News Global Market iron ore prices 3576 17 March 2026

The market was buoyed by China’s stimulus measures, higher freight rates, and supply risks, but high inventories are holding back further growth

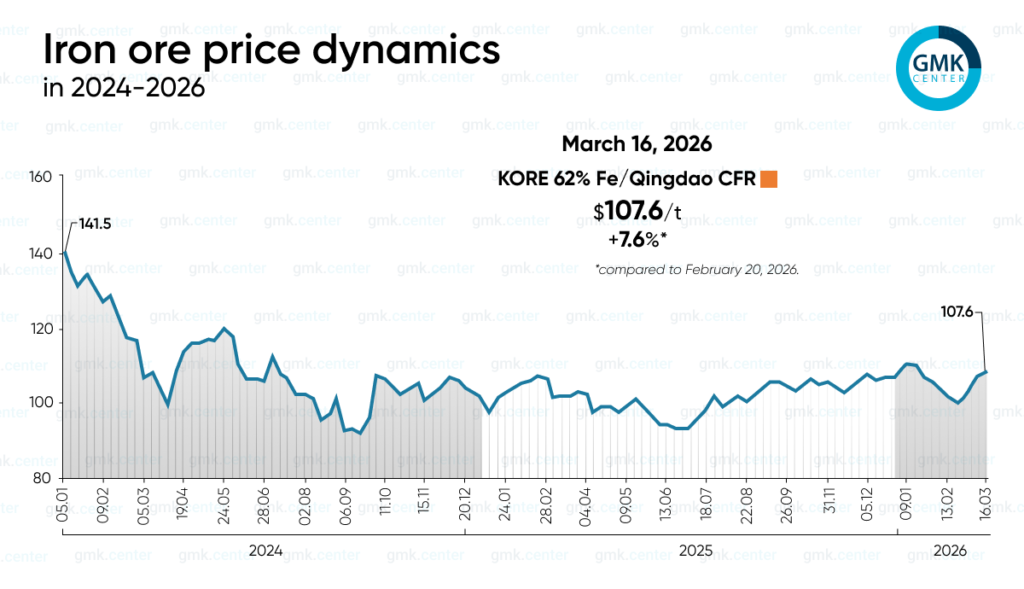

The global iron ore market rebounded in March following a weak February, when prices hovered around $100/t CFR (KORE 62% Fe/Qingdao). As of March 16, prices had risen to $107.58/t, up 7.6% from the previous month and 0.6% from the start of the year.

The main driver of growth in March was not so much a fundamental shift in demand as a combination of macroeconomic signals from China, logistical risks, and short-term supply concerns.

The first supportive factor was expectations surrounding China’s “Two Sessions.” Although the market viewed the announced stimulus measures as modest, signals of record-high budget spending, new government bonds, and transfers to local authorities improved sentiment in the futures market. An additional positive factor was the government’s GDP growth target of around 4.5–5%, which market participants viewed as potential support for steady demand and consumption of raw materials.

The second driver of the March rally was geopolitics. Escalating tensions in the Middle East pushed up oil prices and freight rates, which automatically supported ore prices due to rising logistics costs. Concerns about ships passing through the Strait of Hormuz, the rerouting of cargo, and the accumulation of additional costs for shipowners created a risk premium that was particularly noticeable at the beginning of the month.

Rumors and reports of restrictions on certain BHP ore grades in China became a separate speculative factor. The market reacted sharply to news regarding China Mineral Resources Group’s actions concerning Mac fines, Newman fines, Newman lumps, and the previously suspended Jimblebar fines. It was precisely these supply risks that drove the price of KORE 62% Fe from $101.73/t on March 2 to over $107/t by mid-month. However, when signs emerged that these restrictions were easing, part of the gains quickly evaporated.

At the same time, the fundamental picture remains subdued. Chinese ports maintain historically high ore inventories, and steel mills continue a cautious procurement policy with low inventory levels. Demand is gradually improving thanks to rising pig iron output following the end of temporary production restrictions, but steelmakers’ margins remain weak and finished steel inventories are high. This is limiting the pace of capacity restarts and preventing the market from shifting to a sustained upward trend.

The February decline, in turn, was largely due to seasonal factors: after restocking ahead of the holidays in January, Chinese steel mills cut back on purchases amid the Lunar New Year, while port activity slowed. Although China’s imports in January–February set a record for this period, February shipments specifically were lower month-over-month, which temporarily weighed on the market.

The near-term outlook for iron ore appears mixed. On the one hand, prices are supported by higher freight rates, a gradual recovery in pig iron output, and improved macroeconomic expectations for China. On the other hand, oversupply, high port inventories, and producers’ caution will limit further price increases. Therefore, the March rise appears to some extent as a rebound from February’s decline rather than the start of a new strong upward cycle.

-

Opinions Industry steel consumption

13 July 2026

21 July 2026

21 July 2026

21 July 2026