Posts Global Market scrap market 1303 05 February 2026

Temporary restrictions on supplies from Ukraine do not affect the supply of scrap metal to Polish steel mills

The scrap business in Poland has undergone significant changes over the past four years. Re-export operations of Ukrainian scrap metal to Turkey, made possible by the Free Trade Area between Ukraine and the EU, have turned the country into a transit hub on the way from Ukrainian scrap collection sites to the electric arc furnaces of Turkish steel plants.

Resolution No. 1795 of the Cabinet of Ministers of Ukraine dated December 31, 2025, which established a “zero” quota for steel scrap exports in 2026, temporarily (for one year) made this scheme impossible. The impact on Ukraine’s market is clear: local steelmakers, previously struggling with scrap shortages due to rising exports, will benefit from improved raw material supply. This is also expected to boost tax revenues and help retain more added value within the country. But how will the decision of official Kyiv affect the steel industry in Poland, given that some lobbyists have appealed to the European Commission for a diplomatic response? GMK Center looked into this.

Market profile: record exports in 2025

The Polish scrap market is oversupplied. In 2024–2025, collection amounted to 6.5–6.8 million tons, while local steel mills consumed 4.4–4.5 million tons. This means that even without additional supplies from Ukraine, supply in Poland significantly exceeds domestic demand. This fact refutes the argument that the cessation of Ukrainian imports is allegedly harmful to the Polish steel industry.

The largest local players – ArcelorMittal Poland, CMC Poland, and Złomrex (Cognor Holding) – have an extensive network of scrap collection points throughout Poland. CMC Poland operates an electric steel mill in Zawiercie with an annual capacity of 1.7 million tons of steel. ArcelorMittal Poland also includes the scrap collection company Złomex.

Thus, Polish steel companies can independently supply their steel-making capacities with scrap resources through domestic collection, without relying on imports. At the same time, they continue to gradually absorb small independent suppliers, strengthening their market position and expanding their resource base.

So why do Polish traders additionally purchase imported resources, despite the surplus of local scrap supplies? The reason lies in the price differential between Turkey, where current quotations for HMS 1/2 (80:20) are at $375–380/t CFR Iskenderun/Marmara, and the purchase price of Polish steel mills at $335–360/t DDP. Thanks to this difference, steel scrap exports from Poland have grown by 54% over the past six years. In 2025, a record was set at 2.95 million tons.

Thus, local scrap is shipped to Turkish consumers, while Polish steel mills receive resources from neighboring Germany and the Czech Republic. However, we would like to emphasize once again that imports account for an insignificant part of scrap consumption. Domestic collection mainly supplies it.

Scrap operations from Ukraine were even more profitable. Before the introduction of the “zero” export quota, Ukrainian traders asked for $310–$325 DAP at the Polish border. For direct shipments from Ukraine to Turkey, they had to pay a duty of €180/t. Therefore, scrap was shipped to Polish ports, where it was legally registered as a local resource.

A distinct group of Polish market players known as “port suppliers” has emerged. These companies don’t have their own scrap collection networks but operate transshipment terminals in ports such as Gdańsk, Szczecin, and Gdynia.

In addition, affiliated structures of Ukrainian scrap traders are registered in Poland. They are also used for the transit of scrap metal from Ukraine to Turkey. For example, Keramet LLC has a subsidiary, Keramet Polska Sp. z o.o., registered in Częstochowa.

Impact of government regulation: from transit hub to direct export

The suspension of supplies from Ukraine does not affect the supply of scrap metal to Polish steel mills. Ukrainian imports accounted for no more than 5% of the total Polish market. First, this is too small a share to change the current balance. Secondly, virtually all the resources received were subsequently sent to Turkey.

Thirdly, it is important to note the reduction in scrap consumption in Poland due to the decline in steel production. While in pre-crisis 2018 it amounted to 10.8 million tons, by the end of 2025 it will be only 7.2 million tons. It is an undeniable fact that Polish steel mills need less and less scrap.

At the same time, thanks to Poland’s membership in the European Union, local steelmakers can always purchase the missing volumes in neighboring Germany and the Czech Republic without additional duties in case of force majeure. Thanks to their developed machine-building industry, which is the main driver of scrap generation, they can not only meet the demand of their own steel companies, but also export surpluses to foreign buyers.

This is confirmed by estimates from the WVStahl and Ocelarska unie associations, according to which scrap exports from Germany and the Czech Republic in 2025 amounted to 7.9 million tons and 2.1 million tons, respectively. There is no supply shortage.

In general, the EU has confidently maintained its status as the world’s largest exporter of scrap metal for many years. In January-October 2025 alone, supplies outside the European Union amounted to 13.36 million tons.

The only ones who suffered losses were “port processors.” But even they will not leave the market. As long as steel scrap prices in Turkey exceed $370/ton CFR, they will still have opportunities to export surplus Polish resources.

The only change is that Poland will cease to be a transit hub for scrap metal, returning to its role as a direct supplier. At the same time, scrap export volumes will no longer grow as rapidly as in 2022–2025, when the “Ukrainian scheme” was in effect.

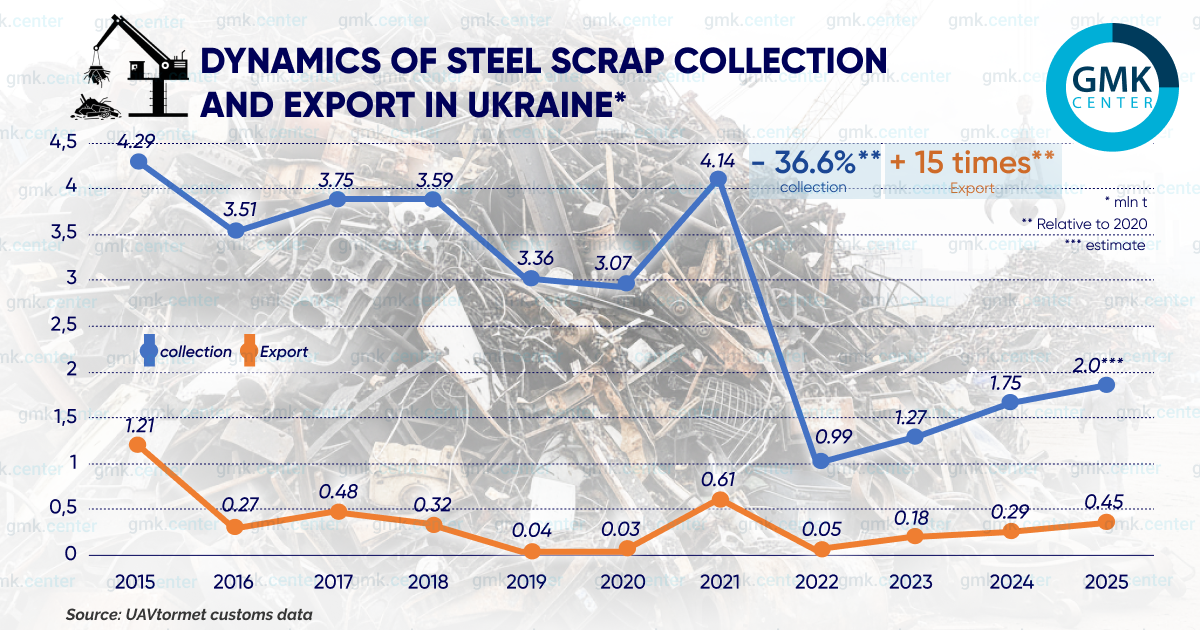

It is important to emphasize the reasons why the official Kyiv temporarily suspended scrap exports. The volume of scrap metal collection in Ukraine in 2021–2025 fell by more than 2.5 times to 2 million tons. At the same time, shipments abroad grew at a record pace. By the end of 2025, they reached a four-year high of about 0.45 million tons.

Domestic scrap consumption grew by 10–12% in 2025, making the battle for every ton of raw materials critical. The European Union countries do not have this problem. So where is the mythical blow to Polish steelmakers, as claimed by representatives of the Polish Chamber of Metallurgy and Trade and the Polish Union of Steel Distributors?

It is obvious that these emotional accusations against the official Kyiv are not supported by facts. The facts prove the opposite. The same is true of Poland’s ban on imports of agricultural products from Ukraine. Polish speakers claimed that this was causing losses to local farmers. However, monitoring by the European Commission did not reveal such losses. Therefore, we can assume that such statements by the Poles are politically motivated and have nothing to do with market reality, as well as the interests of traders who are increasing exports of scrap metal from Poland to Turkey and other non-European countries, while the EU itself has not restricted exports of ferrous scrap metal.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

22 July 2026

17 July 2026

14 July 2026