News Global Market rebar prices 6115 05 March 2026

Turkish producers are trying to stimulate demand through discounts

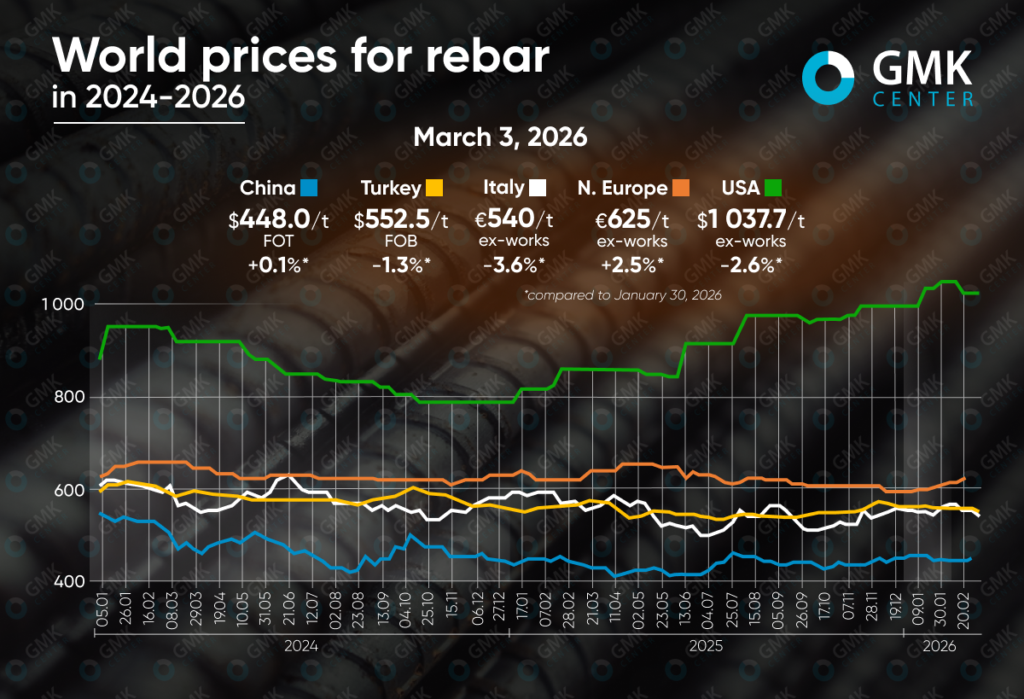

Global prices for rebar declined in most world markets during February. A slight increase was recorded in China and Northern Europe.

Turkey

Reinforcing steel offers on the Turkish market fell by 1.3% – to $552.5/t FOB between January 30 and February 3, 2026. The decline continued throughout the month, and prices are now at their lowest since early November.

Throughout February, the market was under pressure from weak demand both domestically and abroad. Turkish mills were forced to gradually lower their quotations despite relatively stable scrap prices, which further reduced producers’ margins. Weak activity in the domestic market was exacerbated by financial constraints and high inventories among traders, while the approach of Ramadan further reduced construction activity.

An additional factor of pressure was competition from North African suppliers, who offered rebar at $535-545/t FOB. At the same time, export sales to EU countries remained limited due to the impact of CBAM, although individual deals with Romania and Bulgaria were still concluded. Other traditional markets, particularly the Balkans, Africa, and the Middle East, showed weak activity and mainly formed small batches of supplies.

In these conditions, manufacturers tried to stimulate demand through discounts and deferred payments, which allowed them to periodically boost sales in the domestic market.

In the long term, prices for Turkish rebar are likely to remain under pressure from weak demand. At the same time, stable scrap prices and potential growth in interest from European buyers due to high domestic prices in the EU may provide some support to the market.

EU

Prices for rebar in the EU also declined. In Italy, in particular, the decline in February was 3.6%, to €540/t ex-works. In Northern Europe, prices rose by 2.5% to €625/t ex-works between January 30 and February 20, but offers are likely to have fallen at the beginning of March.

The EU rebar market was influenced by conflicting factors in February. On the one hand, producers tried to raise prices due to a significant increase in production costs. Higher electricity and gas prices, as well as an increase in scrap prices by approximately €40/t compared to the end of 2025, forced steelmakers to seek an increase in contract prices by €20-30/t. An additional signal for the market was the price increase by ArcelorMittal.

At the same time, real demand remained weak. Construction activity was low in many countries, and in Italy it was further hampered by prolonged rains and a slowdown in residential construction. Distributors reported minimal purchasing volumes and bought only small batches of products. As a result, most of the announced increases failed to take hold in the market, and by the end of the month, prices in Italy began to decline.

In early March, the situation was further complicated by a sharp increase in energy costs in Europe, which forced some manufacturers to suspend sales in order to review prices.

The market may remain volatile in the future: on the one hand, weak demand will hold back prices, while on the other hand, a sharp rise in energy and scrap prices could trigger a new wave of price increases.

USA

The US rebar market saw a moderate decline in prices in February after a stable start to the year, falling 2.6% to $1,030.7/t ex-works. The current price level has been maintained for over two weeks.

In early February, the market was supported by limited supply and expectations of an increase in scrap prices, which rose by approximately $20-30/t due to winter disruptions in raw material collection. An additional supporting factor was trade restrictions on imports, in particular Section 232 tariffs, which restrained the inflow of foreign supplies and allowed domestic producers to maintain prices.

However, during the month, the market began to show signs of weakening. Demand in the construction sector remained sluggish, as confirmed by weak performance of new construction projects and a decline in architectural orders. At the same time, supplies of imported rebar and supply from domestic producers, including new capacities, increased. This intensified competition and reduced the risk of product shortages.

As a result, prices fell slightly at the end of the month, and some plants began to offer small discounts to support sales.

In the short term, the market is likely to remain relatively stable, while the expected revival of the construction season in the spring may provide additional support for prices.

China

The dynamics of the Chinese rebar market in February were largely determined by seasonal factors. Prices remained stable with a slight increase of 1% to $448.01/t FOT.

On the eve of the Chinese New Year celebrations, trading activity virtually came to a halt as most construction sites suspended work and end users reduced their purchases. In these conditions, spot prices remained almost unchanged, while futures prices were under pressure.

On the supply side, some electric steel mills temporarily halted production for the holiday period, which kept prices from falling. After the holidays, plants quickly resumed production, which led to an accumulation of inventories at major trading platforms and created additional pressure on the market. At the same time, demand recovered slowly as construction activity remained seasonally low and problems in the real estate sector continued to hold back steel consumption.

The market was supported to some extent by expectations of stimulus measures from the authorities ahead of political sessions in China, as well as possible production restrictions at individual enterprises.

Prices are likely to remain largely stable in the near term, while further dynamics will depend on the pace of recovery in the construction sector and new economic stimulus measures.

-

02 July 2026

09 July 2026

09 July 2026

09 July 2026