News Global Market iron ore prices 150 29 June 2026

The downward trend in the market has continued since mid-May, leading to an 8% fall in prices

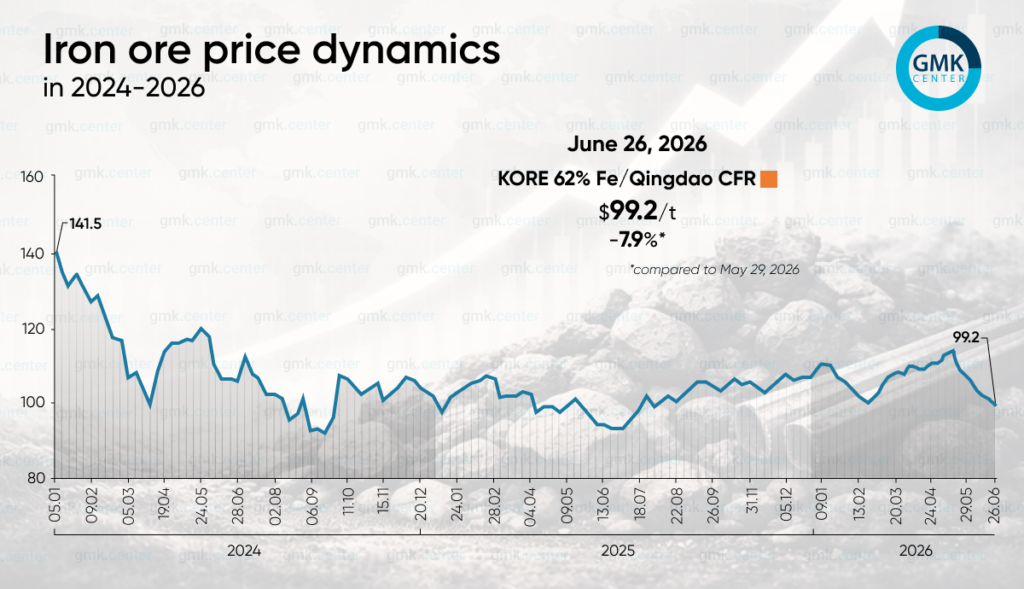

Iron ore prices (KORE 62% Fe/Qingdao) had fallen to $99.2/t as of 26 June 2026 – their lowest level since August 2025. This is 7.9% lower than on 29 May, whilst the average price in June stood at $101.7/t following a peak of $111.2/t in May (-8.5% month-on-month).

In June, the iron ore market came under pressure from several negative factors simultaneously. The main driver of the decline was the expectation of weaker demand from Chinese steelmakers against the backdrop of a seasonal slowdown in construction, deteriorating steel production margins and a cautious procurement policy on the part of steelworks. Most mills operated under a low-stock strategy, purchasing only small batches and showing interest mainly during sharp price dips.

Additional pressure came from rising supply. Market participants noted more active shipments from Australia and Brazil, as well as a gradual build-up of stocks in Chinese ports. This heightened concerns about an imbalance between supply and actual demand, particularly given signs of a decline in pig iron production following peak levels.

Short-term support for prices came from isolated supply-side risks. In particular, the market reacted to a labour dispute at BHP’s facilities near Port Hedland, and towards the end of the month to unconfirmed reports of a possible reduction in supplies from Simandou. However, these factors were largely speculative in nature and failed to alter the overall downward trend.

Temporary support was also provided by higher freight and logistics costs linked to geopolitical tensions and more expensive fuel. It was this factor that prompted Fitch to raise its short-term forecasts for iron ore prices. At the same time, in the second half of the month, the easing of tensions in the Middle East and falling energy prices reduced the support provided by transport costs.

A separate trend was the growing interest among Chinese steel mills in lower-grade ore. Against a backdrop of pressure on margins, mills sought to optimise raw material costs, which limited premiums on high-quality products.

In the short term, the market will remain vulnerable to news regarding Chinese demand, port stocks and political signals following the Politburo meeting at the end of July. Without a noticeable improvement in demand or genuine supply disruptions, prices may remain around $98–102/t, with the risk of a further decline.

-

15 June 2026

29 June 2026

29 June 2026

29 June 2026