News Global Market iron ore prices 4324 29 September 2025

January quotes on the Dalian Commodity Exchange rose by 2.7%, while September contracts on the Singapore Exchange rose by 2%

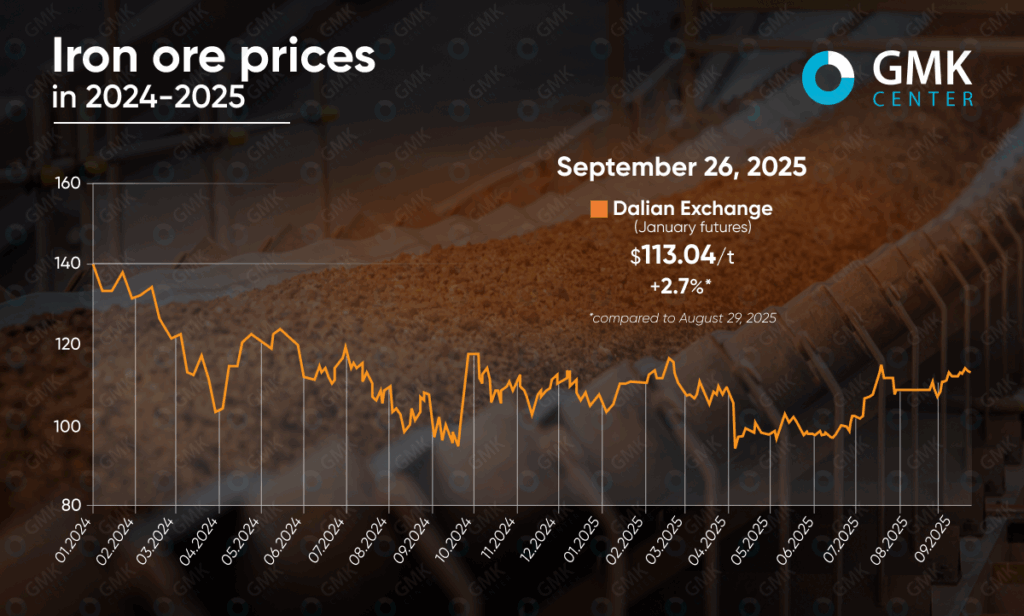

Iron ore prices fluctuated within a narrow range in September. Despite this, the market recorded a 2.7% increase in January quotations on the Dalian Exchange to $113.04/t as of September 26, 2025 (compared to August 29), while September contracts on the Singapore Exchange reached $105.6/t (+2%).

During the month, prices fluctuated under the influence of several key factors. In early September, there was an increase caused by supply constraints due to possible delays in the implementation of the Simandou mining project in Guinea. This created a certain shortage of expectations in the market and supported quotations. At the same time, the resumption of pig iron production at Chinese steel mills boosted demand, and pre-holiday restocking ahead of the National Day of the People’s Republic of China ensured activity on the spot market.

However, from the middle of the month, the dynamics became more unstable. The market reacted to rumors of possible restrictions on steel production in Tangshan, which could reduce the demand for ore. At the same time, weak performance in China’s construction sector put pressure on prices, as construction remains the main consumer of rebar and rolled products.

External events became an additional factor of instability. The US Federal Reserve’s decision to cut interest rates in September did not provide the expected support to commodity markets, as participants believed that monetary policy easing was already priced in. The market was also affected by news of growing global trade tensions, including calls for new tariffs on Chinese and Indian products.

At the end of September, activity declined sharply due to the approaching Golden Week holiday in China. Most mills completed their purchases before September 25, which led to a slowdown in spot prices.

Overall, the market balanced between supply and demand in September, with short-term factors—from typhoons in southern China to rumors of new regulatory changes—causing rapid fluctuations. Despite local declines, the average monthly trend was moderately positive.

Market expectations for October are cautious. On the one hand, demand may recover after the holidays, and expected steel production restrictions will keep the market in balance. On the other hand, the first exports from Simandou and China’s macroeconomic weakness could hold back further growth. It is clear that the iron ore market will remain sensitive to any signals from both demand and supply.

As reported by GMK Center, Moody’s expects iron ore prices to remain at $80-100/t in the next 12-18 months. This forecast is due to weak demand from China and high supply on the global market.

A similar view was expressed by analysts at BMI Country Risk and Industry Research. They maintain their forecast for the average annual price for 2025 at $100/t, although they acknowledge the pressure from weak demand.

-

Opinions Industry steel consumption

13 July 2026

13 July 2026

13 July 2026

13 July 2026