Infographics EU 617 09 March 2026

Import volumes are recovering after weaker dynamics in previous years

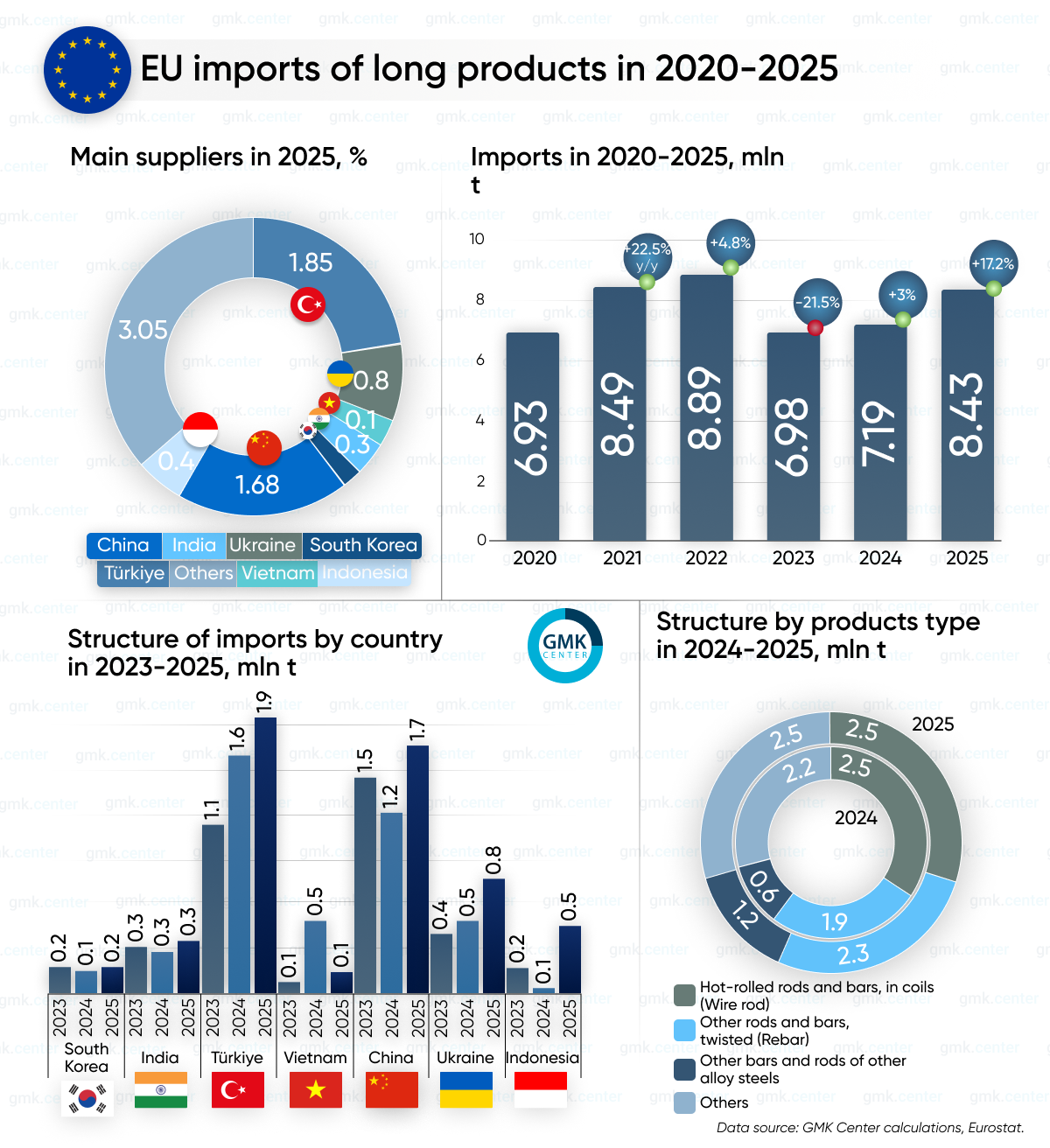

In 2025, 8.43 million tons of long steel products from third countries were shipped to the EU market, which is 17.2% more than in 2024. This growth indicates a gradual recovery in demand from the construction and engineering sectors in the bloc’s countries.

The largest volumes of supplies are hot-rolled bars and rods in coils (HS 7213) – 2.49 million tons compared to 2.47 million tons a year earlier (+0.6% y/y). Another 2.29 million tons of imports are other carbon steel bars and rods (HS 7214). This is 22.1% more than in 2024.

The top three commodity categories also include other bars and rods of other alloy steels; hollow bars and rods for drilling of alloy or non-alloy steels (HS 7228) – 1.19 million tons (+84.8% y/y). At the same time, imports of angles, shapes, and special profiles of non-alloy steel (HS 7216) increased to 755,150 tons, which is 11.4% more y/y.

Turkey remained the main supplier of long products to the EU market in 2025. Supplies from this country reached 1.86 million tons, up 15.6% year-on-year. Exports were dominated by other carbon steel bars and rods, without further processing, twisted (HS 7214) – 575.4 thousand tons (+36% y/y), as well as hot-rolled bars and rods, made of carbon steel, in coils (HS 7213) – 473.9 thousand tons (-0.8% y/y).

A significant increase in exports was recorded from Ukraine. In 2025, Ukrainian producers supplied 768.4 thousand tons of long products to the EU, which is 60.1% y/y more. The main commodity items were hot-rolled bars and rods, made of carbon steel, in coils (HS 7213) – 361.7 thousand tons (+53.7% y/y) and other bars and rods of carbon steel, without further processing, twisted (HS 7214) – 252.6 thousand tons (+270.7% y/y).

Among Asian suppliers, China plays a key role, increasing its exports to the EU to 1.68 million tons in 2025, up 40.5% year-on-year. The bulk of Chinese exports consisted of other bars and rods of other alloy steels; hollow bars and rods for drilling of alloy or non-alloy steels (HS 7228) – 581.03 thousand tons (+58.3% y/y), as well as other bars and rods of carbon steel, without further processing, twisted (HS 7214) – 379.79 thousand tons (+29.9% y/y).

In 2025, India increased its exports of long products to the EU by 28% y/y, to 342.1 thousand tons. The bulk of the supplies consisted of other bars and rods, angles, shapes, and special profiles of corrosion-resistant steel (HS 7222) – 190.64 thousand tons (+25.7% y/y), as well as corrosion-resistant steel wire (HS 7217) – 56.57 thousand tons (+13.3% y/y).

Indonesia showed particularly sharp growth. In 2025, its exports of long products to the European Union increased more than 13 times, to 450.9 thousand tons (+1222.9% y/y). Almost the entire volume consisted of hot-rolled bars and rods made of carbon steel in coils (HS 7213) – 445.8 thousand tons (+1387.6% y/y), while the second largest segment remained corrosion-resistant steel wire (HS 7223) – 5.0 thousand tons (+24.9% y/y).

Vietnam, on the other hand, significantly reduced its supplies. In 2025, exports to the EU decreased by 72.2% y/y – to 131.7 thousand tons after a sharp increase a year earlier. The main product categories remained hot-rolled bars and rods made of carbon steel in coils (HS 7213) – 97.99 thousand tons (-78.8% y/y), as well as other bars and rods of carbon steel, not further worked, twisted (HS 7224) – 20.44 thousand tons (0.7 thousand tons in 2024).

«European producers have the strongest chance of fully replacing imports in the long-rolled segment. On the one hand, the EU has sufficient spare capacity for this, and on the other hand, the СВАМ makes it practically impossible to import long-rolled products produced by BF-BOF. We will see in the near future how much European steel producers will be able to increase the utilization of their capacities,» comments Stanislav Zinchenko, CEO of GMK Center.

In general, the increase in imports of long products indicates that the European market remains dependent on external suppliers, particularly in the construction steel segment. High energy costs and the limited competitiveness of some producers in the EU continue to stimulate demand for imported products.

-

15 June 2026

22 June 2026

18 June 2026

17 June 2026