News Global Market hot-rolled prices 7981 22 January 2024

In the EU market, prices are supported by limited supply

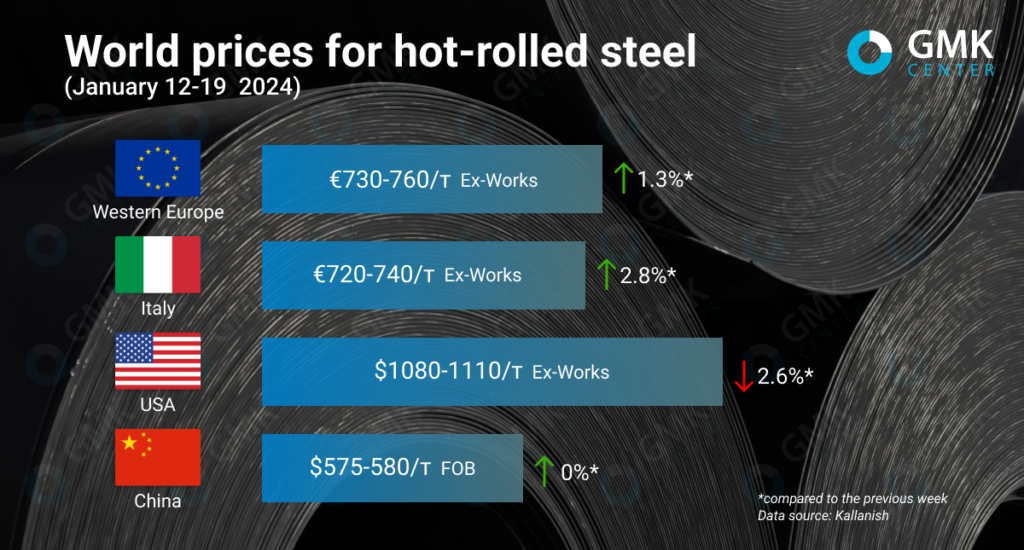

Global hot-rolled coil prices have risen in key markets since the beginning of 2024. In Europe, quotes are supported by a low supply of locally produced products and the exhaustion of import quotas. In the US, the trend is similar, but supply still exceeds demand, which restrains price growth. In the Chinese market, prices have remained stable since mid-December last year.

Prices for hot-rolled steel in Western Europe increased by €10/t, or 1.3%, compared to the previous week, to €730-760/t Ex-Works for the period January 12-19, 2024. At the same time, since the beginning of the year, rolled steel prices have increased by €60/t, or 8.6%. Prices for the relevant products in Western Europe have now reached their highest level since the end of May 2023. In general, the market has been on a steady recovery trend since November last year.

On the Italian market, prices for hot-rolled steel as of January 19, 2023, amounted to €720-740/tonne Ex-Works, which is €20/tonne, or 2.8% more than on January 12. Since the beginning of the year, product quotations have also increased significantly by €40/t.

European hot-rolled coil prices saw a significant increase in early January. This was facilitated by an increase in the target price levels for the relevant products by ArcelorMittal, the main producer of hot-rolled coils in the EU market. The company noted that it was raising its offer prices by €50/t amid limited import opportunities and low supply in the domestic market.

At the same time, the company is openly targeting €800/t, although buyers are not ready to work at such levels. Most buyers are not willing to pay more than €750/t, citing economic problems and increased logistics costs.

Negotiations on annual contracts between steel mills and the automotive industry are still ongoing. The average price for automakers is at least €800 per tonne, with some deals being made at higher prices. At the beginning of negotiations in November, the automotive industry demanded a discount of at least €100/t compared to last year’s contracts, which amounted to €800-850/t.

Prices for hot-rolled steel in Europe are expected to rise in the short term, as the market is undersupplied and import quotas for the first quarter have already been exhausted. At the same time, delivery times for products from local mills are already reaching March-April.

In the United States, prices for hot-rolled steel for the period December 12-19, 2024 decreased by $30/t, or 2.6% compared to the previous week to $1080-1120/t. At the same time, since the beginning of January, quotes have been growing and were at $1150/ton. As of the end of 2023, HRC was offered at $1080-1110/t on the US market.

The upward trend, which was recorded in early January, was supported by pricing abroad, particularly in Europe. In addition, one of the factors behind the rise in prices was the increase in the cost of iron ore. At the same time, the market did not expect the upward trend to last long, as demand was lower than supply.

Last week, hot-rolled coil prices in the US market began to decline, with a drop recorded for the first time since September. This happened amid weak demand and loyalty from steelmakers.

Production is currently at a fairly low level, which is a key factor in the growth and maintenance of prices. Although January was better than December in terms of demand, it is still not enough, and steelmakers will have to cut production further to keep prices at a profitable level. Currently, the lead time for orders is 4-5 weeks, which is normal.

Thus, the sharp increase in prices in early January was aimed at testing whether consumers were willing to pay more for a hot-rolled coil. The market is expected to stabilize in the near future. If US steelmakers resort to further capacity cuts and reduced supply, prices are likely to rise further.

-

Opinions Industry steel consumption

13 July 2026

15 July 2026

15 July 2026

15 July 2026