News Global Market сляби 1449 12 November 2025

Brazilian factories ramp up production of semi-finished products

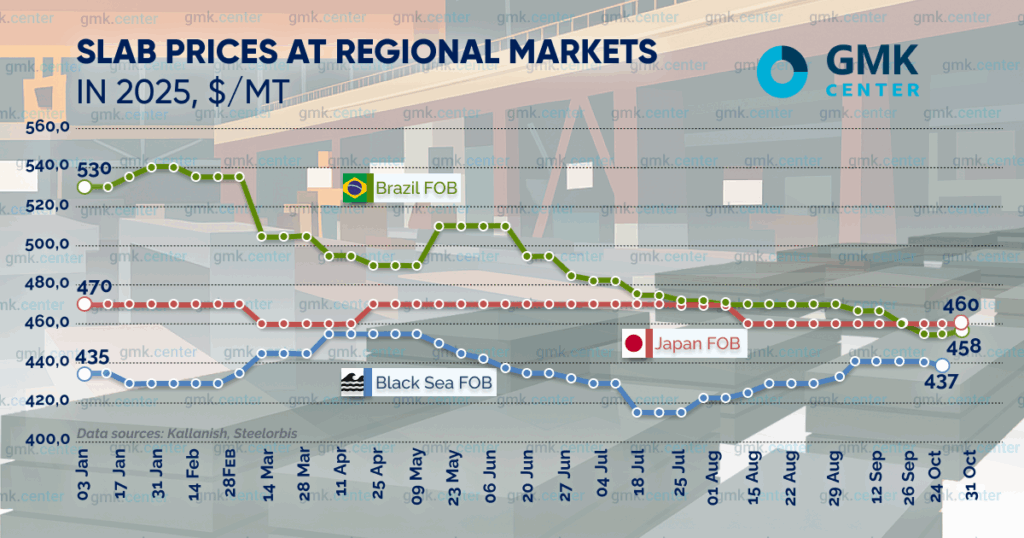

Regional slab markets saw mixed price trends in October. According to SteelOrbis, the benchmark export price for Brazilian slab rose slightly in October, by $3, to $458/t (FOB). After a period of instability and price declines caused by the US imposing a 50% tariff on Brazilian goods, including a significant portion of metallurgical products, in early August, the situation for slab improved.

The positive dynamics were reflected in production figures. In September, Brazilian mills increased their output of semi-finished products by 18% compared to August, to 780,000 tons, of which 707,000 tons were slabs. At the same time, production of semi-finished products in the first nine months of 2025 fell by 10.3% year-on-year, to 6.2 million tons.

At the same time, as Kallanish notes, in September, the Brazilian metallurgical sector saw a slowdown in business activity: capacity utilization fell to 66% from 67.5% in August. According to the Brazilian Steelmakers Association (IAB), steel production in the country in September decreased by 2.3% compared to August, to 2.8 million tons. At the same time, steel production in January–September decreased by 1.7% year-on-year, to 25 million tons.

As for other regions, average slab prices in Japan remained unchanged in October at $460/t. Meanwhile, average FOB Black Sea quotations fell slightly last month to $438/t from $440/t in September.

In Turkey, recent changes in the domestic processing regime (DIR), which require the purchase of at least 25% of the raw materials/semi-finished products needed for production on the domestic market, had a minimal impact on demand for imported slabs.

This is because domestic slab production capacity is insufficient to meet domestic demand. In September, Turkey’s own slab production increased by 4.8% year-on-year to 1.15 million tons. At the same time, in the first nine months of this year, production of the product decreased by 4.1% year-on-year to 10.25 million tons.

At the same time, imports of the product remain quite high. According to the Turkish Statistical Institute (TUIK), slab imports to Turkey in September decreased by 11% year-on-year to 299,600 tons after growing by 34% year-on-year in August. At the same time, the structure of supplies changed significantly again in September. Russia increased its share to 59% from 36% in August, while China, which accounted for 25% of the August market, disappeared from the list of importing countries. Overall, in January–September, slab imports to Turkey increased by 8% year-on-year to 3 million tons.

The average price of slab imports to Turkey in September was $459/t, compared to $471/t in August. The price difference between the largest importers was quite significant: Russia supplied slabs at an average price of $446/t, while Malaysia (18% of September’s supply) supplied them at $495/t.

As for price benchmarks, it should be noted that the average benchmark price for slabs – hot-rolled coil (HRC) – remained at $485/t (on China FOB terms) at the beginning and end of October, although in the middle of the month, quotations fell by $5 per tonne amid declining demand and increased uncertainty. The rise in HRC prices in China at the end of the month contrasted with cautious demand worldwide. At the same time, regional markets saw mixed dynamics: prices in Asia and the Middle East mostly declined, while Europe saw cautious growth or attempts to raise prices.

It should be noted that at the end of September, regional markets saw mixed price trends for slabs. The average export price of Brazilian slabs in September fell by $15 to $455/t (FOB).

-

15 June 2026

23 June 2026

23 June 2026

23 June 2026