on-month to $1,175.6/t ex-works. Comparing the figure as at 5 June with that of 1 May ($1,212.5/t), it increased by 1.1%.

Unlike Europe, the US market continued to show a steady upward trend. The growth was supported by limited availability of spot volumes and an aggressive pricing policy by steelmakers. Seasonal plant maintenance had a significant impact, causing delivery dates to shift to July–August and forcing buyers to reserve products in advance.

Favourable market conditions also persisted on the demand side. Producers and distributors reported stable sales of hot-rolled, cold-rolled and galvanised steel, whilst strong industrial production figures only reinforced market participants’ optimism. Nucor also played a significant role, setting the tone for the entire market with several consecutive increases in its official prices.

It was only towards the end of the month that the first signs emerged that the rise in US steel prices could stimulate an increase in imports. So far, this factor has had no significant impact, but in the long term it could intensify competition and limit further growth.

In the coming months, prices are likely to remain high due to sufficient demand and seasonal plant downtime. At the same time, as import supply increases and market supply gradually improves, the pace of price rises may slow down.

China

In China, average rolled steel prices rose by 4.1% month-on-month in May, to $519/t FOB. Comparing prices as at 5 June with those of 1 May, they rose by 1% to $520/t FOB.

For the Chinese market, May was a month of sharp shifts in sentiment. Following the Labour Day celebrations, prices quickly rose to their highest levels in nearly a year and a half, driven by positive macroeconomic expectations and high-cost coking coal. However, within a few days this momentum faded, and the market entered a gradual correction.

The turnaround was a result of deteriorating fundamentals. Production was growing faster than demand, causing HRC stocks to build up whilst apparent consumption was falling. Concerns about the seasonal summer slowdown only reinforced the pessimistic sentiment and forced exporters and traders to revise their price offers.

The external market also failed to provide support. Buyer activity in Vietnam and other Asian countries remained weak, whilst competition among Chinese suppliers intensified due to low-cost offers and the use of VAT-free schemes, which made it difficult to establish stable export prices.

In the near term, the market is likely to remain under pressure from oversupply and weak demand. Local support may come from changes in raw material prices or new economic stimulus measures, but without an improvement in consumption, it is difficult to expect a significant rise in prices.

-

02 July 2026

03 July 2026

03 July 2026

03 July 2026