News Global Market hot-rolled prices 7771 05 February 2026

In the EU and the US, positive dynamics were supported by large local factories, which gradually raised their offer prices

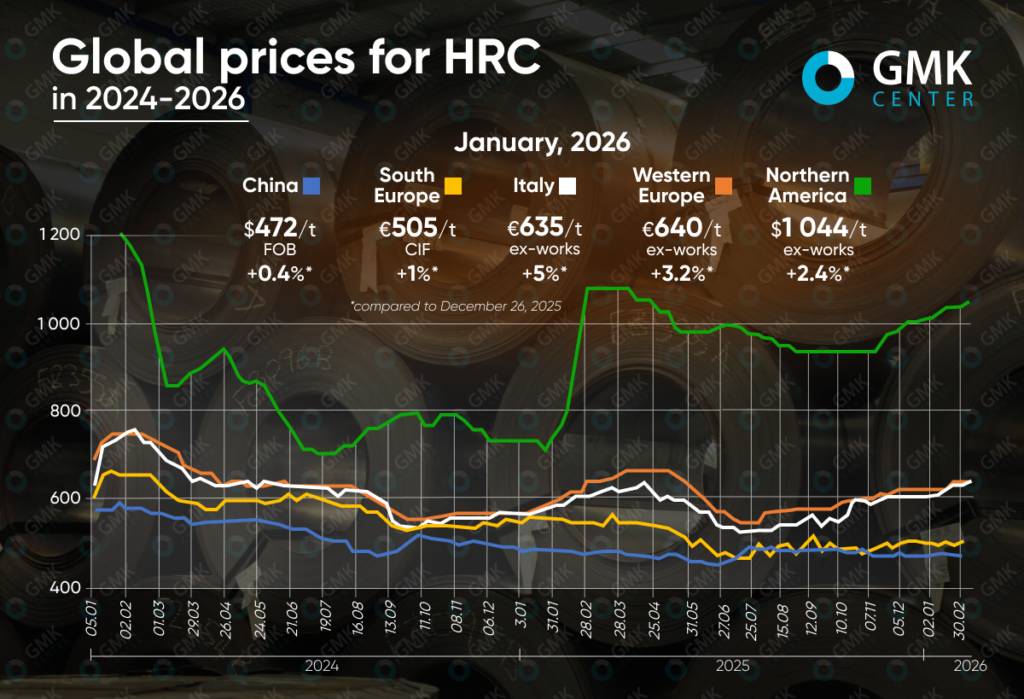

Global prices for hot-rolled coil (HRC) rose in most key regions in January 2026. The largest market upturn was recorded in the EU and the US, while China saw only a slight increase in prices after a weak November-December.

EU

In the European market, hot-rolled coil prices rose by between 1% and 5% in January. In particular, offers in Italy rose by 5% between December 26, 2025, and January 30, 2026, to €635/t ex-works, with expectations of a continuation of the trend in early February (≈€645/t ex-works).

In Western Europe, product prices rose by 3.2% to €640/t ex-works. Offers for imported products in Southern Europe rose to €505/t CIF (+1%).

The January recovery in quotations was driven by a sharp decline in import supply due to uncertainty surrounding CBAM and expected changes in EU protective measures, which effectively narrowed the arbitrage. The key drivers were successive price increases by European mills, led by ArcelorMittal, as well as limited production capacity at mills until the end of Q1. The market was further supported by a shortage of cold-rolled coil: the reorientation of plants towards HRC and HDG, shutdowns of some capacities, and anti-dumping investigations made cold-rolled coil (CRC) the narrowest segment.

At the same time, demand remained subdued. Processors were unable to pass on the increase in costs to the prices of finished products, and buyers actively used the stockpiles formed at the end of 2025. Imports were hampered by quotas, uncertainty regarding CBAM, and the need to reserve significant funds for future carbon payments.

In February, the market is likely to maintain a moderate upward trend due to limited supply, but growth will be held back by weak real demand. By the end of the quarter, HRC prices may gradually approach €670-700/t ex-works in Western Europe, provided that imports stabilize and there is no sharp decline in consumption.

USA

In North America, HRC prices rose by 2.4% in January (compared to the end of December) to $1055.5/t ex-works. Prices in the region are currently at their highest level since April 2025.

The January growth in the US market was driven by a combination of logistical and production factors. A series of weekly increases from Nucor set an upward tone for the market, while shipment delays due to winter weather and chronic plant underperformance reduced spot availability. Additional pressure was created by limited supply from Cleveland-Cliffs and United States Steel, as well as production disruptions at some other manufacturers’ sites.

Against this backdrop, service centers actively replenished their inventories after their sharp decline at the end of 2025, which fueled short-term demand. At the same time, weak imports and limited delivery times (3-5 weeks) strengthened the position of domestic mills. However, market participants were already noting the risk of saturation at the end of the month: large volumes of outstanding orders could quickly increase supply.

China

China saw the lowest growth rate – 0.4% to $472/t.

January fluctuations in HRC quotations took place amid weak final demand and high dependence of the spot market on the futures market. In the middle of the month, prices received short-term support due to a slight reduction in inventories and a symbolic increase in apparent demand, but this effect was largely due to speculative purchases. On the eve of the Chinese New Year celebrations, sentiment deteriorated rapidly: expectations of a seasonal decline in consumption put pressure on futures and, accordingly, on spot prices.

The export segment remained sluggish. Chinese HRC offers declined amid pessimistic expectations and competition from other regions, while Middle Eastern buyers showed subdued activity, focusing only on selected brands. At the same time, the semi-finished products market looked livelier than HRC.

In February, prices are likely to stabilize with moderate downward pressure due to the post-holiday pause in demand. Export sales and possible restocking may provide support, but without clear signals from domestic consumption, a significant increase in prices seems unlikely.

-

Opinions Industry steel consumption

13 July 2026

26 July 2026

24 July 2026

24 July 2026