News Global Market iron ore prices 164 03 June 2026

Commodity prices began to decline following an upward trend that had been in place since early March

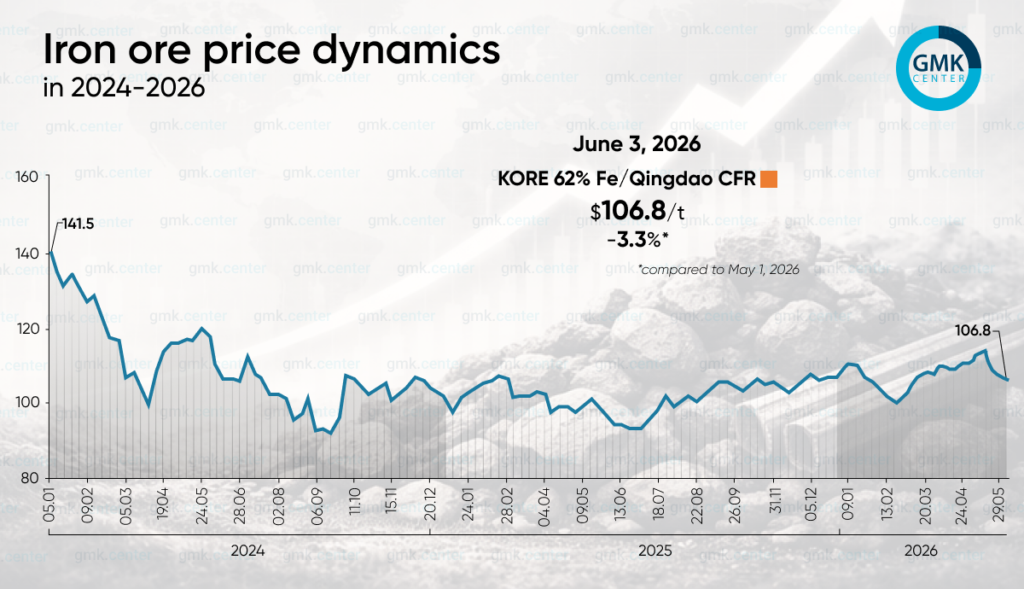

Iron ore prices (KORE 62% Fe/Qingdao) began to decline in late May–early June 2026 following a prolonged recovery that had been underway since early March. As of June 3, iron ore prices stood at $106.8/t CFR, down 3.3% from May 1, while the average price for May was $111.2/t compared to $109.4/t in April, indicating that prices remained high at the beginning of the month but fell sharply in the final week.

In early May, the market was still riding the wave of growth momentum that had built up in March and April. Following the holidays in China, steel mills partially resumed their purchasing, while improved margins for steelmakers and rising steel prices supported demand. Expectations of a pickup in consumption in China and on foreign markets served as an additional factor. Against this backdrop, KORE 62% Fe rose above $114–115/t CFR in the first half of the month.

At the same time, by mid-May it became apparent that the market was following the pattern of strong expectations versus weak reality. Infrastructure activity in China showed signs of recovery, but actual demand remained sluggish. Purchases by smelters weakened after brief waves of restocking, and spot trading lost momentum. Pressure was intensified by rising global ore shipments, high inventories in Chinese ports, and expectations of a seasonal peak in miners’ shipments.

After May 18, the decline accelerated. The market reacted to fading macroeconomic optimism following a lack of breakthroughs in negotiations between China and the U.S., as well as to fears that pig iron production had already neared its peak. Sentiment was further dampened by environmental inspections in Chinese provinces, which heightened the risks of restrictions on steel production and demand for iron ore. The decline in billet prices in Tangshan served as another signal of market weakness.

High freight rates and temporary interest in lump ore provided some support to prices, as some mills optimized their blast furnace charge to reduce coke consumption. However, these factors merely limited the depth of the correction without shifting the balance in favor of sellers.

In the short term, ore is likely to remain under pressure due to high port inventories, seasonal weakening of steel demand, and active shipments at the end of the quarter. A sharp decline could be limited by high freight rates, coking coal costs, and potential disruptions or trade restrictions affecting certain suppliers. The base case is a range of $105–110/t CFR, with the risk of further declines if demand in China does not recover.

-

Opinions Industry macroeconomics

28 May 2026

03 June 2026

03 June 2026

02 June 2026