News Global Market ціни на газ 2059 17 May 2026

The market is under pressure from the conflict in the Middle East and the need to replenish inventories

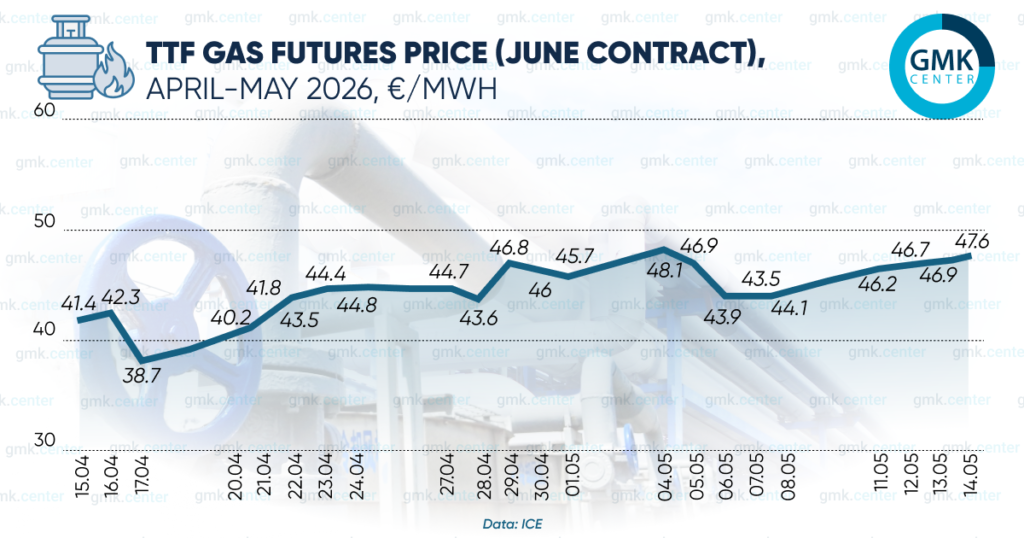

The key factors shaping the European gas market in May are the conflict in the Middle East, the need to replenish inventories, rising structural demand, and unstable weather conditions. At the same time, prices this month have not yet reached the highs seen in March and April.

According to ICE, the highest monthly TTF futures prices were recorded on May 4 (over €48/MWh) and May 15—the price of over €49/MWh on that day marked the highest level in the past five weeks.

Overall, in the first half of May, European gas prices have fluctuated between €44 and €49/MWh.

According to data from the AGSI platform, as of May 15, 2026, European gas storage facilities were 35.85% full (on the same date in 2025, the figure was 43.64%).

Torgrim Reitan, CFO of Norway’s Equinor, expressed the view during a conference call with analysts in early May that it would be difficult for Europe to replenish its gas storage facilities to the target level of 80% by the start of the next winter season. He cited price discrepancies (near-term contracts are more expensive than those for next winter) and lower-than-expected supply levels. Reitan noted that this means the European gas market will be vulnerable to weather events and operational issues in the future.

The Financial Times had previously offered a similar assessment. According to traders and companies, by the end of April, summer prices had risen to winter levels due to supply constraints stemming from the conflict in the Middle East and the EU’s target of filling storage facilities to 80% capacity.

In particular, as noted by Henning Gloystein, an expert at Eurasia, the filling process will proceed more slowly than under normal market conditions. According to him, the lack of market incentives to replenish stocks creates the risk that gas will have to be purchased on the spot market in winter at higher prices.

On May 13, the European lobbying groups Eurogas and the International Association of Oil and Gas Producers (IOGP) called for greater flexibility in meeting the bloc’s targets to avoid putting pressure on the market during the summer season. Current regulations allow for a 10 percentage point deviation from the target of filling storage facilities to 90% capacity by the start of the heating season. In the event of adverse market conditions, an additional 5 percentage point deviation may be applied.

At the same time, according to the energy analysis center IEEFA, the conflict in the Middle East is making the EU increasingly dependent on LNG from the United States—by 2026, the U.S. will account for two-thirds of its imports. The U.S. may even surpass Norway in terms of supply share. Norway accounted for 30% of total gas imports to the EU in the first quarter of this year, while the United States accounted for 29%.

Imports of American LNG to Europe from 2021 to 2025 have already more than tripled amid the shift away from Russian pipeline gas. Overall, as noted by the IEEFA, the increase in LNG supplies from the global market also makes the EU vulnerable to sharp price spikes during periods of geopolitical turmoil.

Earlier, on April 22, the European Commission unveiled plans to combat high energy prices. The bloc will also avoid major market interventions, such as gas price caps or taxes on energy companies’ windfall profits, similar to those implemented in 2022. Coordinated gas purchases among member states are also planned.

-

Opinions Industry macroeconomics

28 May 2026

06 June 2026

05 June 2026

05 June 2026