Posts Infrastructure construction 3834 14 April 2025

Warehouses, factories, grain elevators, and hotels were actively built in the west and center of the country

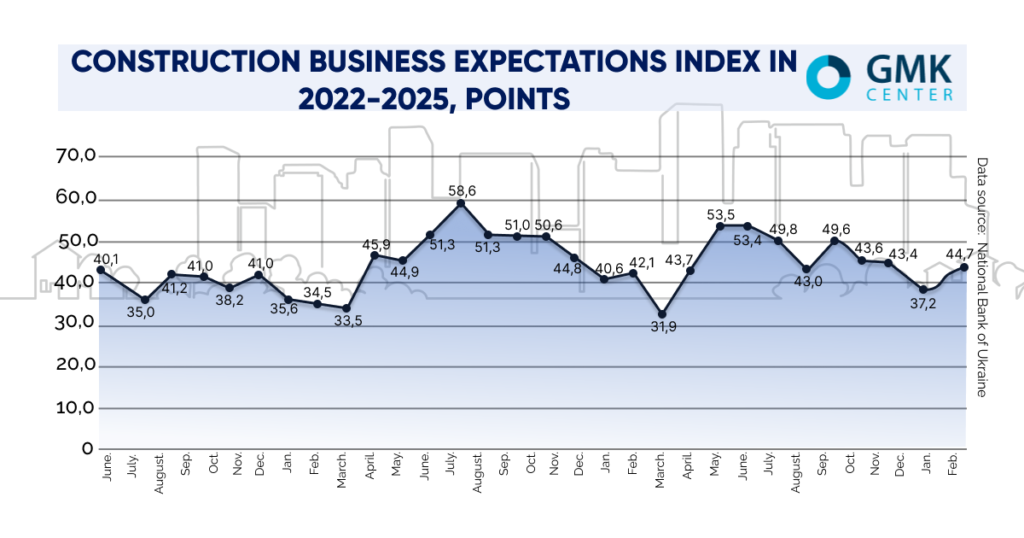

In 2023-2024, the Ukrainian construction market showed positive dynamics due to the intensification of economic activity in the central and western regions, as well as due to the restoration of war-damaged infrastructure and programs to protect energy facilities. At the same time, the volume of the market itself is still almost half of its pre-war level in 2021.

Construction market picture

The volume of completed construction works in Ukraine last year increased by 15.5% y/y – to UAH 204.7 bln. There is a slowdown in growth dynamics compared to 2023 (25% y/y) partly due to the effect of a low base of comparison in 2022, as in the first year of full-scale war the volume of construction work collapsed by 65% in annual terms.

By individual segment, the increase in construction work in 2024 was as follows:

- residential construction – by 7.6% y/y, up to UAH 26.6 bln;

- non-residential construction – growth by 26.2% y/y, up to UAH 57.7 bln;

- engineering constructions – growth by 12.5% y/y, up to UAH 120.4 bln.

According to GMK Center estimates, the volume of the construction market in dollar equivalent in 2024 increased by 14.6% y/y – to $5.1 bln. However, this is 45.2% lower than in pre-war 2021 ($9.3 bln). Individual segments of the construction market showed the same dynamics in dollars as according to State Statistics Service data.

Among the main trends and challenges of the construction industry last year, which, however, are also relevant in 2025, are the following:

- increase in production costs due to rising prices for energy, building materials, etc. amounted to 25-40% in different segments of the construction market;

- shortage of labor force – both low-skilled and specialists and engineers;

- power supply disruptions due to missile strikes on the energy infrastructure during the spring and summer of 2023;

- delayed payment for government contracts, which requires the contractor to have significant working capital;

- slowdown in the dynamics of infrastructure construction compared to 2023 (+33%) due to problems with state funding for the protection of power facilities.

Lack or shortage of financing is one of the key problems of the entire construction industry, as the market can “absorb” much larger volumes, especially in terms of infrastructure and non-residential construction.

“Since the ‘big build’ the number of companies capable of carrying out such work has increased significantly. The number and volumes of existing projects do not allow loading the number of construction companies that now operate in this market. Therefore, the competition for each contract is very tough,” says Dmytro Tonkoshkur, technical director of MetTransService.

Residential real estate market

According to the results of 2024, the total area of commissioned housing in Ukraine increased by 32% – up to 9.8 million square meters. Regional leaders are predicted to be Kyiv – 1.41 million sq. m. (14.5% of the total size), Kyiv and Lviv regions – 1.95 million sq. m. (19.9%) and 1.06 million sq. m. (10.9%) respectively.

According to Oleg Prikhodko, general director of Greenol development company, the main reasons for such growth were the following factors:

- The action of state support programs, such as “e-Osela”, which stimulated demand for housing, particularly in the primary market segment. In 2024, the volume of loans issued under the program amounted to UAH 14.6 billion (+66% YoY), although in the second half of the year lending slowed down due to changes in the terms of lending and lack of funds. The plan for “єOsela” for 2025 envisages UAH 18 bln.

- Developers’ activity has been concentrated in regions remote from the fighting – Kyiv, Lviv, Zakarpattya and Ivano-Frankivsk regions. These regions have become magnets for internally displaced persons, which has increased demand for housing and stimulated the completion of projects started before the war.

- Gradual adjustment of logistics and stabilization of the supply of building materials, despite high energy and logistics costs, which increased many times compared to the pre-war period.

Mortgage is actively developing – by the end of 2024 the volume of mortgages exceeded the pre-war level by 30%, but its volumes are absolutely insufficient in the current conditions.

“Net hryvnia loans of the population for 2024 grew by almost 40%. The share of mortgages in the portfolio of loans to the population at the end of 2024 increased to 13.5%, but remains quite small”, noted in the NBU.

Non-residential construction

Non-residential construction showed the highest dynamics among all market segments. The area of non-residential premises accepted last year increased by 15% to 2.7 million square meters. m. Last year the construction of logistics, retail and industrial real estate, as well as hotels was actively developing. According to the results of 2024, commissioning of industrial buildings and warehouses increased by 16% compared to 2023 – up to 987 thousand sq. m. This is only 12% lower than in pre-war 2021.

The demand for non-residential construction is driven by developers of warehouse and hotel real estate, retailers, food industry, machine building and agricultural processing companies, manufacturers of building materials, etc. The main drivers of demand for non-residential construction are developers of warehouse and hotel real estate, retailers, food and beverage companies, and manufacturers of construction materials.

One of the main reasons for the significant growth of the industrial real estate market is the relocation of enterprises to the central and western regions of Ukraine. According to Opendatabot service, over 11 thousand companies changed their registration in 2024, which confirms the ongoing process of business migration, albeit with a slightly lower dynamics (-18% y/y).

“Western regions such as Volyn, Ivano-Frankivsk, Lviv, Ternopil and others continue to attract both local and international companies. For example, several large international companies, including Nestlé, Peikko Group Corporation, Philip Morris, Saint-Gobain and others have already launched their production facilities in new locations or are at different stages of the process of transferring their production facilities”, – says Yaroslav Gorbushko, Director of Capital Markets Department at CBRE Ukraine.

Also, as CBRE Ukraine notes, in recent months there has been increased activity among manufacturers from Dnipropetrovsk region, which is due to security factors, namely the approaching front line. It is not excluded that in case of further aggravation of the situation, we can expect a stronger tendency to relocation of industrial enterprises from this region to safer areas.

Engineering construction

This largest segment of the construction market consists of two sub-segments:

1. Construction of structures for various purposes.

The largest engineering projects in 2024 with a total value of at least UAH 13.4 billion are new main water pipelines in Dnepropetrovsk region, the need for which arose after the destruction of the Kakhovska HPP dam:

- Marganets – Nikopol – Pokrov;

- Ingulets River – Southern Reservoir;

- Khortytsya (DVS2) – Tomakovka – Marganets.

2. Restoration of social, transportation and energy infrastructure facilities destroyed due to Russian military aggression.

In 2024, about 20% of the construction market was occupied by the restoration and protection of critical infrastructure facilities. According to Oleksandr Dunaysky, director of Metal Invest, the most active restoration is taking place in Kharkiv, Chernihiv, Dnipropetrovsk and Zhytomyr regions.

Among the problems of the recovery processes are the following:

- Lack of funds, which leads to delayed payments to contractors. According to Dmytro Tonkoshkur, funding for the construction of defense facilities and bridge rehabilitation is very limited.

- Restoration of residential and social facilities is done in a point-by-point rather than comprehensive manner.

- Underfunding of certain areas of work. In particular, the volume of work on repair of highways has significantly decreased.

Construction prospects

The nature and dynamics of development of the construction industry in the current year depends on the factor of security and economic stability. If the intensity of hostilities does not increase and financing of mortgage programs and infrastructure rehabilitation continues, the market may maintain positive dynamics. However, if the situation on the front or in the economy worsens, the pace of construction may slow down.

In addition to war risks, rising material and energy prices, labor shortages, limited access to financing to increase production capacity, etc. remain relevant. It is expected that in 2025, construction costs could rise by another 15-25%.

At the same time, construction market operators expect Ukraine to experience a surge in demand and industry development in the process of post-war recovery.

“One of the key investment trends is the active entry of building materials manufacturers into the market, driven by the expected increase in demand as part of the country’s upcoming recovery. In particular, the Irish company Kingspan (sandwich panel manufacturer), has already announced investments in local production,” says Natalia Sokirko, director of warehouse and logistics real estate department at CBRE Ukraine.

According to Andriy Ozeychuk, director of engineering and construction company Rauta, most investors are already actively calculating the cost of construction and waiting for the end of hostilities to start new projects. With positive growth dynamics, the Ukrainian construction market will be able to reach the level of 2021 in 4-5 years.