News Global Market scrap prices 5966 20 September 2024

Scrap production in the EU is decreasing in parallel with the decrease in steel production volumes

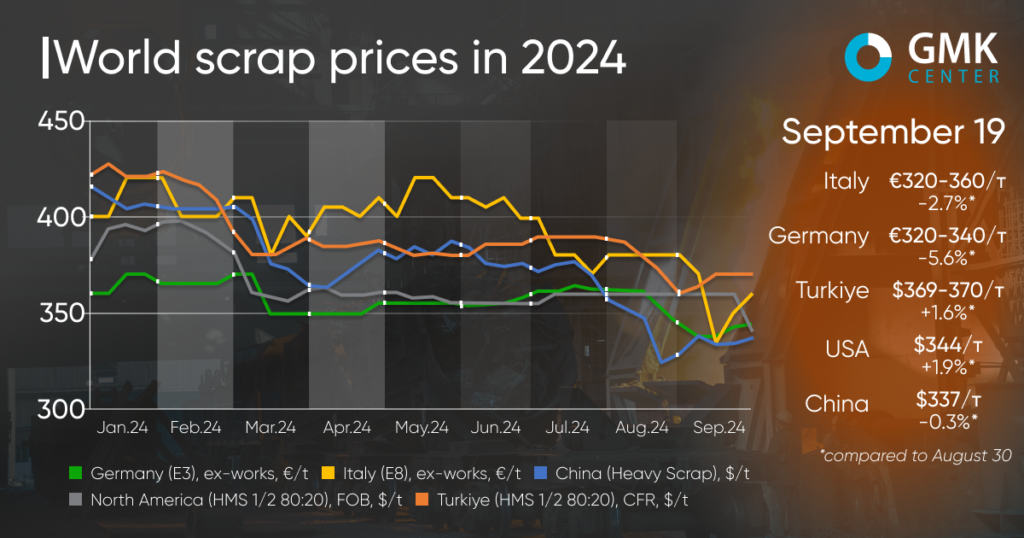

Global scrap prices have not shown a clear trend since the beginning of September. In some markets, raw material prices continued to decline without support from major consumers, but Turkey and the United States saw a slight increase.

Prices for scrap in Turkey (HMS 1&2 80:20) have risen by 1.6% – to $359-370 per tonne CFR since the beginning of September. At the same time, scrap prices in the Turkish market fell by 5.9% in August and by 0.8% in July. The last increase in quotations was observed in June – by 2.6%, after a long decline since the beginning of the year.

The slight recovery in scrap prices in Turkey in early September is the result of improved demand for locally produced steel products from European consumers, as well as a short-term improvement in the steel market in China. In particular, prices for Chinese billets rose by $30-35 per tonne, but soon fell again. In addition, Turkey is expected to launch its long-awaited low-interest housing loan scheme soon, which will help to restore demand for construction steel and improve the outlook for the steel industry.

The Turkish scrap market saw a major price increase in the first week of September, but the situation has since stabilized. Suppliers of raw materials indicate that demand has slowed again, but price offers are unlikely to decline as this is impossible due to weak collection and rising dock handling costs.

Although Turkey’s need for scrap is obvious, most market participants do not expect another significant rise in scrap prices, given the further decline in imported billets, as well as the weakening of rebar and hot-rolled steel futures in China. The US Federal Reserve’s interest rate cuts may bring some optimism to the market, but uncertainty in China will continue to weigh on the market.

“Steel consumption is declining in Turkey’s domestic market, with a drop of 18.9% y/y in July. Steel production is supported by exports, and there are chances that exports may increase given the anti-dumping investigations in the EU against imports of hot-rolled coils from Egypt, India, Japan and Vietnam. We expect that monthly demand for scrap in Turkey will remain within the average figure recorded over the past 7 months until the end of the year,” said Andriy Glushchenko, GMK Center analyst.

In the European market, scrap prices fell between August 30 and September 19, 2024. In particular, in Germany, scrap quotations (E3 Demolition Scrap) decreased by 5.6% – to €320-340/t Ex-Works, and in Italy (E8 Light New Scrap) – by 2.7%, to €320-360/t Ex-Works.

The overall market is rather negative. Local steel producers are gradually resuming activity after a long summer break. The decline in prices is mainly due to weak demand for steel.

Some market participants point out that scrap prices are close to bottoming out, as scrap companies are facing a shortage of raw materials and declining inventory levels. However, on the other hand, the decline in steel production in response to high energy costs and low order volumes is balancing the scrap market.

Suppliers believe that European scrap prices will stabilize in the near future and stop declining, maintaining current levels through October. The forecast is based on a significant decline in scrap collection in August and September.

In the North American market, scrap prices have risen by 1.9% – to $344/t Ex-Works since the beginning of September. Despite a slight increase in supply, the overall mood is negative. As the order books of US steelmakers are rather weak, some mills are expected to idle some capacity in September and October. Since the beginning of the month, the growth of prices for hot-rolled plates has been rather shaky and cannot support the scrap market.

In China (Heavy Scrap), scrap prices fell by 0.3% – to $336.98 per tonne during this period. There was a bigger drop in early September, but prices have been gradually recovering since then. Some growth in quotations reflects the improving situation on the steel markets along with a limited supply of scrap. Currently, the price offer is regulated by the availability of raw materials on the market. Suppliers have to balance supplies to keep price levels at acceptable levels amid volatile steel market conditions.

-

Opinions Industry steel consumption

13 July 2026

15 July 2026

15 July 2026

15 July 2026