News Global Market gas prices 7405 18 March 2026

The market remains sensitive to political statements

The European gas market continues to be affected by the ongoing conflict in the Middle East

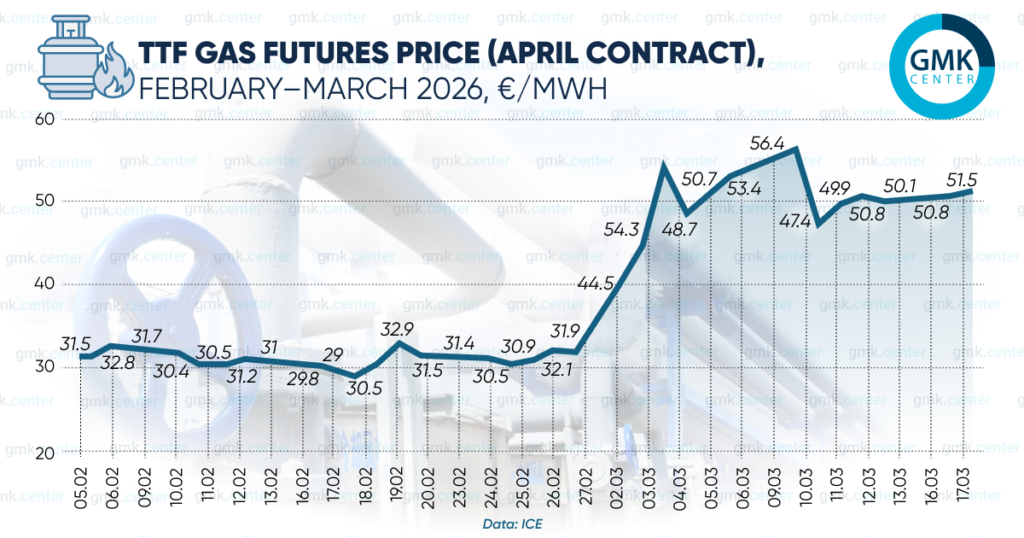

During the first week of the escalation (March 2–6), average European gas prices rose by nearly 50% to €45/MWh (prior to the escalation, the figure stood at €31/MWh). On March 9, according to ICE, one-month TTF futures rose to €56.4/MWh—the highest level since mid-February 2025.

The market, among other things, remains sensitive to political statements. For example, as early as March 10, following hints from the U.S. president that the conflict with Iran might soon end, the price fell to €47.4/MWh.

During trading on March 18, the price of futures rose above €55/MWh.

According to a report by British bank HSBC Holdings, as reported by Bloomberg, European natural gas prices this year will be 40% higher than previously forecast and will remain elevated through 2027 amid supply shortages caused by the war with Iran and the closure of the Strait of Hormuz. As noted, disruptions in LNG supplies will force European countries to pay a significant premium. Asian nations, which receive about 26% of their liquefied natural gas from Qatar and the UAE, will be forced to seek alternative suppliers.

According to the AGSI platform, as of March 17, 2026, European gas storage facilities were 28.93% full; last year, this figure stood at 34.47%. Europe is particularly sensitive to changes in LNG supply due to intensifying competition for it. Although direct gas imports from the Middle East to the region, Ember notes, are relatively small (Qatar accounts for about 10% of LNG supplies to the region), some countries, such as Italy and Belgium, are more dependent on it.

Last week, European Commission President Ursula von der Leyen proposed a solution to cap energy prices, including natural gas, to protect businesses and households from the consequences of the conflict in the Middle East. However, analysts caution against this move. In particular, it would hinder the region’s ability to compete for LNG cargoes on international spot markets. Furthermore, even existing regulations are underutilized. For instance, the market correction mechanism introduced by the European Commission in 2023 has never been used in practice during its entire period of validity.

As a reminder, in February, the European gas market was influenced by geopolitical and weather factors, as well as low inventory levels in European gas storage facilities. In particular, at the beginning of last month, price volatility was driven by concerns over threats to LNG supplies through the Strait of Hormuz; TTF futures also rose sharply in the first week of February due to worsening weather forecasts. In contrast, on February 17, the latter showed the lowest monthly settlement price—€29.82/MWh.