Posts Global Market steel consumption 1050 10 March 2026

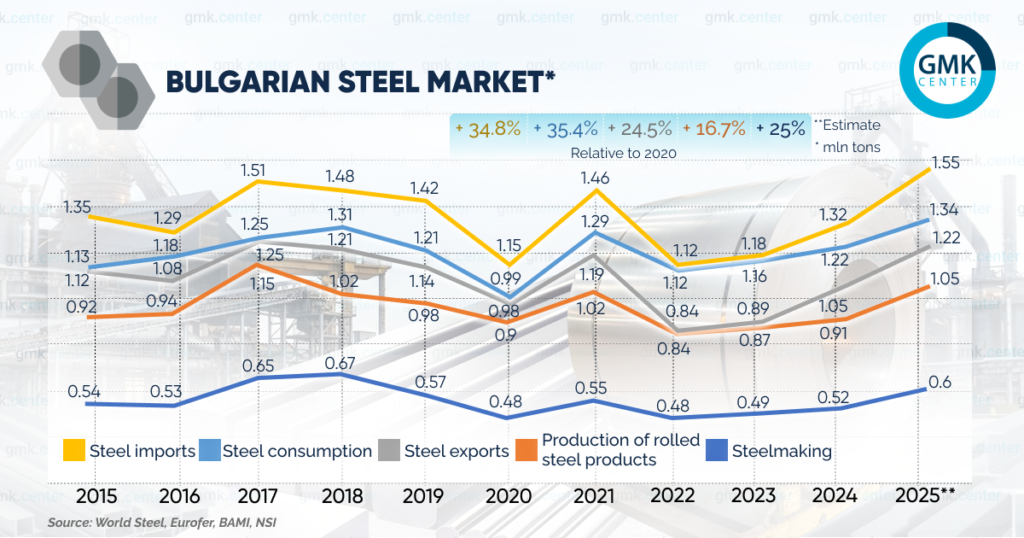

Demand for steel in the country is currently at its highest level in 11 years

The construction and engineering industries in Bulgaria successfully adapted to the European economic crisis of 2022–2023 caused by the surge in energy prices. It can be said that they were hardly affected by it. Consumption of finished steel remained high here even when other EU countries experienced a sharp decline. This is what makes the Bulgarian market case unique.

Market profile

Virtually all steel in Bulgaria is smelted at a single plant — the Stomana Industry EAF plant in Pernik, which is part of the Greek Viohalco group. It is the only manufacturer of thick sheet steel in the region, which is in high demand in shipbuilding and mechanical engineering. This plant was particularly affected by the rise in gas and electricity prices in Europe, as can be seen from the dynamics of steelmaking production.

At the end of 2024, the Bulgarian government introduced compensation for high electricity prices for energy-intensive enterprises, which enabled Stomana Industry to increase its production capacity. The plant periodically purchases imported billets when order volumes exceed steelmaking capacity.

Another major producer is the Promet Steel rolling mill in Burgas, which is owned by the Ukrainian Metinvest Group. It operates entirely on imported billets and specializes in rebar and wire rod. The plant’s annual capacity is up to 800,000 tons.

The presence of such a large rolling mill, together with Stomana Industry’s strategy, makes Bulgaria a rolling hub for Southeast Europe. It mainly imports semi-finished steel products and exports finished rolled products.

The small Helios-Metalurg rolling mill in Plovdiv produces rebar and wire. Its customers are local construction companies.

Stomana Industry and Promet Steel export significant volumes, up to 70% of their production. Rebar and wire rod account for approximately 60-65% of Bulgaria’s total steel exports, while thick plate accounts for approximately 20%. The main export destinations for long products are Romania, Serbia, North Macedonia, and Hungary, while sheet products are mainly exported to Germany and Greece.

Sanctions against Russian steel companies and the Belarusian Iron and Steel Plant have enabled Bulgarian players (especially Stomana Industry) to fill their niche in Central European countries. Steel and rolled steel production in Bulgaria is growing, and with it, exports.

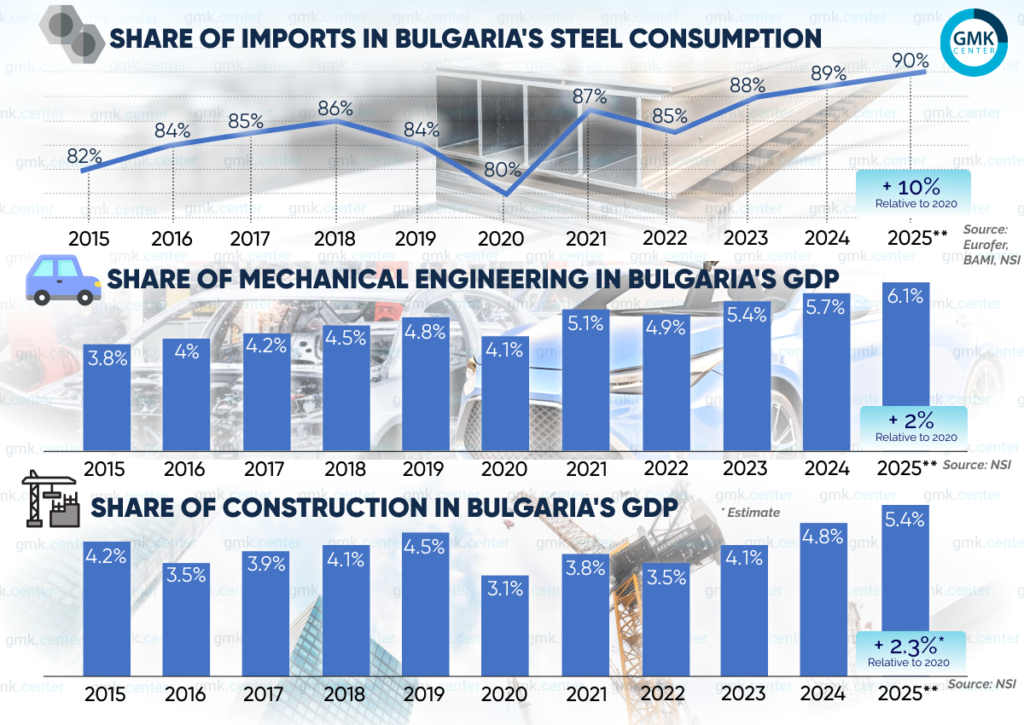

The increase in foreign shipments by Bulgarian manufacturers amid growing domestic demand is forcing local consumers to purchase more and more imported rolled products. Bulgaria does not produce the hot-rolled and cold-rolled coils needed for mechanical engineering. It also does not produce the painted and galvanized rolled products used in construction. In these segments, imports account for 100% of the market, with the main supplies coming from Turkey, Italy, and Romania.

Demand for flat rolled products

Unlike the Baltic states and Moldova, Bulgaria has managed to preserve its Soviet legacy of heavy engineering. The UNITRAF, BULTRAF, ZA VN-Dobrich, and Elprom Heavy Industries (formerly Vasil Komarov) plants manufacture transformers.

The M+S Hydraulic, Caproni, HidroPnevmoTehnika, Industrialtechnic, Haskovo Hydraulics, and Badestnos factories located in Kazanlak specialize in the production of hydraulics and pumps. Bulgaria is one of the world leaders in this field. Balkancar, a large manufacturer of forklifts, is one of the companies that has survived since Soviet times.

In the 2000s, European automotive companies began to transfer the production of auto components to Bulgaria. Now, 9 out of 10 passenger cars assembled in the EU have parts manufactured in Bulgaria. The country is also one of the five largest bicycle manufacturers in the European Union. This explains the higher share of mechanical engineering in the structure of steel consumption.

Bulgaria’s machine building industry has not experienced a recession or downturn for 11 consecutive years. The growth in orders from NATO for hydromachine companies and stable market positions (Bulgarian hydraulics are used in Deere&Co agricultural machinery, TM John Deere) are the secrets to the industry’s stability.

The specifics of transformer manufacturing should also be taken into account. The order portfolio here is formed several years in advance, so production dynamics are almost independent of the current economic situation.

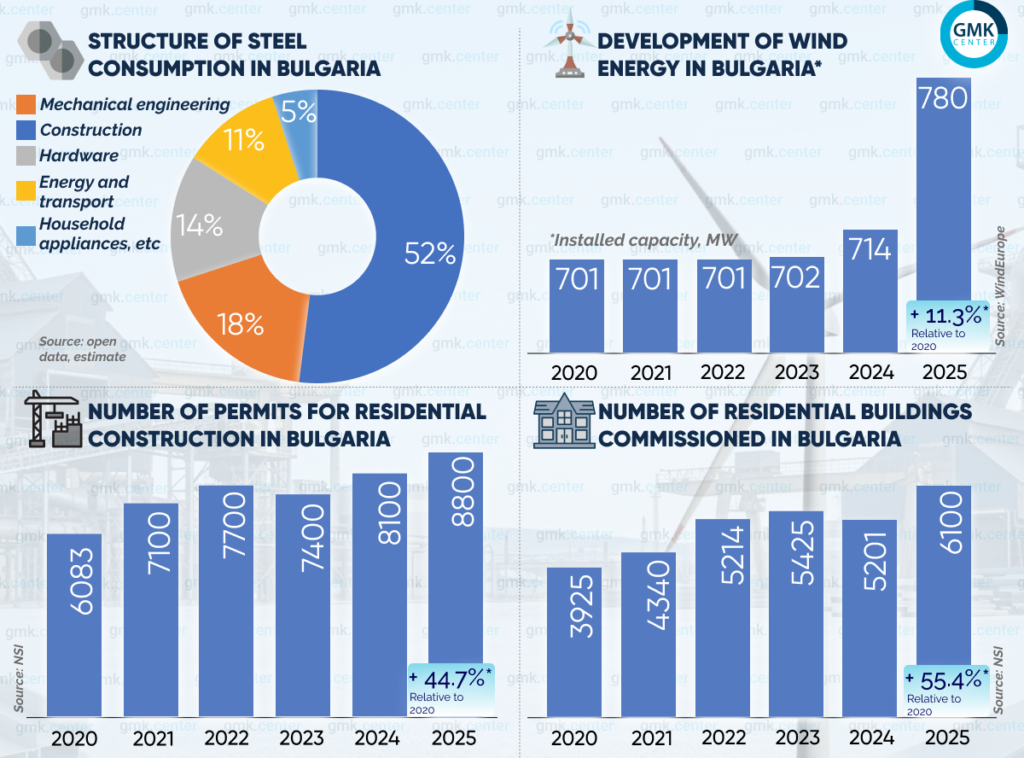

Bulgaria’s wind energy sector was on hold in 2020–2025 due to regulatory barriers. Obtaining all the necessary permits for the construction of wind farms took 5–7 years, so investors switched en masse to solar generation.

The resumption of growth in 2025 was linked to the start of the modernization of existing wind farms—the replacement of old 0.8–1 MW turbines with modern 4–6 MW ones. This also contributed to an increase in demand for flat rolled products.

The main suppliers of wind turbines for Bulgarian wind farms are Denmark’s Vestas, America’s GE Renewable Energy, and Germany-Spain’s Siemens Gamesa, meaning that replacing the equipment will have no impact on steel sales in Bulgaria. However, new, taller wind towers need to be built for them. Such structures are manufactured at Bulgarian steelworking plants in Ruse and Radomir according to the specifications of Vestas and other companies. Rolled steel is also needed to build new foundations for the towers.

Additional demand for flat rolled products is generated by the highly developed network of SSC steel service centers in Bulgaria. These enterprises purchase hot-rolled coils, cut them into finished sheets, which are then used by other factories to manufacture steel furniture (cabinets, racks). These products are then exported to the EU.

Demand for long-term rentals

The Bulgarian residential construction market is unique. The country has one of the highest rates of home ownership in the European Union – 86.1%. The volume of work performed and, accordingly, the demand for long-term rentals are growing year by year.

There is an explanation for this phenomenon. The stock market in Bulgaria is underdeveloped, and deposit rates are close to zero. Investing in residential real estate in such conditions is practically the only way to preserve savings, which is why Bulgarians are actively investing in “concrete.”

Bulgarian banks are overflowing with liquidity, which is why they are very active in issuing mortgage loans. Interest rates on these loans remain low – 2.6–3.5% in leva compared to 4–5% in euros.

The transition to the euro became one of the main drivers of investment in real estate in 2023–2025. Bulgarians took out cheap loans in the national currency to purchase “hard” assets (real estate) before the final entry into the eurozone (from January 1, 2026). As a result, according to realtors’ estimates, up to 25–30% of apartments in new buildings in Sofia are unoccupied — they are simply instruments for preserving funds.

It should be noted that the existing housing stock in Bulgaria consists mainly of prefabricated buildings constructed in 1960–1980. New residential construction often involves the demolition of these old buildings. A significant portion of Bulgarians work in other EU countries, and their savings drive demand for modern, comfortable housing.

Since 2023, the share of infrastructure construction has begun to grow thanks to the inflow of funds under the European Recovery and Resilience Plan. This has made it possible to finalize previously frozen large projects: the longest (2 km) road tunnel in Bulgaria, Zheleznitsa, the third line of the Sofia metro, the Balkan Stream gas pipeline, and the IGB gas interconnector on the border with Greece.

This segment’s share in the total volume of construction work in 2020–2025 increased from 38% to 45%, creating additional demand for steel. Among the projects currently under implementation, the following can be highlighted:

- Modernization of the Elin Pelin–Kostenets railway line. This is the most expensive and complex railway project with dozens of bridges and tunnels for high-speed trains (up to 160 km/h).

- Construction of the A8 motorway, which will connect Sofia with Varna through the northern regions of the country.

- Construction of the Vidin-Botevgrad high-speed motorway. It will connect the New Europe Bridge over the Danube with the main road network.

- Construction of the Bulgarian section of the Europe motorway. Work is currently underway on the section from Sofia to Kalotina (border with Serbia).

Prospects for demand for long-term leasing

These facilities will remain drivers of demand for long-term leasing in the infrastructure sector in 2026. Its share will continue to grow thanks to new projects.

On January 1, 2025, Bulgaria and Romania became full members of the Schengen area by land. This abolished border controls on bridges across the Danube and sharply increased the need to expand capacity. Currently, there are only two bridges between Bulgaria and Romania on a 400 km stretch of the border.

In 2026, construction is expected to begin on the Ruse-Giurgiu-2 bridge, costing €2.5 billion. The funds are being allocated by the EU, and the project is awaiting approval by the European Commission. The Bulgarian government is also discussing the construction of the Nikopol-Turnu Măgurele bridge with officials in Brussels.

According to statements by the Bulgarian authorities, major repairs to the bridge in Ruse (Friendship Bridge) will continue in 2026.

In February, Bulgaria, Greece, and Romania intensified efforts to create the Aegean Sea–Black Sea transport corridor with the Thessaloniki–Alexandroupolis–Bucharest axis by signing an agreement on the development of a road and rail network.

The plan is to build the Silistra-Kelerashi bridge between Bulgaria and Romania, border bridges between Bulgaria and Greece, develop the Constanta-Burgas route, and restore passenger rail service on the Thessaloniki-Sofia route. It is expected that 85% of the costs will be financed by the European Commission.

The basis for further growth in residential construction in 2026–2027 will also be the record growth in the number of permits issued in 2025.

Outlook for demand for flat rolled products

According to analysts’ estimates, the share of mechanical engineering in Bulgaria’s GDP could reach 6.4–6.5% in 2026. The main driver here is the relocation of production from Southeast Asia. In particular, amid European anti-dumping duties on Chinese electric bicycles, Maxcom, in partnership with the Austrian Pierer Group, is completing the construction of a new plant in Bulgaria.

European manufacturers are also moving here due to low taxes and the cheapest labor in the EU. For example, British-Czech BTL Industries has built a large medical equipment manufacturing plant in Plovdiv. According to company representatives, it will become the main production site for customers from the European Union and the Middle East.

In 2025, French company Schneider Electric completed the expansion of its electrical equipment factory in Plovdiv. Previously, components for these devices were ordered from China. Now, production will be completely localized.

The launch of new enterprises and the stable operation of existing ones create the conditions for further growth in production in the machine-building industry and demand for finished steel.

Wind energy will also contribute. In 2026, Petroceltic will build the country’s first 5 MW offshore wind farm near Varna. Also this year, the government plans to hold tenders for the creation of floating wind farms with a capacity of up to 1 GW. They are expected to be commissioned by 2027.

To this end, an agreement was signed in Athens in January this year to create a cross-border offshore wind energy cluster. Thanks to the harmonization of regulations, investors will be able to build joint wind farms on the maritime border between Bulgaria and Romania, where the strongest winds blow.

Conclusions

The main challenge for Bulgarian steel consumption in 2026 will be price increases caused by the introduction of the CBAM. Previously, imports of Turkish long products reduced domestic prices. Now, the cost of Turkish and Bulgarian rebar on the local market has equalized.

Producers’ costs in Bulgaria have risen because the CBAM has made imports of steel billets, mainly from Ukraine, more expensive. This is not so critical for infrastructure projects financed by the EU budget, but it may have a negative impact on residential construction.

The situation with flat rolled products is similar. Due to the introduction of the CVA, the cost of Turkish and Egyptian sheet steel in Bulgaria has increased by approximately €60/t by February 2026. This makes Bulgarian engineering products less competitive in foreign markets. As a result, steel consumption growth in Bulgaria may slow down. It is likely that its volume will reach 1.39 million tons in 2026, exceeding the record pre-pandemic figure of 2018.

-

15 June 2026

16 June 2026

10 June 2026

27 May 2026