News Global Market hot-rolled prices 3967 23 September 2024

Expectations for the revival of the market after the summer holidays did not come true

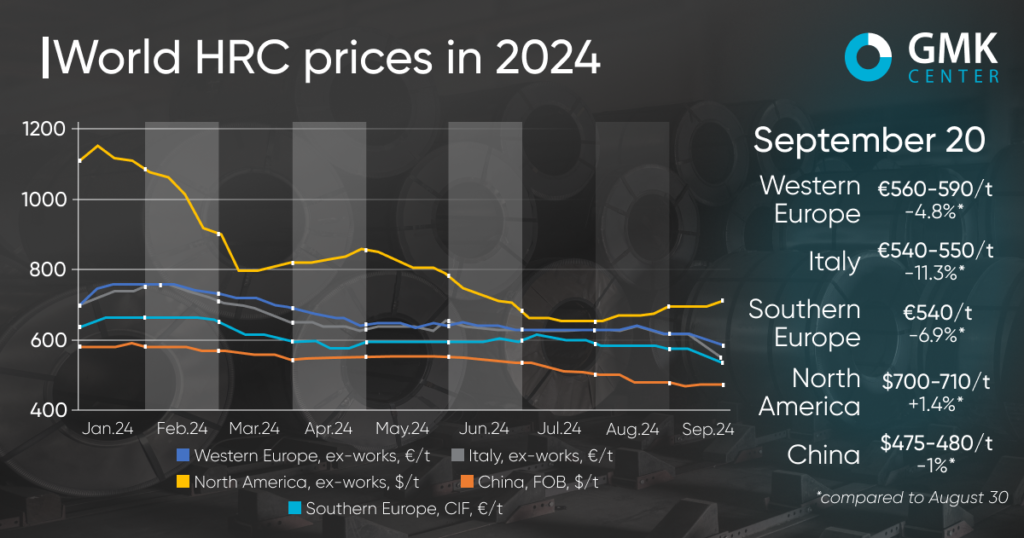

Global hot-rolled coil prices continued to decline in August and early September, driven by weak demand, economic uncertainty and high inventory pressure. Supply in Europe and China reached their lowest levels since 2020. At the same time, South America saw some recovery in prices, which may indicate that the bottom has been reached after prices almost halved since the beginning of the year.

Hot-rolled coil prices on the European market have seen a significant decline since the beginning of September. In Western Europe, and in Italy in particular, product quotations decreased by 11.3% (August 30 – September 20, 2024) to €550/tonne Ex-Works, respectively. At the same time, in Southern Europe, the decline was 6.9%, to €540/t CIF. Currently, the price level for hot-rolled coils on the European market is the lowest since the beginning of the year.

Last month, some steel mills tried to raise HRC prices by €20-30/t, but consumers did not accept these intentions. As demand is still weak and inventories exceed consumption, prices are falling.

Market participants’ expectations of a possible pickup in consumption after the summer holidays did not materialize. In particular, this is due to the poor economic situation in Germany, the weak state of the automotive and household appliances sectors in the EU. Local consumers are also not interested in imported products from Asia, whose supply fell significantly in early September to €560-570/t CFR.

The short-term expectations of market participants vary considerably. Some predict an improvement in activity in the second half of September, while others expect further price declines due to pressure from imports and the overall weakness of the global market.

“The European Commission has launched anti-dumping investigations into imports of hot-rolled coils from 4 countries: Japan, India, Vietnam and Egypt. If provisional duties are imposed as part of these investigations, they will provide some support to prices for hot-rolled coils. However, given the fall in commodity prices and the weakness of the EU economy, the positive effect is unlikely to be long-lasting,” said Andriy Glushchenko, GMK Center analyst.

Hot-rolled coil prices in North America showed a slight increase of 1.4% – to $710 per tonne between August 30 and September 20 this year. At the same time, prices rose by 7.7% in August, but they are still significantly lower than at the beginning of the year.

HRC prices in the region saw a slight rebound amid increased supply from key US steelmakers. In particular, Cleveland-Cliffs announced an increase in the September spot price for hot rolled coils by $20/t from $730/t – to $750/t, while Nucor raised its weekly spot price for coils by $10/t on September 11 compared to the previous week to $720 per short ton.

Sources in the flat steel market indicate that consumers are accepting a moderate price increase. The transparency of spot prices provided by Cleveland-Cliffs and Nucor is helping to increase consumer confidence in buying. At the same time, there has been a sharp increase in demand from the construction industry and service centers.

In China, hot-rolled coil prices have fallen by 1% – to $480 per tonne since the beginning of September. At present, Chinese prices are also at their lowest level since the beginning of the year. The market decline is the result of weak sentiment, rising inventories and production. Exports are also falling, but at a slower pace, as demand abroad is still better than at home.

Typhoons in eastern China, where one of the largest economic regions is located, have slowed economic activity and reduced steel consumption. Market expectations for the next few weeks remain negative. Prices may fall again after the National Day in early October, but the main problem is the decline in activity in export markets.

-

Opinions Industry steel consumption

13 July 2026

21 July 2026

20 July 2026

20 July 2026