News Global Market scrap metal 3726 31 October 2024

A slight increase in offers was recorded in China and Italy

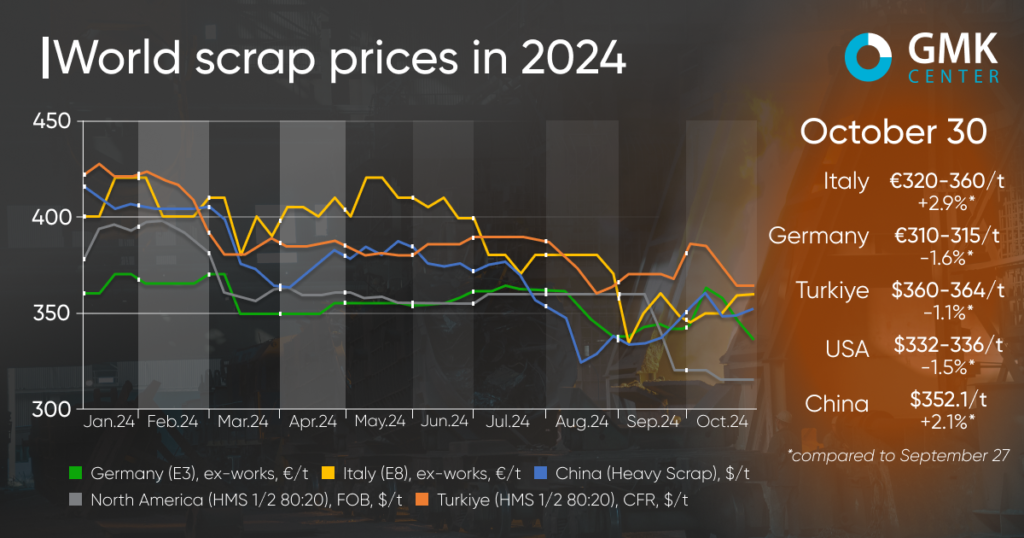

The global scrap market showed mixed trends in October. Most regions saw a decline in prices due to weak demand and high inventories, while in Italy and China, prices rose slightly due to increased demand and limited supply.

Prices for scrap metal in Turkey (HMS 1&2 80:20) decreased by 1.1% in the period from September 27 to October 30, 2024, after rising by 1.1% in September to $360-364/t CFR. This means that supply has returned to the level of August. At the same time, the market was volatile during the month, with prices fluctuating in the range of $364-390/t CFR due to the impact of global economic factors and domestic demand dynamics.

The beginning of October was marked by an increase in scrap prices in Turkey to $390/t due to increased demand from local steel companies and hopes for a revival in the Chinese steel market after the economic stimulus announced in late September. However, China failed to meet market players’ expectations, and raw material prices mostly stabilized and began to decline in mid-October.

Nevertheless, the demand for scrap in November remained strong, which supported prices at the beginning of the month. The market remained relatively stable, but gradually succumbed to pressure from plants that lowered their price targets.

By the end of the month, scrap prices fell to $360-364 per tonne, driven by overall weak demand and a lack of expected support from Chinese consumers. This factor was also influenced by an increase in supply from Europe and the US. After the euro stabilized, exporters from the Benelux countries tried to maintain prices, but Turkish mills continued to insist on lower levels. Rebar prices in the Turkish domestic market were also under pressure in October. This was also reflected in the cost of scrap, forcing suppliers to cut prices.

In the short term, scrap prices in Turkey are expected to remain stable or continue to decline as demand for November supplies has already been met. However, in the run-up to the winter season, prices may stabilize or even rise slightly, given the limited supply of scrap and expectations of new stimulus measures from China.

The European market showed mixed trends in October. In particular, in Germany, due to low demand and limited exports, scrap prices (E3 Demolition Scrap) decreased by 1.6% – to €310-315/t Ex-Works. Demand for scrap remained weak due to a decline in steel production, especially from producers of high-quality steel for the automotive industry. The outlook for further purchases also remained restrained amid lower demand from Turkey and weak economic growth in the region.

In Italy, on the other hand, scrap prices (E8 Light New Scrap) increased by 2.9% to €320-360/t Ex-Works, due to a lack of supply of certain types of scrap and low collection volumes. Supply problems have forced some producers to raise purchase prices, especially for rare grades such as E5 and high-grade E8. At the same time, a number of producers are planning production shutdowns for November, which will reduce demand for scrap in the short term.

The decline in production activity and significant plant shutdowns in November in both countries will affect the demand for scrap in Europe. However, the expected winter supply reduction and a possible increase in demand from Turkey may support prices.

The US scrap market in October saw a 1.5% decline in prices to $332-336/t Ex-Works due to low demand and rising inventories. The rise in prices in Turkey at the beginning of the month temporarily supported optimism, but the gradual weakening of demand in China and Turkey again lowered prices. It is expected that in November, scrap prices in the United States may remain stable or continue to decline due to low demand and economic uncertainty before the election.

In China (Heavy Scrap), scrap prices for this period increased by 2.1% – to $352.1/t. The price increase was driven by the resumption of activity in the construction market after the holidays. An additional factor was the increase in domestic demand in China, which contributed to the overall strengthening of prices. In the short term, prices are expected to stabilize, but future dynamics will largely depend on government stimulus policies.

-

Opinions Industry steel consumption

13 July 2026

15 July 2026

15 July 2026

15 July 2026