The market continues to be dominated by weak demand for finished rolled products and high uncertainty

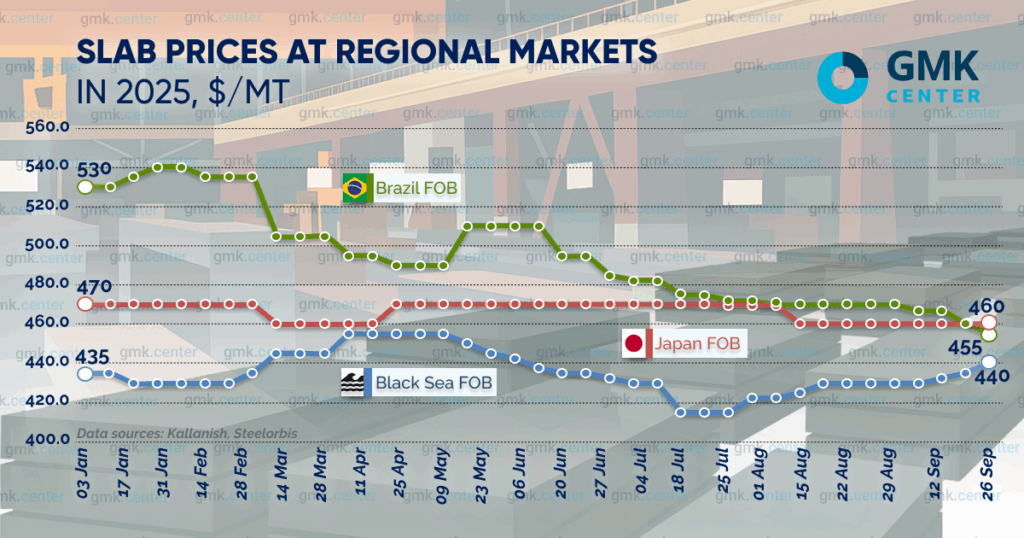

Regional markets saw mixed trends in slab prices in September. This is largely due to the fact that each regional market has its own unique conditions and influencing factors.

According to SteelOrbis, the average export price of Brazilian slabs fell by $15 to $455/t (FOB) in September. This is a direct consequence of the 50% tariff imposed by the US on goods from Brazil on August 7, which covers many types of Brazilian steel products. Due to such a high rate, it will be more profitable for American buyers to purchase slabs in other countries.

This situation was also reflected in slab production figures. In August, Brazilian mills reduced their production of semi-finished products by 9% compared to July, to 661,000 tons, of which 591,000 tons were slabs. Production of semi-finished products in January-August fell by 11.4% y/y, to 5.4 million tons.

At the same time, as Kallanish notes, in August, the Brazilian steel sector showed a slight increase in activity: capacity utilization rose to 67.5% after 66% in July. According to the Brazilian Steelmakers Association (IAB), steel production in the country in August increased by 2.3% compared to July, to 2.9 million tons. At the same time, in the first eight months of 2025, production decreased by 1.5% y/y, to 22.2 million tons.

Average slab prices in Japan remained unchanged in September at $460/t. In turn, average FOB Black Sea quotations rose by only $10 last month to $440/t.

Turkey remains the driver of the Black Sea slab market. According to TUIK, slab imports to Turkey jumped sharply in August, up 34% y/y to 406.1 thousand tons. In August, the structure of slab supplies to the Turkish market changed significantly. Russia increased its share to 36%, and a new source of imports appeared – China, which took 25% of the market in August. In January–August, imports of the product to Turkey grew by 11% y/y to 2.7 million tons.

The average price of slab imports to Turkey in August was $471/t. The price difference between the largest importers was quite significant: Russia supplied slabs at an average price of $449/t, while China supplied them at $486/t.

From October 1, exporters of certain types of products in Turkey are required to purchase at least 25% of the raw materials/semi-finished products necessary for their production on the domestic market. The new requirements may affect the import situation. According to Kallanish, since Turkey’s own slab production capacity is insufficient (domestic slab production in January–August fell by 5.2% y/y to 9.1 million tons), market participants expect an increase in slab imports.

The average benchmark price for slabs – hot-rolled coil (HRC) – continued to decline in August, falling by $5 to $485/t (on China FOB terms). The global HRC market remained largely weak and stable in September amid low prices and demand, as well as the absence of a clear trend for further development. Competition led to a slight decline in prices in some markets, but in others there was a moderate increase in hot-rolled coil quotations.

It should be noted that at the end of August, regional markets saw mixed trends in slab prices. The average export price of Brazilian slabs in August remained unchanged at $470/t (FOB) amid negative expectations regarding the introduction of duties on Brazilian imports.

-

Opinions Industry macroeconomics

28 May 2026

03 June 2026

03 June 2026

03 June 2026