Infographics EU 790 05 May 2026

Weak steel production held back demand, while exports stabilized, with a focus on Turkey and Egypt

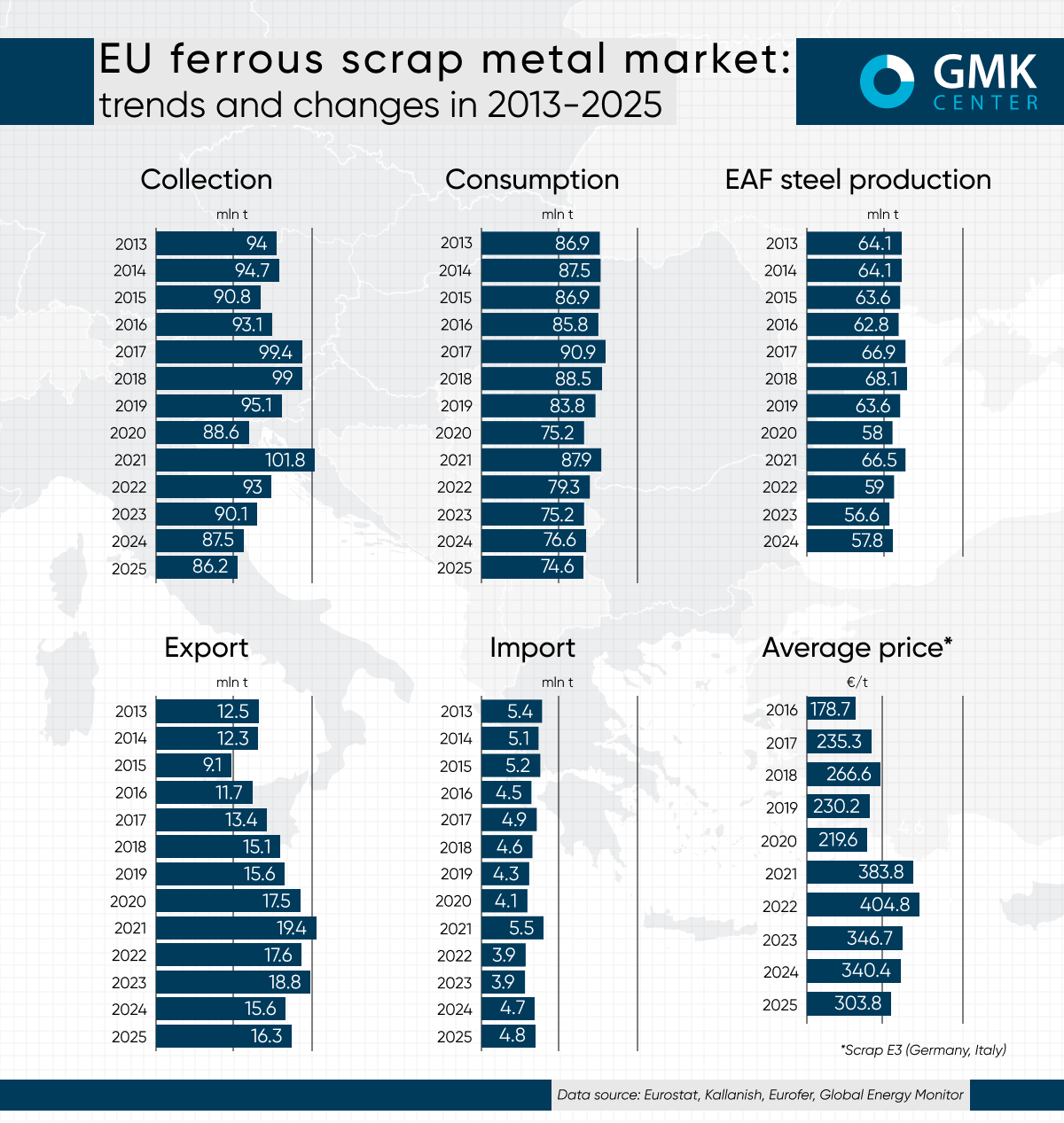

The EU scrap market in 2025 remained under the influence of weak conditions in the steel market, but showed signs of stabilization following the previous year’s decline. The key factor remained the green transition, which shapes long-term scrap demand but has not yet offset the cyclical decline in steel production.

Supply and consumption

Based on estimates of specific scrap consumption, scrap demand in 2025 fell by 2.6% year-on-year to approximately 74.7 million tons, reflecting the decline in EU steel production to 126.2 million tons (-2.6% year-on-year). At the same time, scrap collection declined to a lesser extent—by 1.6% year-on-year, to 86.2 million tons.

Thus, the gap between supply and demand persisted, which supported export activity. The main reason for the decline in demand remained insufficient utilization of electric arc furnaces. With existing EAF capacity of about 78 million tons, their utilization remains below potential, which is holding back domestic scrap consumption.

Raw material prices

The average price of E3 scrap in the EU in 2025 was €303.8/t, a 10.8% decrease compared to 2024. The decline reflects weak demand from steelmakers and subdued activity in key steel-consuming sectors. At the same time, prices remain significantly higher than the 2016–2020 levels, confirming the strategic role of scrap in the context of decarbonization.

Exports and imports

In 2025, scrap exports from the EU to third countries totaled 16.31 million tons, a 4.4% increase year-on-year. The figure rebounded after a sharp 16.6% drop in 2024 but remains at significantly lower levels.

Turkey remains the key destination, importing 10.78 million tons of scrap (+2.2% year-on-year) and accounting for over 65% of total EU exports. Egypt showed the fastest growth among major buyers—up 11.6% to 1.83 million tons—solidifying its position as the third-largest importer.

At the same time, India reduced imports to 1.02 million tons (-6.7% y/y), which is nearly half the volume of 2023. Pakistan also cut purchases by 10.5% to 585,000 tons, reflecting weak demand in South Asia.

Among exporting countries, the Netherlands leads the way with 3.67 million tons (+50.7% y/y), becoming the key driver of the redistribution of trade flows. Next are Belgium (2.59 million tons; +5.1% y/y), Germany (1.23 million tons; +10.5% y/y), and Poland (1.2 million tons; -8.6% y/y).

Scrap imports to the EU in 2025 increased by 1.2% year-on-year – to 4.8 million tons, maintaining the region’s status as a net exporter with net exports of approximately 11.7 million tons.

Outlook

In the short term, the market will remain dependent on trends in steel production. At the same time, in the medium and long term, demand for scrap in the EU will grow alongside the expansion of EAF capacity and the implementation of climate policy. This will gradually reduce the region’s export potential and intensify competition for high-quality raw materials.

-

Opinions Industry steel consumption

13 July 2026

22 July 2026

20 July 2026

06 July 2026