News Global Market DRI 1120 08 June 2026

The main suppliers include Venezuela and the United States

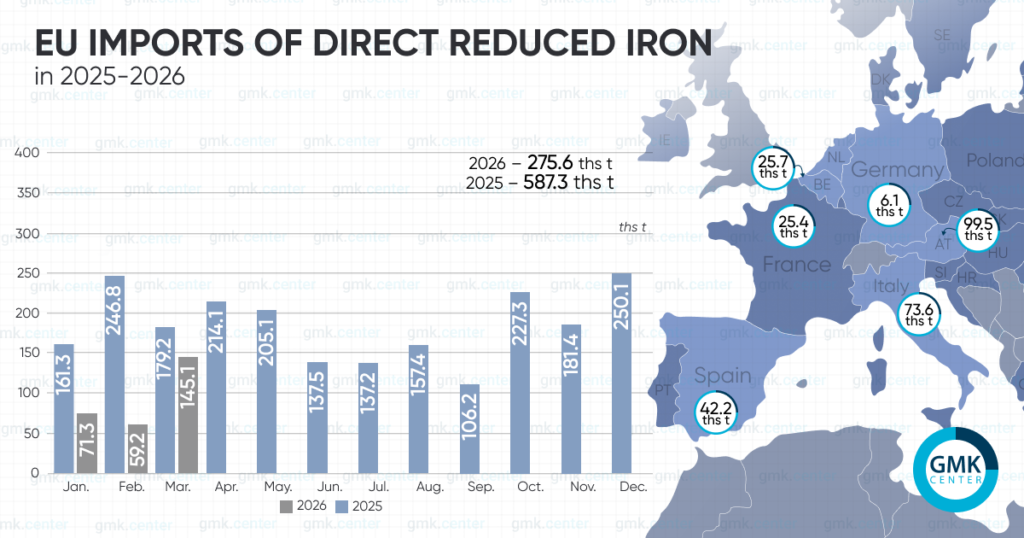

According to figures for January–March 2026, EU steelmakers reduced their imports of direct reduced iron (DRI) by 53.1% compared with the same period in 2025, to 275,650 tonnes. This is according to calculations by the GMK Center based on Eurostat data.

The main supplier during the period was the US – 102.5 thousand tonnes, which is 5.3% less compared to the same period in 2025. Almost the entire volume was shipped to Austria – 99.48 thousand tonnes (+12.7% y-o-y).

A further 73.64 thousand tonnes of DRI imports arrived in the EU from Venezuela. Volumes fell by 52.6% compared to January–March last year. The entire volume was shipped to Italy. Libya also supplied 33.34 thousand tonnes of the product to the EU (-62.5% y-o-y). The entire volume was shipped to Spanish consumers.

In March, DRI imports to the EU were estimated at 145.14 thousand tonnes (-19% y/y; +145.2% m/m). This is the highest figure since the start of the year, as deliveries in January amounted to 71.32 thousand tonnes (-71.5% month-on-month; -55.8% year-on-year), and in February to 59.19 thousand tonnes (-17% month-on-month; -76% year-on-year).

It should be noted that in 2025, the EU reduced its imports of direct reduced iron by 20% compared with the previous year, to 2.203 million tonnes. In 2024, this figure increased by 16.9% year-on-year.

The trend in DRI imports to the EU in 2024–2025 largely reflects both a shift in supply channels and the weak conditions of the European steel market. The growth in 2024 was partly explained by the greater volumes of Russian DRI/HBI available under the EU’s transitional quotas: as of 2024, these stood at 1.14 million tonnes, whereas for 2025 they were reduced to 651,900 tonnes. Last year, imports fell against a backdrop of weak demand for steel in the European Union, where real consumption declined for the third consecutive year, and steel production fell to 126.2 million tonnes.

Despite this, the structure of supplies continued to change: the EU was increasingly replacing Russian supplies with imports from Venezuela, the US, and Libya. Full replacement has not yet taken place, as even in 2025, Russia remained one of the largest suppliers of DRI to the EU market. From 2026, imports of Russian DRI/HBI have already been completely halted, so the European market’s shift towards alternative suppliers is set to intensify further.

-

Opinions Industry steel consumption

13 July 2026

24 July 2026

24 July 2026

24 July 2026