News Global Market scrap prices 2941 26 June 2024

Limited scrap supply keeps prices from falling significantly

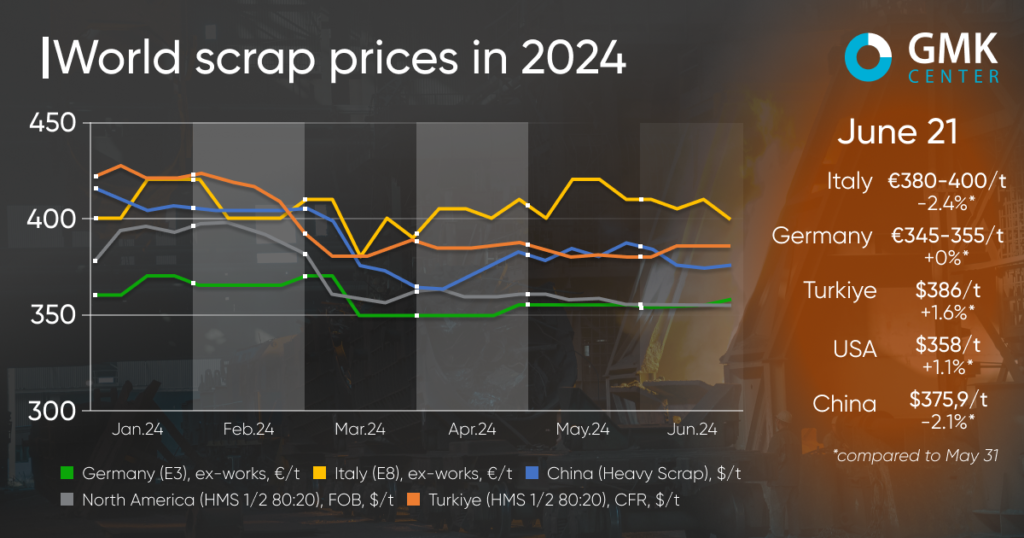

In June 2024, global scrap prices fluctuated under the influence of uncertain steel market prospects during the seasonal slowdown in consumption. The pre-holiday activity of Turkish consumers provided some support to the US and EU markets. At the same time, prices fell in China.

Scrap prices in Turkey have increased by $6/t, or 1.6%, to $386/t CFR since the beginning of June 2024 (as of June 25). The increase in quotations occurred in the first week of June, and then the price level stabilized.

The upward trend in early June is explained by increased demand for raw materials and the strengthening of the euro against the dollar. The increase in demand was driven by local steelmakers’ need to replenish stocks before Ramadan, which steelmakers believe was used by suppliers to raise prices. At the same time, scrap sellers emphasize that the higher price levels are caused by a shortage of raw materials due to difficulties in collecting them.

With the approach of the holiday season, activity in the Turkish market slowed down and prices stabilized as most steel mills fulfilled their procurement plans. In addition, scrap suppliers decided not to make price compromises, while steel producers disagreed with the reasonableness of prices.

«I don’t understand where suppliers are finding support to raise prices. The domestic scrap market in the US continues to decline amid a sharp drop in hot-rolled coil prices. In the EU, the euro is on the decline. There is not a single fundamental factor that would support the growth of scrap prices,» said a representative of a Turkish steel mill.

After the holidays, Turkish buyer activity was weak. Most plants extended their vacations or started maintenance. Market expectations differed, as suppliers planned to raise prices, while buyers hoped for a decline, as steel prices did not rise despite high production costs. Scrap shortages remain the main source of support for prices.

«Steelmakers will be in no hurry to buy scrap after the holiday and will put pressure on scrap prices, assessing the prospects for steel demand,» a scrap supplier said.

Most market participants expect raw material prices to remain in the range of $380-390/t in the short term, as there are currently no factors that would contribute to a significant decrease or increase.

The EU market shows a multidirectional trend with slight fluctuations. In Germany, scrap prices (E3) as of June 21 amounted to €345-355/t Ex-Works, which corresponds to the price level at the beginning of the month. In Italy, scrap prices (E8) fell by €10/t (-2.4%) – to €380-400/t Ex-Works during this period.

The German market remained largely stable in June due to unchanged domestic demand and declining exports. This trend is expected to continue until the end of the month amid stable commodity market conditions in Europe and the approaching summer holidays. The situation is similar in France and Luxembourg.

In Italy, scrap prices fluctuated throughout June due to the weak steel market. This month, demand for raw materials decreased, but so did availability. Steel producers are uncertain about the future prospects for steel demand, as previous attempts to raise prices for steel products have failed. At the same time, the scrap shortage is keeping prices from falling too far, and if demand increases, prices are expected to rise.

The North American scrap market in the period May 31-June 21 was marked by a slight increase of 1.1%, or $4/t, to $358/t US East Coast FOB. It was expected that in the June auction, scrap prices in the United States would decline due to weak demand from local steelmakers, who suffer from lower prices for hot-rolled steel. At the same time, prices were supported by improved export demand, particularly from Turkey.

In China, scrap prices have fallen by $11/t, or 2.9%, to $373.04/t since the beginning of June.

Raw material quotations have been declining throughout the month due to deteriorating demand from steelmakers. Seasonal unfavorable weather conditions have a negative impact on steel demand, which, in turn, is forcing steelmakers to reduce capacity utilization or take some of their facilities out of service for maintenance. In addition, some steelmakers say that pig iron is currently more cost-effective for steel production than scrap. At the same time, high temperatures and rainy weather are leading to a decrease in the collection of raw materials, which provides some support to prices in the current environment.

-

Opinions Industry rolled steel

25 June 2025

30 June 2025

30 June 2025

27 June 2025