News Global Market slabs 6532 06 September 2025

The market continues to be dominated by low demand for finished rolled products and negative effects from US tariff policy

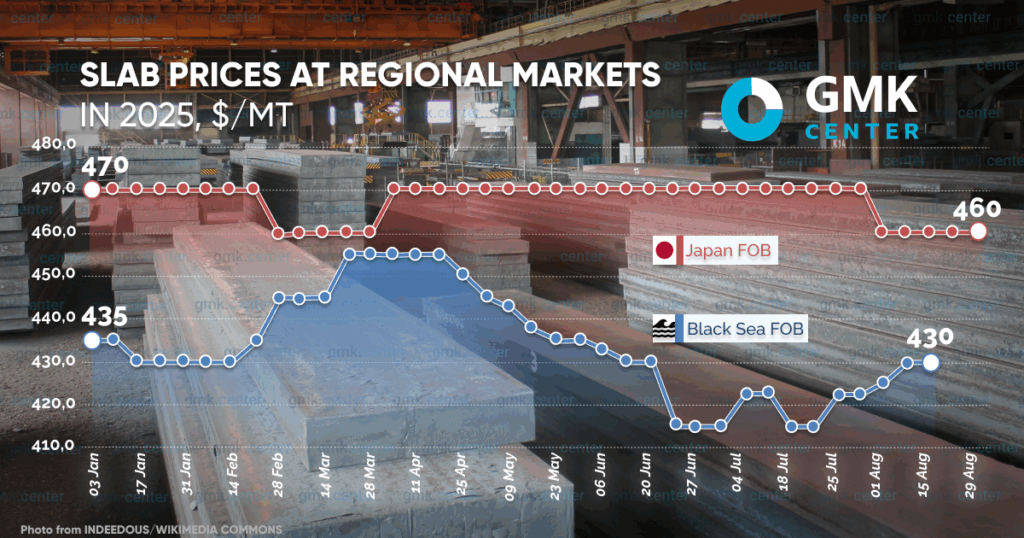

Regional markets saw mixed trends in slab prices in August. This is partly due to the fact that each market has its own unique conditions and influencing factors.

According to SteelOrbis, the average export price of Brazilian slab in August remained unchanged at $470/ton (FOB). At the same time, as Kallanish notes, the Brazilian steel sector saw a decline in activity in July. Capacity utilization in July was 7 p.p. lower than in the same period of 2024. Production of semi-finished products in July decreased by 0.4% compared to June to 727 thousand tons, of which slabs accounted for 689 thousand tons. Since the beginning of the year, the output of semi-finished products has decreased by 10% y/y – to 4.7 million tons.

The reason for this is that on August 7, the US imposed a 50% tariff on goods from Brazil. At the same time, Brazilian semi-finished products and finished steel are already subject to a 50% tariff in the US under Section 232. Due to such high tariffs, it will be cheaper for American buyers to purchase slabs from other countries.

Due to its heavy dependence on American buyers, the Brazilian steel industry may face additional difficulties on top of the problems associated with growing competition from cheap Asian imports. In the first half of this year, Brazil sold 2.7 million tons of slabs to the US, and 4.3 million tons in the whole of last year. The market appears to have been preparing for the new tariffs in advance, which led to an increase in imports. For example, in June, the US imported 353,700 tons of slabs from Brazil, compared to 326,000 tons in May.

Average prices for slabs on FOB Black Sea terms in August (as of the 15th) rose by 2% to $430/t. At the same time, the market itself remains quite active. Turkey’s own slab production in January-July amounted to 7.8 million tons (an increase of 8% year-on-year), while imports in the first half of the year grew by 5.3% year-on-year – to 2 million tons. Russian slabs account for about 56% of total imports, with imports in the first half of the year growing by 89% year-on-year – to 1.1 million tons.

Russian slab’s position in the EU remains significant, but the annual quota for imports of this product into the European Union is close to being exhausted ahead of September 30, when a new period will begin. As of August 15, only 27,000 tons remained of the 3.2 million ton quota. From October 1 and throughout the calendar year, it will be 3 million tons.

In turn, average slab prices in Japan fell by $10 – to $460/t in August. In other Asian markets, slab prices stabilized after a recent decline. According to SteelOrbis, Asian slab prices did not rise in August amid weak demand in China and competition from Russian products. Attempts by Asian slab exporters to raise prices in mid-August failed.

At the same time, the average benchmark price for slabs – hot-rolled coil (HRC) – fell by $5 to $490/t (China FOB) in August. Demand in regional HRC markets remained weak or stable last month, with prices fluctuating within a narrow range, in contrast to the last week of July, when global hot-rolled coil prices rose, supported by a strengthening Chinese market. The market saw a seasonal slowdown in August amid macroeconomic uncertainty in the world and China in particular, where there was both positive and negative news for this segment.

At the end of July, regional markets saw a predominantly downward trend in slab prices. The average export price of Brazilian slab in July fell to $470/t from $482/t at the end of June (on FOB terms) amid expectations of the introduction of duties on Brazilian imports.

-

Opinions Industry steel consumption

13 July 2026

13 July 2026

13 July 2026

13 July 2026