Posts electricity prices 6602 03 April 2025

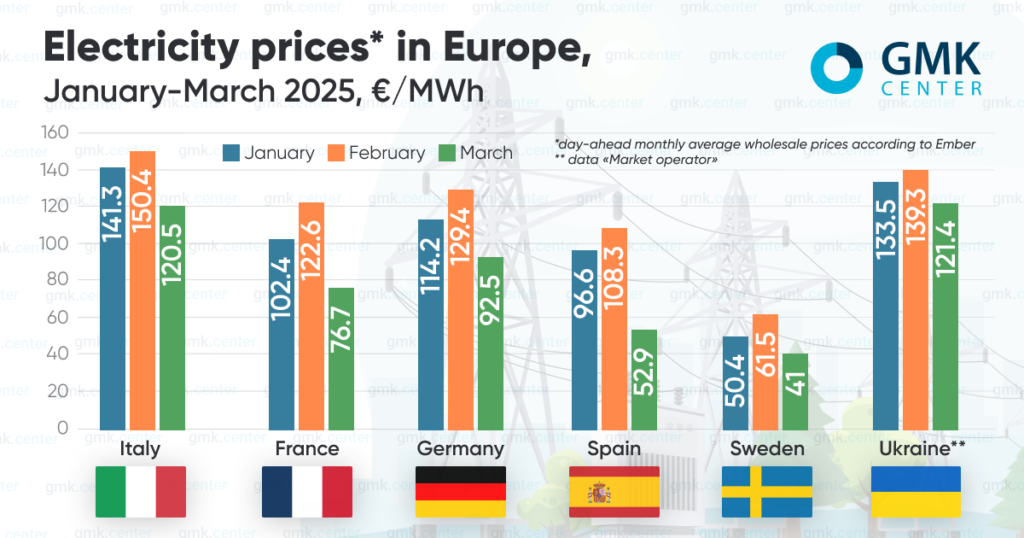

Last month, the weighted average price for DAM in Ukraine amounted to €121.4/MWh

In March 2025, average monthly wholesale day-ahead prices in Europe fell significantly in most markets.

According to Ember, they were as follows:

- Italy – €120.49/MWh (-19.8 m/m);

- France – €76.73/MWh (-37.4%);

- Germany – €92.54/MWh (-28.5%);

- Spain – €52.87/MWh (-51.2%);

- Sweden – €41.03/MWh (-33%).

The decline in electricity market prices in Europe last month was driven by falling demand, increased renewable energy generation, lower gas prices and CO2 emissions. The only exception was the second week of March due to lower temperatures in the region. At the end of the month, a number of markets registered negative hourly prices and the lowest daily electricity prices since mid-2024.

In general, according to AleaSoft, in January-March 2025, the average quarterly electricity price in most major European markets exceeded €85/MWh amid rising demand, the cost of TTF gas futures in the first month of the year and an increase in the quarterly carbon price.

European decisions

On March 19, the European Commission released its Steel and Metals Action Plan, which aims to strengthen the competitiveness of the steel sector and protect its future. The document, among other things, provides for affordable and secure energy supply.

According to the EC, the cost of energy remains a key factor in the industry’s competitiveness, as it accounts for a larger share of production costs than in other sectors. Before the energy crisis, according to the institution, this share was about 17% for the steel sector and 40% for aluminum, and in 2022 it increased to 80%. It is also noted that electricity prices in the EU are 2-3 times higher than in the US, and gas is five times more expensive.

The plan proposed by the EC encourages the use of power purchase agreements (PPAs). The institution calls on member states to use the flexibility of the energy tax and reduced network tariffs to mitigate price volatility. Thus, the European Commission has essentially given the green light to any energy subsidies that do not contradict European energy legislation and state aid rules.

The document also provides for faster access to the grid for energy-intensive industries and supports the increased use of renewable energy sources and low-carbon hydrogen in these sectors.

However, industry associations insist on more detail. For example, EUROFER noted that further work on reducing energy costs is crucial, as high energy prices affect not only steel and metal production but also entire European industrial value chains. The German Steel Industry Association (WVStahl) pointed out that the EC plan still lacks a specific concept of a competitive price for industrial electricity.

Italy’s Assofermet, which represents distributors of scrap, raw materials and steel products, believes that the measures to reduce energy costs in the plan are of little importance and require further concrete steps. A similar opinion was expressed by Federacciai, the country’s steel producers’ association. They also pointed to a possible inequality between European countries in this regard.

The situation in Ukraine

In Ukraine, the weighted average price for the purchase and sale of electricity on the DAM in March 2025, according to Market Operator, fell by 9.4% month-on-month to UAH 5,473.83/MWh (€121.4/MWh at the average monthly exchange rate of the hryvnia to the euro). Demand for the DAM in the period under review decreased by 18.44% compared to February, while supply decreased by 10.61%.

In March, according to ExPro Electricity monitoring, Ukraine increased electricity imports by 11% m/m to 272 MWh. The largest volumes came from Hungary (42%). Slovakia came in second (19%), and Poland was third (18%).

At the same time, electricity imports to the country last month decreased by 40% year-on-year.

In March, Ukrenergo applied power restrictions for industry and business only three times – at the beginning and in the middle of the month, justifying it by the consequences of Russian attacks on energy facilities.

Fullness of gas storage facilities

According to the AGSI platform, European gas storage facilities were 33.6% full as of March 30, 2025 (compared to 58.5% on the same date in 2024).

The winter of 2024/2025 was the coldest for Europe in the last four heating periods, so this winter, reserves were depleted faster than usual. Earlier, the region had lost most of its pipeline gas supplies from Russia, and in early 2025, gas transit through Ukraine was suspended.

At the end of March, the price of futures on the TTF hub in the Netherlands was €40.7/MWh, while at the beginning of the month (March 3) it exceeded €45/MWh, but has since fallen. Contracts for the summer months are currently trading at over €42/MWh.

In April, the EU begins the season of filling gas storage facilities, but cool spring weather may force an extension of the withdrawal. At the same time, Bloomberg writes that the tightening of the market has led to the fact that summer gas prices are now consistently higher than prices for the following winter, which eliminates financial incentives for storage deals.

In this situation, the role of governments and their role in the process will be important. At the same time, traders note that April will demonstrate whether market participants are ready to start pumping gas despite the price situation, or whether they will take a wait-and-see attitude.

The EU is also currently discussing new conditions for filling gas storage facilities – the European Commission’s rules provide for a target of 90% by November 1. It is about the possibility of deviating from it by 5% in case of unfavorable market conditions. The proposed change complements other options, such as not applying a fixed deadline.

The negotiating proposal was prepared by Poland, which currently holds the presidency of the bloc. Countries such as Germany, France, and the Netherlands are concerned that compliance with the rules will lead to price increases or manipulation.

According to the latest estimates, Ukraine needs to import 4.5-5 billion cubic meters of gas to get through the next heating season comfortably.

In particular, Dmytro Abramovych, a member of the Board and Commercial Director of Naftogaz Group, announced at a meeting of the parliamentary committee that the figure of 4.5-4.6 billion cubic meters by November 1 was needed. According to him, in February-March of this year, the company imported almost 800 million cubic meters, but these were technological imports. The commercial director also said that during the last heating season, Ukraine lost 700 million cubic meters of its own production as a result of Russian shelling.

On March 26, the EBRD approved a new loan for Naftogaz of Ukraine for the purchase of natural gas for the next two heating seasons worth up to €270 million, the company said. Additionally, about €140 million in grants from the Norwegian government will be channelled through the EBRD for these purposes.

-

Opinions Industry rolled steel

25 June 2025

25 June 2025

18 June 2025

16 June 2025