Infographics DRI 2312 25 March 2025

More than 38% of supplies come from Russia

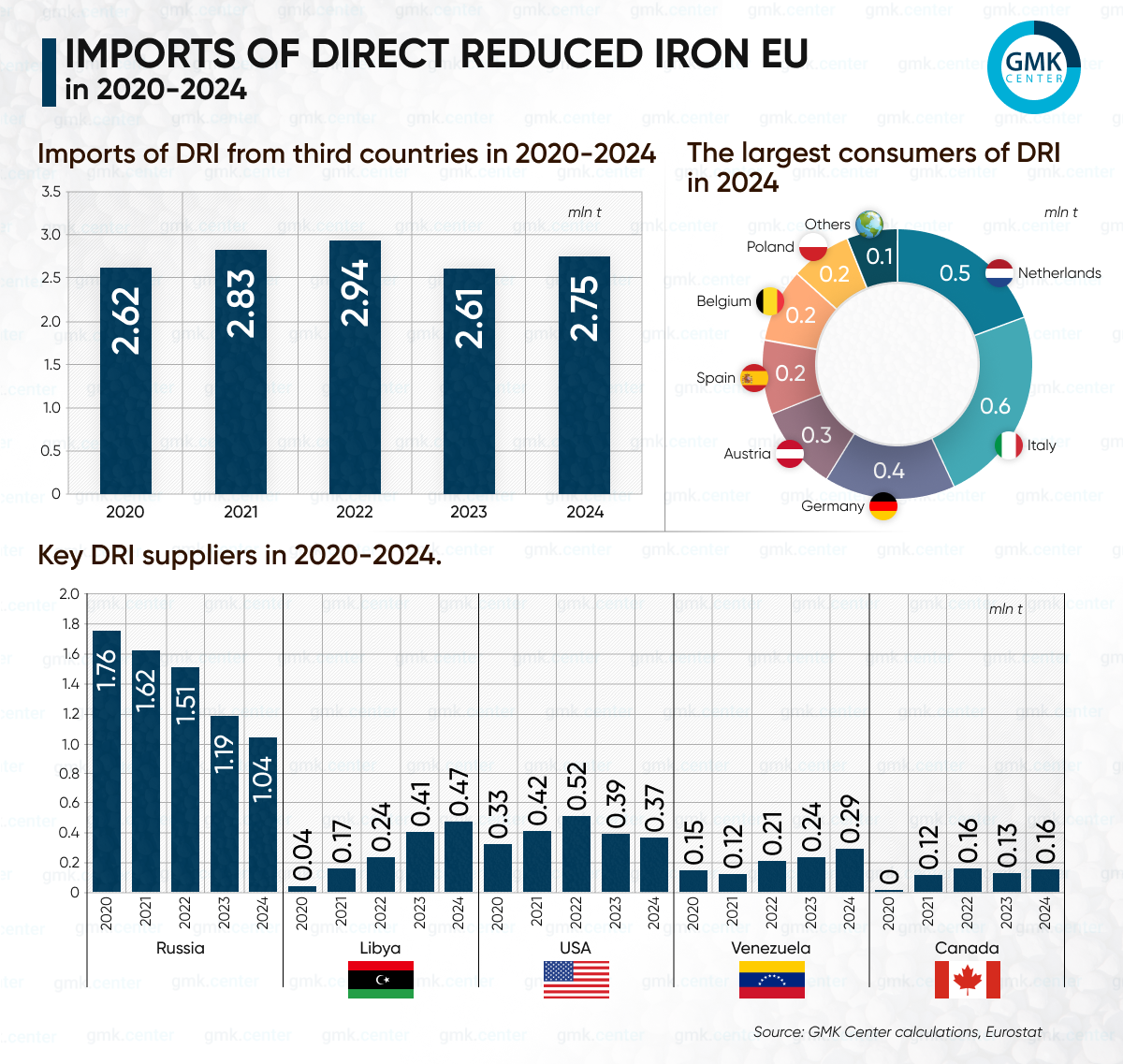

In 2024, steel enterprises of the European Union (EU) increased imports of direct reduced iron (DRI) from third countries by 5.4% compared to 2023, up to 2.75 million tons. In 2023, there was a drop of 11.1% y/y. This is according to GMK Center’s calculations based on Eurostat data.

The largest importers of DRI among the EU member states last year were:

- Italy – 659.73 thousand tons (-23.7% y/y);

- Netherlands – 527.27 thsd tonnes (+423%);

- Germany – 438.46 thsd tonnes (-33.5%);

- Austria – 276.51 thousand tons (+58.4%);

- Spain – 247.07 thsd tonnes (-1.6%);

- Belgium – 238.62 thousand tons (-7.6%);

- Poland – 202.81 thsd tonnes (+209.9%).

Thus, several countries, including the Netherlands and Poland, contributed to the annual growth of the overall figure, while most consumers reduced imports of direct reduced iron.

Traditionally, the key suppliers of DRI to the EU in 2024 were the Russian Federation, Libya, the United States, Venezuela, and Canada. These countries account for about 85% of the bloc’s raw material supplies, with Russia accounting for 38%.

Thus, European steelmakers consumed 1.04 million tons of DRI of Russian origin during the year, down 12.2% y/y. The bulk of it went to Italy – 487.99 thousand tons (-30.8% y/y), Belgium – 207.16 thousand tons (+0.7%), and Poland – 202.8 thousand tons (+210%).

In 2024, Libya supplied 475.53 thousand tons (+16.6% y/y) of direct reduced iron to the EU market, the United States – 368.63 thousand tons (-6.3%), Venezuela – 294.81 thousand tons (+23.8%), and Canada – 158.42 thousand tons (+16.8%).

The increase in DRI imports to the EU in 2024 indicates that demand for this raw material among European steelmakers remains strong, although the supply structure remains heterogeneous. High dependence on Russian exports continues to be a challenge for the EU, especially given the sanctions policy and the need to diversify supply sources. At the same time, countries such as Libya, Venezuela, and Canada have increased their supplies to the EU, which opens up prospects for further market reorientation.

The significant increase in imports in the Netherlands and Poland demonstrates the change in supply chains and the adaptation of individual countries to new market conditions. However, the overall decline in imports among leading consumers, such as Germany and Italy, may indicate a change in the strategy of using DRI or the impact of economic factors.

Going forward, the key issues for the market will be the stability of supply, the impact of the EU’s regulatory policy on DRI sourcing, and the development of domestic direct reduced iron production within Europe.

-

15 June 2026

18 June 2026

17 June 2026

04 June 2026