News State semis prices 93 08 July 2026

Weak demand and falling scrap metal prices pushed prices down

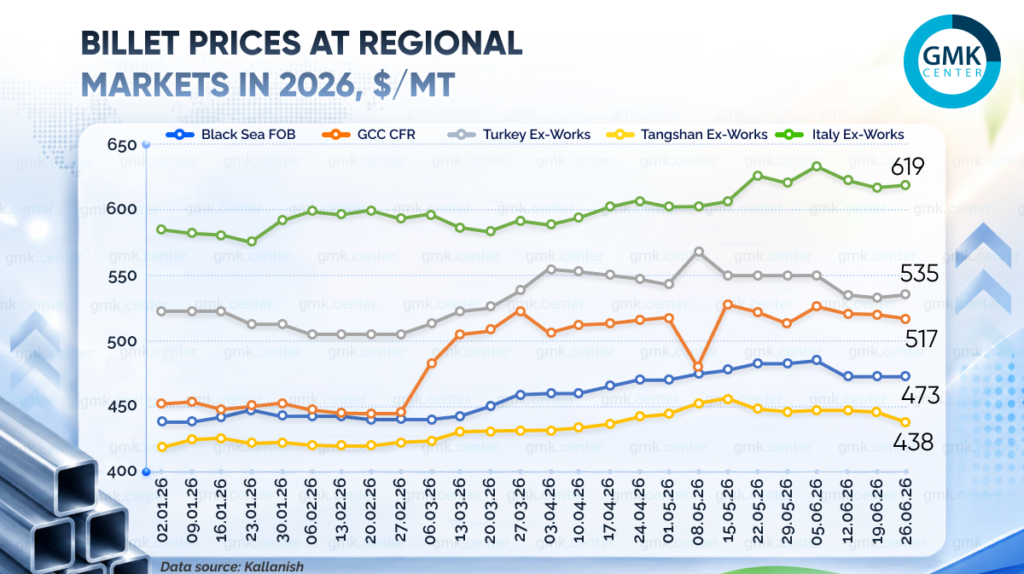

In most regional markets for square billets, prices fell by 5–15 dollars per tonne in June. The Gulf states were an exception, where the war in the region created a unique market situation, and prices rose slightly last month to 517 dollars per tonne.

June began without a clear trend in the global square billet market: prices in regional markets were supported by high production costs. In the middle of the month, the market remained sluggish, with prices stable, except for a decline in the Turkish market. At the same time, market participants anticipated a fall in prices due to the possible return of Iranian products. By the end of the month, activity had slowed even further, and prices began to fall in almost all regional markets following a decline in demand and a drop in scrap metal quotations.

Turkey

In the Black Sea square billet market (Black Sea FOB), average quotations fell by $10 in June to $473/t. According to Turkish buyers, an acceptable price for Russian billets is $500/t CFR Turkey, whilst Russian suppliers are aiming for $515/t CFR.

Russian billet exporters are facing pressure from the strong rouble and the return of Iranian products to certain export markets, against a backdrop of falling domestic prices for the product in Turkey.

The average price of square billets on Turkey Ex-Works terms also fell in June – by $15, to $535/t. Trade remained sluggish throughout the second half of the month, with prices falling due to a slowdown in rebar sales caused by a reduction in construction activity and a fall in scrap metal prices.

According to Kallanish, on 10 June, the Kardemir plant held a tender to sell 100,000 tonnes of billets, reducing the price by $5–10 per tonne – to $525/t for the S235JR grade and to $530/t for the B420 grade. These quotations do not include 20% VAT. Interest in the products is driven by attractive prices compared to imports and high scrap prices on the domestic market, as well as the requirement to source at least 25 per cent of steel raw materials domestically when producing rolled steel for export.

This requirement continues to support demand for domestic billets. At the same time, domestic billet production in Turkey fell by 0.6% year-on-year over the first five months of 2026, to 9.8 million tonnes.

According to the Turkish Statistical Institute (TUIK), imports of billets into Turkey rose by 23% month-on-month in May, reaching 488,000 tonnes. The largest suppliers in May were Russia – 133,000 tonnes (+20% year-on-year) and Malaysia – 130,000 tonnes (–14% year-on-year). Russia supplied billets at $470/tonne, whilst the average import price was $483/tonne.

ASEAN countries

The billet market in ASEAN countries is showing a steady downward trend in prices against a backdrop of low trading activity. By the end of June, Chinese billet prices had fallen to $485/t from $500–505/t (on a CFR Manila basis) at the start of the period. The key factors behind the fall were lower Chinese futures prices and cheaper raw materials – iron ore and scrap metal. Lower freight costs provided further support for the price decline.

Demand in the region remains sluggish due to the rainy season in a number of countries and macroeconomic instability. Buyers are facing weakening national currencies in Indonesia and the Philippines, which, combined with concerns over GDP growth, is prompting them to adopt a wait-and-see approach in anticipation of further price reductions. At the same time, Chinese suppliers, operating on the edge of profitability, are exercising caution and are reluctant to accept excessively low price offers, which is creating additional tension in trade.

China

According to Kallanish, average prices for billet from Tangshan (China) in June ranged between $438 and $447 per tonne. In the second half of the month, prices for local billet fell due to weak demand from rolling mills during the off-season and traders’ limited appetite for speculation. Due to low sales and warehouses being overstocked with finished products, consumers cut back on raw material purchases. Furthermore, steelmakers were unable to reduce prices any further due to rising coke costs, whilst losses on billet production exceeded 50 yuan per tonne.

Persian Gulf

According to Kallanish, average billet prices in the Persian Gulf countries stabilised in June following May’s volatility and rose by $4 to $517/t (CFR). The logistics situation, despite apparent improvements, remains highly uncertain. Buyers are including alternative unloading ports in their contracts in case the Strait of Hormuz is blocked. Due to rising freight costs from China, Saudi Arabian buyers are adopting a wait-and-see approach. At the same time, billet supplies from Oman and Saudi Arabia are helping UAE mills avoid import delays.

Italy

Average Ex-Works quotations for square billets in Italy at the end of June fell slightly compared with the end of May – to $619/t. However, at the start of June, quotations had risen to $633/t.

As previously reported, the National Bank of Ukraine (NBU) expects the average price of steel billets to rise by 4.9% year-on-year by the end of 2026, to $487.7/t on FOB Ukraine terms. The forecast for 2027 and 2028 stands at $510.4/t (+4.7% year-on-year) and $518/t (+1.5% year-on-year) respectively.

-

02 July 2026

02 July 2026

18 June 2026

18 June 2026