Infographics quotas 23 17 June 2026

Stricter EU tariff-rate quotas would harm Ukraine’s wartime economy without solving Europe’s real steel-market challenges

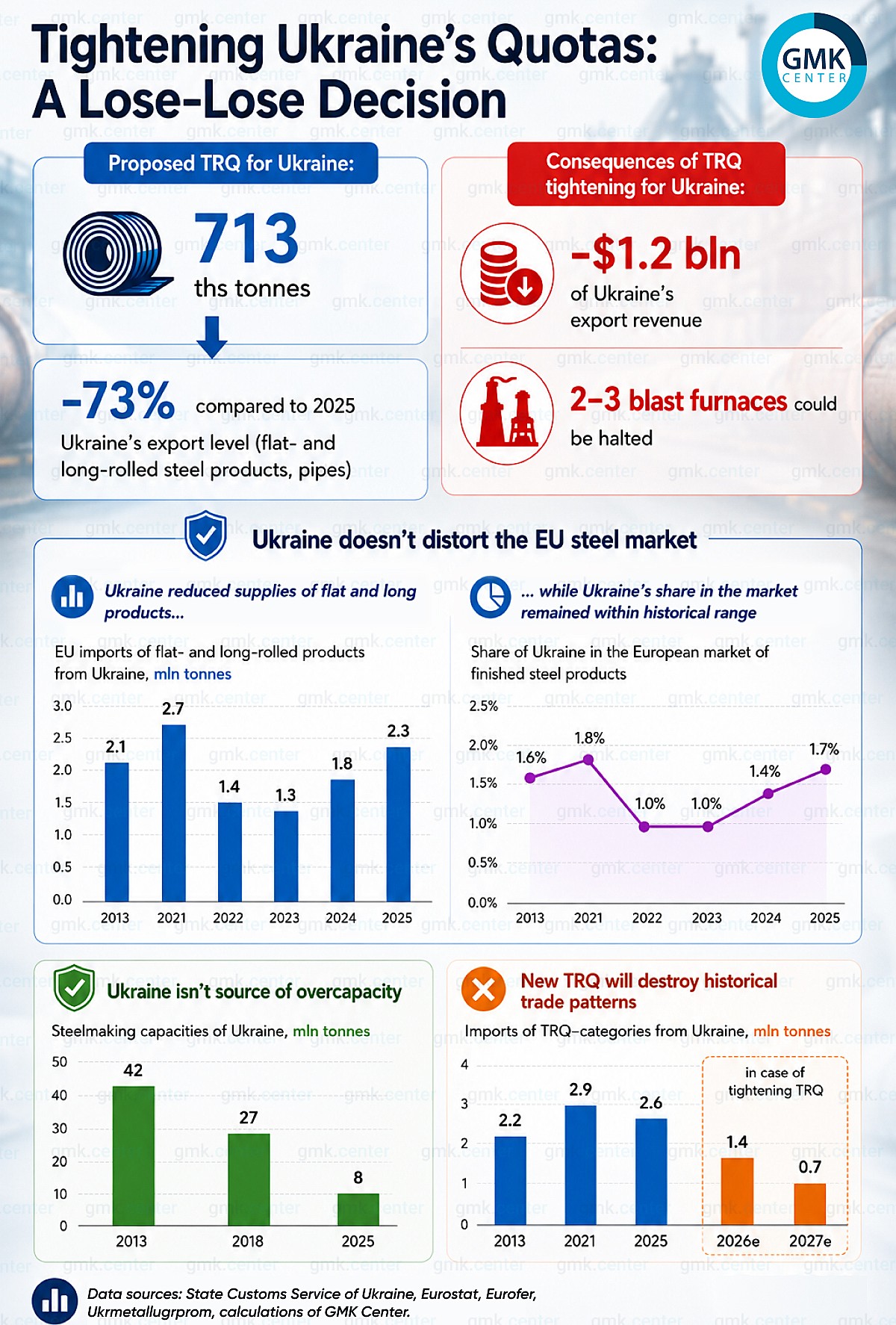

According to mass-media, the EU is going to set Ukraine’s TRQ at 713 ths tonnes for flat- and long-rolled steel products and pipes. That would represent a 73% reduction compared with Ukraine’s 2025 export level. The expected consequences for Ukraine are severe: an estimated $1.2 bln loss in export revenue and the possible shutdown of two to three blast furnaces. Crucially, the expected shock would be policy-driven rather than caused by any market fundamentals.

Tightening Ukraine’s TRQ doesn’t look substantiated since Ukraine isn’t a source of pressure on the EU steel market. EU imports of flat- and long-rolled products from Ukraine reached about 2.3 mln tonnes in 2025, below the 2021 level of about 2.7 mln tonnes. Ukraine’s share of the European finished steel market remained within its historical range, reaching about 1.7% in 2025. In other words, Ukraine’s presence in the market is measurable and limited.

In flat-rolled steel imports to the EU in 2025, Ukraine accounted for about 1.6 mln tonnes, or 6.8%, while Türkiye, South Korea, India, Indonesia, Taiwan, Vietnam, and China held larger positions. In long-rolled steel imports, Ukraine represented about 766 ths tonnes, or 9.1%, behind Türkiye and China and alongside several other suppliers. Ukraine is one import source among many. Imports from Ukraine is not large enough to drive price or volume disruption across the EU.

Ukraine is not a source of global or regional overcapacity. Ukrainian steelmaking capacity has fallen dramatically, from 42 mln tonnes in 2013 to only 8 mln tonnes in 2025. This collapse reflects the destruction caused by war. Restricting Ukrainian access further would therefore penalize a diminished and strategically important producer without addressing the structural causes of oversupply in the European steel market.

Moreover, new TRQ would break historical trade patterns. Ukrainian imports in TRQ-covered categories were 2.2 mln tonnes in 2013 and in range of 2.6-2.9 mln tonnnes in 2022-2025. Under tightened quotas, they would fall to an estimated 1.40 mln tonnes in 2026 and only 713 ths tonnes in 2027 that will disrupt European supply chains.

The EU market’s real challenges which should be addressed are rising TRQ-exempt imports from Asia and stagnating steel demand. Hot-rolled coil imports from Indonesia climbed almost 18 times (from 91 ths tonnes in 2021 to 1.6 mln tonnes in 2025). In Q4 2025, hot-rolled coil shipments from Indonesia and Malaysia exceeded 1 mln tonnes, crushing prices and denying EU mills any recovery in margins. Low-cost imports from Asia continue to exert a negative effect on EU prices this year.

Apparent EU steel consumption fell from 150.4 mln tonnes in 2021 to 128.4 mln tonnes in 2025. In long term restricting imports will not increase steel demand in the EU. On the contrary, higher steel prices caused by trade restrictions will put additional pressure on downstream industries that are already struggling with competitiveness.

-

15 June 2026

04 June 2026

03 June 2026

01 June 2026