News Global Market EU 618601 28 February 2025

Construction recovery and import decline to support the European steel market

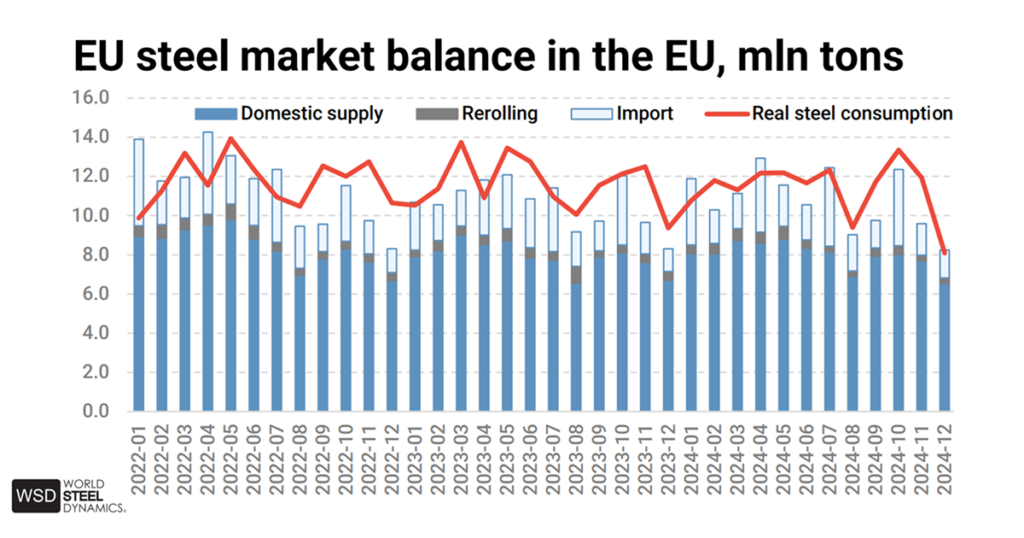

Steel demand in the European Union remains unstable, but analysts at World Steel Dynamics (WSD) forecast a gradual recovery in Q2 2025. After a decline in steel-consuming industries at the end of 2024, the market is showing the first signs of improvement, particularly in the construction sector.

According to the February report by WSD’s EU Steel Dynamics Reports and Analytics Service, total activity in steel-consuming industries fell by 1.6% year-on-year in December 2024. However, at the beginning of 2025, business sentiment in the Eurozone improved, which could positively impact demand in the coming months. The ZEW Business Expectations Index rose by 6.2 points in February, reaching 24.2 points, significantly above the average level.

The construction sector is expected to be one of the key drivers of steel demand. Activity in this sector is projected to return to pre-pandemic levels by the end of Q2. Some recovery is also expected in mechanical engineering and metal structures manufacturing, although at a slower pace.

A decline in steel imports to the EU could further strengthen domestic demand. Between January 1 and February 18, imports of hot-rolled coil (HRC) fell by 42% year-on-year, reducing competition from external suppliers. If new import restrictions are introduced in April, flat-rolled steel imports could decrease by another 25% quarter-on-quarter, further supporting European steel producers.

WSD analysts believe that if demand continues to improve and imports decline, steel prices in Q2 could rise to €640-650 per ton. However, numerous risks remain, including economic uncertainty, regulatory changes, and global market dynamics.

You can sign up for a trial subscription to the EU Steel Dynamics Reports and Analytics Service via the link.

-

Opinions Industry rolled steel

25 June 2025

27 June 2025

27 June 2025

27 June 2025