News Global Market ціни на напівфабрикати 1612 10 May 2026

Prices for Asian slabs continued to rise amid a supply shortage

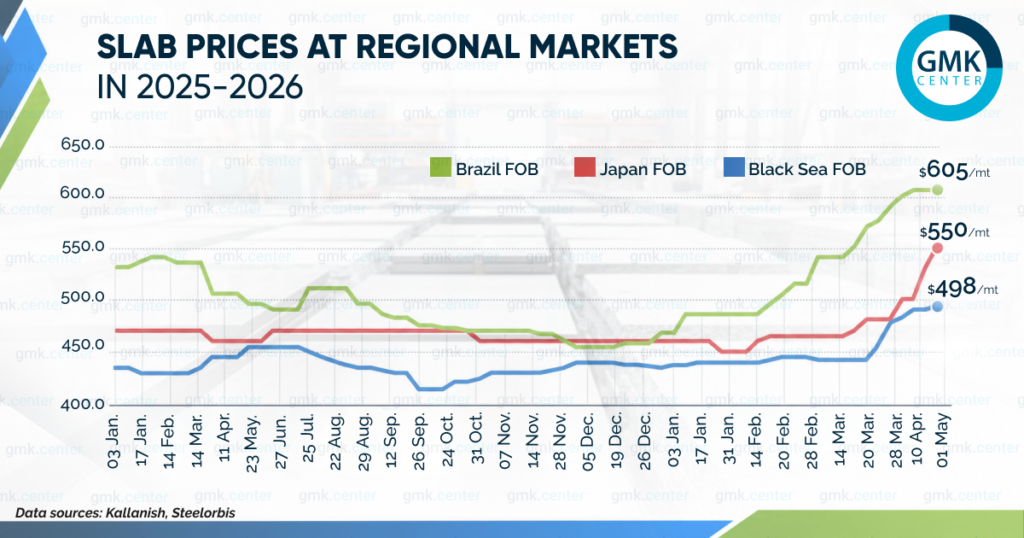

Prices continued to rise across all regional slab markets in April, with increases mostly ranging from $15 to $20 per ton. The sharpest price increase was recorded in Japan, where average prices rose by $70 in April to $550/t.

Brazil

According to SteelOrbis, the reference export price for Brazilian slabs rose by $15 in April to $605/t (FOB), a two-year high. Export prices for Brazilian slabs remained high due to strong domestic demand.

Reserves for the domestic market remain in place. According to the Brazilian Steel Manufacturers Association (IAB), local mills increased slab production by 25.5% in March compared to February, reaching 763,000 tons. Production in the first quarter totaled 1.9 million tons.

Slab exports from Brazil are highly volatile. By the end of March, the figure had fallen by 63% to 298,000 tons, compared to 794,000 tons in February (+93% m/m). The sharp decline in exports in March (as well as the increase in February) is linked to the dynamics of shipments to the U.S.—their volume fell to 239,000 tons at a price of $594/ton (FOB) compared to 537,000 tons at $552/ton (FOB) a month earlier.

With the launch of CBAM, Brazilian slabs offer European importers a significant price advantage compared to other supplier countries. In March, Brazil exported 32,000 tons of slabs to France at $473/ton (FOB) and 27,000 tons to Germany at $477/ton (FOB). France and Germany accounted for 11% and 9% of exports, respectively.

Turkey

Average FOB Black Sea prices rose by $20 in April to $498/t, compared to $478/t at the end of March. This level marked the highest since the beginning of last year. The main drivers of the increase remained the global trend of rising slab prices due to reduced supplies from Iran and high freight rates.

According to the Turkish Statistical Institute (TUIK), slab imports to Turkey rose by 35% m/m in March to 179,000 tons, following a 56% MoM decline in February. The average import price was $464/t. The largest suppliers in March were Russia (102,000 tons, -10% y/y) and Malaysia (52,000 tons, -48% y/y). Overall, slab imports to Turkey totaled 617,000 tons for January–March.

Despite rising prices, demand in Turkey’s key market remains limited: local producers are switching to domestic raw materials. Since the beginning of this year, the Turkish domestic market has seen a significant increase in production: in March, output rose by 25% year-on-year to 1.45 million tons, and for January–March, by 17% year-on-year – to 4 million tons.

Other markets

Price trends in other regional markets also remained upward. Prices for slabs from Asian producers continued to rise amid a shortage of supply at acceptable prices. Steel semi-finished products from Iran will not appear on the market before June: the Iranian authorities have imposed an export ban until that time.

Iranian slabs are unlikely to appear on the market for a long time, as airstrikes on March 27 against the Iranian Khuzestan Steel plant (which specializes in steel semi-finished products—billets, blooms, and slabs—for export markets) led to a suspension of production. It is worth noting that according to the Iranian Steel Producers Association (ISPA), in the Iranian calendar year ending March 20, 2026, slab production increased by 10.2% year-on-year, to 12.4 million tons.

At the same time, average slab prices in Japan rose by $70 in April – to $550/ton.

It should be noted that in March, all regional slab markets also saw price increases of $15–35 per ton. This was driven by rising demand in the U.S., Europe, and Southeast Asia, as well as a supply shortage linked to the withdrawal of Iranian steel semi-finished products from the market.

-

Opinions Industry macroeconomics

28 May 2026

03 June 2026

03 June 2026

03 June 2026