News Global Market EU 283 11 June 2026

Competition for LNG could intensify this summer, depending on weather conditions in Asia

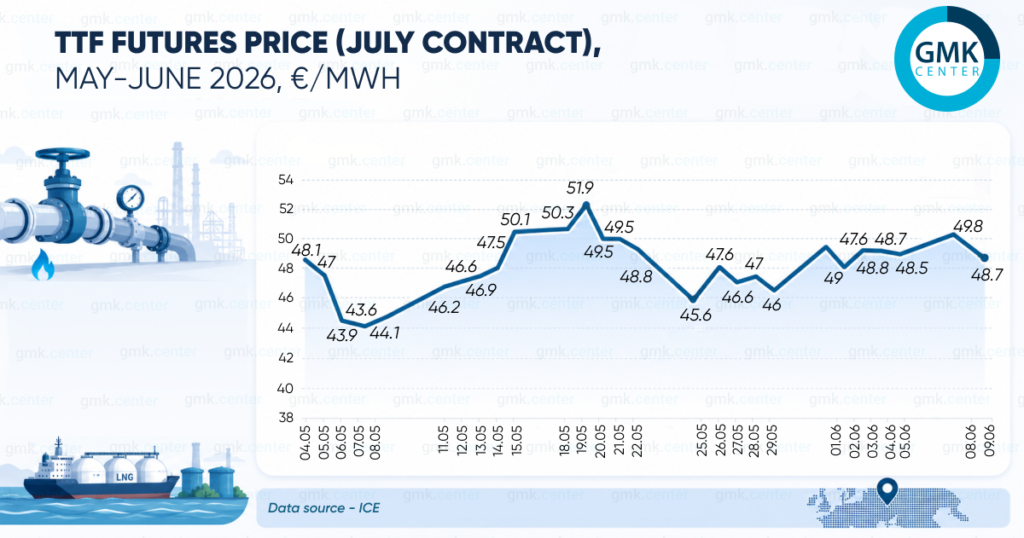

In early June 2026, one-month TTF futures remained below €50/MWh, generally fluctuating between €48 and €49/MWh.

In the first ten days of the month, European natural gas prices rose compared to the end of May amid uncertainty over the prospects of conflict in the Middle East and pressure to fill storage facilities ahead of the winter season.

According to ICE, the highest price for TTF one-month futures was recorded on 10 June at €49.9/MWh.

According to data from the AGSI platform, as of 9 June 2026, European gas storage facilities were 42.79% full (on the same date in 2025, the figure stood at 51.4%).

Market analysts warn that LNG prices and competition for it could rise this summer if supply disruptions are compounded by a heatwave in Asia. In particular, John Roper, Uniper’s Executive Director for the Middle East, recently warned of this. According to him, the current disruptions have hit Asian countries, with the exception of China, harder than Europe, and the consequences will be felt until at least 2030. However, new LNG projects, which are due to come online in 2027–2028, will ensure a more balanced gas market in the medium term.

Bloomberg columnist Javier Blas has suggested that Europe is likely to have enough gas to avoid a sharp rise in gas and electricity prices, despite the slow seasonal replenishment of stocks.

He notes that European officials believe regional gas stocks could still be replenished to around 80% by the start of next winter. However, according to the expert’s estimates, Europe will reach only 70% by the end of October.

Meanwhile, Greg Molnar, a gas analyst at IEA, notes that the decline in supplies from the Middle East in May was offset by other sources. In May this year, LNG supplies from the Gulf states fell by almost 9 billion cubic metres, equivalent to approximately 45% of EU demand for that month. At the same time, supplies from outside the Persian Gulf during this period rose by 20% year-on-year, adding nearly 8 billion cubic metres to the market and offsetting around 90% of the losses caused by the situation in the Strait of Hormuz.

This increase, the expert emphasises, was largely supported by new liquefied natural gas production capacity in the US and Canada, as well as improved availability of feed gas from some traditional producers. Therefore, price dynamics may change should the Strait of Hormuz reopen.

It should be noted that European gas prices in the first half of May stood at €44–49/MWh. As is the case now, the market was pressured from the conflict in the Middle East and the need to replenish stocks.